How Long Does an Insurance Claim Take in Tampa?

Quick Answer

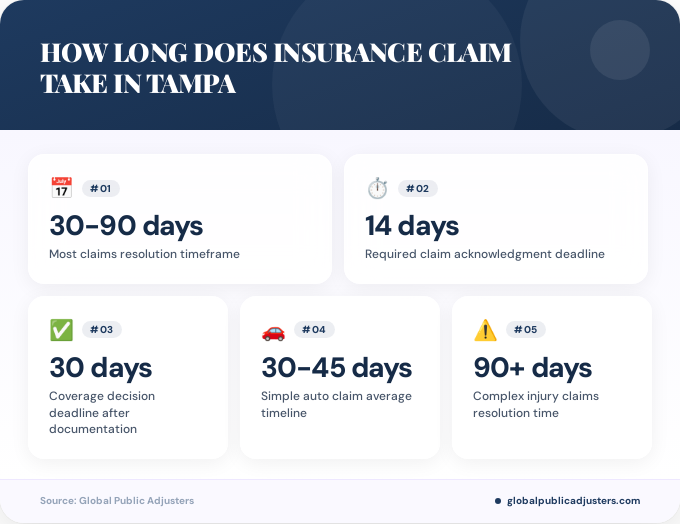

Most insurance claims in Tampa take30 to 90 daysto resolve for property damage and auto incidents, though complex cases involving severe injuries or disputed liability typically extend beyond 90 days. Florida law requires insurers to acknowledge claims within 14 days and issue coverage decisions within 30 days of receiving all documentation.

Understanding Insurance Claim Timelines in Tampa

If you’re dealing with an insurance claim in Tampa, you’re probably asking yourself: how long will this actually take? Whether you’ve experienced water damage from Tampa’s heavy summer storms, a car accident on Interstate 275, or hurricane damage to your Ybor City property, understanding insurance claim timelines can help reduce your stress and set realistic expectations.

The timeline for how long an insurance claim takes in Tampa varies significantly based on the claim type, complexity, and your insurer’s workload. Simple claims like minor fender benders or straightforward property damage typically resolve within30 to 60 days, while complex cases involving severe injuries, liability disputes, or major hurricane damage can stretch beyond90 daysor even several months.

Tampa’s unique position on Florida’s Gulf Coast means residents face specific challenges, from frequent thunderstorms causing water damage to periodic hurricane threats that can overwhelm local insurance adjusters. These regional factors directly impact how quickly your claim moves through the system.

What Are Florida’s Legal Requirements for Insurance Claim Processing?

Florida law establishes specific timeframes that insurance companies must follow when processing claims. Understanding these legal deadlines empowers you to hold your insurer accountable and recognize when delays become unreasonable.

Within 14 days, your insurance company must acknowledge receipt of your claim after you submit it. This initial acknowledgment doesn’t mean approval, it simply confirms they’ve received your documentation and started reviewing your case. According toFlorida property insurance regulations, insurers must respond promptly to avoid bad faith claims.

Insurance companies in Tampa must issue acoverage decision within 30 daysafter receiving all required information and documentation. This 30-day clock starts only when you’ve submitted every piece of evidence they’ve requested, including photos, estimates, medical records, or police reports.

Final payment or denial must occur within 90 daysof when you originally filed the claim, unless exceptional circumstances exist such as ongoing investigations, catastrophic events affecting the region, or complex liability determinations. These deadlines apply to most property and auto claims throughout Tampa and the broader Florida market.

How Long Do Different Types of Claims Take in Tampa?

The type of insurance claim you’re filing significantly impacts the resolution timeline in Tampa. Here’s what you can expect for the most common claim types:

| Claim Type | Average Timeline | Key Factors |

|---|---|---|

| Simple Property Damage | 30-60 days | Minor water damage, theft, small fires |

| Moderate Property Damage | 45-90 days | Hurricane damage, major water damage |

| Simple Auto (PIