Public Adjuster Fees Florida: What to Expect in Florida for Your Insurance Claim

Quick Answer

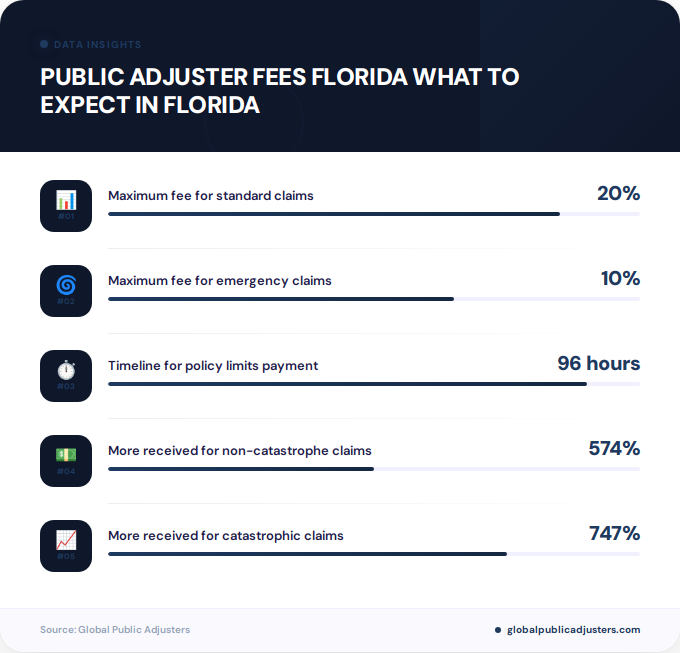

In Florida, public adjuster fees are capped at20% of your insurance claim paymentfor standard claims, but drop to10% for state of emergency claims(such as hurricane damage) for one year after the declaration. If your insurer pays policy limits within 96 hours, adjusters can only charge an hourly rate rather than a percentage fee.

When a hurricane tears through Miami or Tampa, or water damage floods your Jacksonville home, understandingpublic adjuster fees Floridaregulations becomes critical to protecting your financial interests. Florida’s insurance landscape is complex, and knowing what to expect in Florida regarding adjuster compensation can mean the difference between a fair settlement and leaving thousands on the table.

Here’s a surprising statistic: According toindustry data from the Florida Association of Public Insurance Adjusters, policyholders using public adjusters received574% morefor non-catastrophe claims and747% morefor catastrophic claims compared to those who handled claims themselves. Yet many Florida homeowners hesitate because they’re unsure about the costs involved.

This comprehensive guide breaks down everything you need to know about public adjuster fees in Florida, from state-mandated caps to payment structures, so you can make informed decisions when disaster strikes.

What Are Public Adjuster Fees in Florida?

Public adjusters are licensed professionals who work exclusively for policyholders, not insurance companies, to assess damage and negotiate fair settlements. In Florida, these professionals are compensated through fees that are strictly regulated by state statute to prevent exploitation during vulnerable times.

Unlike company adjusters who work for insurers,public adjusters represent your interestsand typically work on a contingency basis. This means they only get paid when you receive a settlement, aligning their interests directly with yours.

The fee structure is designed to be transparent and fair, with specific caps enforced by the Florida Department of Financial Services. Understanding these regulations helps you evaluate whether hiring a public adjuster makes financial sense for your specific situation.

How Do Florida’s Public Adjuster Fee Caps Work?

Florida law establishes clear maximum fees that public adjusters can charge, with different caps depending on the circumstances of your claim. According toFlorida Statute 626.854, these regulations protect consumers while ensuring adjusters are fairly compensated for their expertise.

| Claim Scenario | Maximum Fee | Duration/Conditions |

|---|---|---|

| Standard Claim (Non-Emergency) | 20%of settlement | Always applies |

| State of Emergency Claim | 10%of settlement | 1 year after declaration |

| Reopened/Supplemental Claim | 20%of new payment only | Based on additional recovery |

| Policy Limits Paid Within 96 Hours | Hourly rateonly | No percentage allowed |

These caps represent themaximumfees allowed, not necessarily what every adjuster charges. Many factors influence the actual fee you’ll pay, including the complexity of your claim, the adjuster’s experience, and market conditions in your specific Florida region.

It’s worth noting thatthe payment structure in Floridais designed to ensure adjusters cannot charge for payments received before you signed the contract. This protects policyholders from paying fees on settlements they would have received anyway.

What’s the Difference Between Emergency and Standard Claims?

The distinction between emergency and standard claims in Florida significantly impacts what you’ll pay. Astate of emergency claimoccurs when the Governor declares an emergency due to hurricanes, tropical storms, wildfires, or other disasters affecting large areas.

When Governor DeSantis declares a state of emergency for a hurricane threatening Orlando or Tampa, the fee cap drops to10% for one full yearfrom the date of that declaration. This reduced rate helps Florida residents recover without excessive fees during catastrophic events.

After that one-year window expires, the standard20% capapplies. This means timing matters when you hire a public adjuster after a major storm. According tothe Florida Department of Financial Services, these protections help thousands of Florida families each year during disaster recovery.

Standard claims, such as routine water damage from a broken pipe in Jacksonville or fire damage in Fort Lauderdale, fall under the 20% cap from the beginning. These non-catastrophic events don’t trigger the emergency provisions.

Why Do Public Adjusters Charge These Fees?

Understanding the value proposition helps explain the fee structure. Public adjusters invest significant time, expertise, and resources into your claim. They handle documentation, damage assessment, policy interpretation, negotiation with insurers, and often coordination with contractors and engineers.

Consider what a public adjuster provides: detailed damage inventories, accurate cost estimates, policy coverage maximization, negotiation expertise, and advocacy throughout what can be a months-long process. Most importantly, they work on contingency, meaning if they don’t increase your settlement, you don’t pay their percentage fee.

Florida’s licensing requirements are more stringent than many other states, requiring specific self-insurance of$350,000for public adjusters. This ensures only qualified, financially stable professionals can operate, providing additional consumer protection.

How Does the Payment Structure Actually Work?

The standard payment model for public adjusters in Florida is contingency-based, meaning fees come directly from your insurance settlement after the insurer pays you. Here’s the typical timeline and process you can expect in Florida:

Step 1: Contract Signing– You sign a contract detailing the fee percentage (within legal limits), services provided, and cancellation rights. Florida law requires specific disclosures in these contracts.

Step 2: Claim Work– The adjuster documents your damage, researches your policy, prepares estimates, and negotiates with your insurance company. You pay nothing during this phase.

Step 3: Settlement– When your insurer issues payment, you receive the full amount. You then pay the agreed-upon percentage to your public adjuster based on the recovered amount.

For example, if your adjuster secures a$50,000 settlementon a standard claim with a 20% fee agreement, you would pay$10,000to the adjuster and keep$40,000. However, if they negotiate a supplemental claim increasing your settlement by an additional $20,000, the fee applies only to that $20,000 increase, not the original amount.

There’s an important exception: if your insurance company pays policy limits within96 hoursof your loss report, the adjuster cannot charge a percentage fee. Instead, they’re entitled only to reasonable hourly compensation based on actual time and documented expenses.This payment provisionprotects policyholders when insurers act quickly and fairly.

Can You Cancel a Public Adjuster Contract in Florida?

Florida law provides specific cancellation rights to protect consumers who hire public adjusters. Understanding these rights is crucial before signing any agreement, especially during the stress following property damage in Miami, Tampa, or anywhere else in Florida.

Forstandard claims, you have10 business daysfrom signing the contract to cancel without penalty or obligation. Simply provide written notice to the adjuster within this window.

Forstate of emergency claims, protection is even stronger. You can cancel within30 days of the lossor10 business days after signing, whichever period is longer, without any cancellation fees or penalties.

This extended protection recognizes that disaster victims may sign contracts under duress or make hasty decisions immediately after catastrophic events. If a hurricane damages your Orlando home and you hire an adjuster the next day, you have substantial time to reconsider that decision.

After these windows close, cancellation may still be possible but could involve fees or obligations outlined in your specific contract. Always read cancellation provisions carefully before signing.

What Changed in 2026 for Public Adjuster Fees?

Florida’s legislature continues refining public adjuster regulations. According toSenate Bill 266 analysis, legislation effectiveJuly 1, 2026introduced several important provisions affecting both adjusters and policyholders.

The most significant change requires public adjusters to provide awritten loss estimate within 60 daysof contract execution. This ensures policyholders understand the potential value of their claim early in the process, promoting transparency and informed decision-making.

The 2026 legislation also clarifies disciplinary actions the Department of Financial Services can take against adjusters who violate regulations, strengthening consumer protections across Florida.

Legal challenges continue as well. A lawsuit in Miami-Dade County currently challenges the state’s fee cap and 48-hour solicitation ban. According toproperty insurance coverage law analysis, this case argues these restrictions infringe on public adjusters’ rights, though the fee caps remain in effect as litigation proceeds.

Additionally, proposed bills have sought to further restrict adjuster fees, with some proposing caps as low as5%. While these proposals haven’t become law, they reflect ongoing policy debates about balancing consumer protection with access to professional claims assistance.

What Should You Look for When Hiring a Public Adjuster?

Not all public adjusters offer the same value, even when charging the same fee percentage. When selecting representation for your Florida claim, consider these factors beyond just cost:

Licensing and Credentials– Verify the adjuster holds a current Florida public adjuster license through the Department of Financial Services. Check for disciplinary actions or complaints.

Experience with Your Claim Type– Whether you’re dealing withwater damage in Florida, hurricane damage, fire loss, or other perils, look for proven experience with similar claims.

Local Knowledge– Florida’s diverse climate and building codes vary by region. An adjuster familiar with Jacksonville construction differs from one experienced in Miami high-rises or Tampa residential communities.

References and Reviews– Request references from recent clients with similar claims. Online reviews provide insight, but focus on detailed testimonials that describe actual results and service quality.

Communication Style– You’ll work closely with your adjuster for weeks or months. Choose someone who communicates clearly, responds promptly, and keeps you informed throughout the process.

Fee Negotiation– While Florida sets maximum fees, some adjusters charge below these caps. The fee percentage ranges from 10% to 20% depending on claim type and circumstances, with variation based on claim complexity, potential recovery amount, and market factors. Pricing depends on your specific situation, and it’s worth discussing fee structures with multiple adjusters before committing.

Remember that the lowest fee doesn’t necessarily provide the best value. An adjuster who charges 15% but secures a $100,000 settlement provides better results than one who charges 10% but only obtains $60,000.

For those considering whether professional representation makes sense,Global Public Adjustersoffers consultations to help Florida homeowners understand their options and potential claim value before making commitments.

Key Takeaways

- Standard claim fees are capped at 20%of your settlement amount in Florida, while state of emergency claims drop to 10% for one year after the governor’s declaration.

- Contingency-based paymentmeans you pay nothing unless your adjuster secures a settlement, aligning their interests with maximizing your recovery.

- Statistical evidence shows dramatic value: Florida policyholders using public adjusters received 574% more for standard claims and 747% more for catastrophic claims compared to self-representation.

- Cancellation protections existwith 10 business days for standard claims and up to 30 days for emergency claims, protecting consumers who reconsider their decisions.

- 2026 legislative changes requirewritten loss estimates within 60 days of contract signing, increasing transparency in the adjuster-client relationship.

- Fee caps represent maximums, not standard rates: actual fees vary from 10% to 20% based on claim complexity, timing, and negotiation, with pricing dependent on your specific circumstances.

- Choose adjusters based on credentials, experience, and proven resultsrather than fees alone, since a higher-paid adjuster who secures a substantially larger settlement provides superior value.

People Also Ask

Are public adjuster fees tax deductible in Florida?

Public adjuster fees may be tax deductible if the claim relates to business property or rental property, but generally are not deductible for personal residence claims. Consult a tax professional for guidance specific to your situation, as tax treatment depends on the property type and claim circumstances.

Can a public adjuster charge different fees for different parts of a claim?

No, Florida law requires a single fee percentage applied uniformly to the entire claim settlement. Adjusters cannot charge different rates for different coverage types within the same claim, such as charging 15% for structure damage but 20% for contents.

What happens if I fire my public adjuster before the claim settles?

If you terminate the contract after the cancellation period, the adjuster may be entitled to compensation for work already completed, typically based on hourly rates or a prorated percentage depending on contract terms. Review your specific contract’s termination provisions to understand your obligations.

Do I pay the public adjuster directly or does the insurance company?

In Florida, the insurance company pays you directly, and you then pay the public adjuster according to your contract. Some adjusters may request the insurance company issue a two-party check, but the payment flows through you as the policyholder.

Can public adjusters charge upfront fees in Florida?

No, Florida law prohibits public adjusters from collecting fees before the insurance company pays the claim. The contingency-based model protects consumers from paying for services that don’t result in settlements, though adjusters can charge for certain out-of-pocket expenses with proper documentation.

What if my insurance company offers a settlement before I hire a public adjuster?

If you receive and accept an offer before signing with a public adjuster, you pay no fees on that amount. However, a public adjuster can still review the offer, potentially find underpayments, and negotiate a supplemental claim, charging fees only on the additional recovery obtained.

Frequently Asked Questions

How much does a public adjuster cost for a typical homeowner’s claim in Florida?+

Public adjuster fees in Florida range from 10% to 20% of your insurance settlement depending on whether your claim falls under a declared state of emergency. For a $50,000 settlement on a standard claim, you would pay approximately $10,000 at the 20% cap, while emergency claims would cost $5,000 at the 10% rate. Actual costs depend entirely on your specific claim value and circumstances.

When does the 10% emergency fee cap expire after a hurricane?+

The 10% fee cap for state of emergency claims expires exactly one year from the date of the governor’s emergency declaration, not from when the storm occurred or when you filed your claim. After that one-year period, the standard 20% cap applies even if your claim is still being negotiated or remains unsettled.

What happens if my public adjuster gets me a much larger settlement than initially offered?+

You pay the agreed percentage only on the total amount recovered, which typically results in significantly more money in your pocket even after fees. For example, if your insurer initially offered $20,000 but your adjuster negotiates $80,000, you pay the fee on $80,000 but net $64,000 (at 20%), compared to the $20,000 you would have received without representation.

Can I hire a public adjuster if my insurance claim was already denied?+

Yes, public adjusters frequently help policyholders appeal denied claims or reopen closed claims when they believe the denial was unjustified. The fee structure remains the same, charged as a percentage of any settlement ultimately obtained. Many Florida residents successfully overturn denials with professional representation, asthe appeals processrequires detailed documentation and policy expertise.

Are there any situations where I wouldn’t pay the percentage fee?+

Yes, if your insurance company pays your policy limits within 96 hours of receiving your loss report, the public adjuster can only charge an hourly rate rather than a percentage fee. Additionally, you pay no fees on any amounts paid by your insurer before you signed the adjuster contract.

Do public adjuster fees vary by location within Florida?+

The fee caps are uniform statewide under Florida law, but the actual percentage charged may vary based on local market conditions, claim complexity, and individual adjuster practices. An adjuster inJacksonvilleand one in Miami both operate under the same 10-20% legal framework, though their specific rates within those limits may differ.

Should I negotiate the fee percentage with a public adjuster?+

Related:How Long Does an Insurance Claim Take in Tampa?

Related:How to Navigate the Water Damage Insurance Claim Process in Tampa: A Complete 2026 Guide

Related:Public Adjuster Colorado in Florida: Complete 2026 Cross-State Licensing and Practice Guide

Yes, fee percentages are negotiable within the legal caps. Factors affecting negotiation include your claim’s size, complexity, the adjuster’s workload, and competitive market conditions. However, focus on the total net recovery rather than just the fee percentage, since a skilled adjuster charging 20% who secures a substantially higher settlement provides better value than a discount adjuster at 15% who achieves minimal results.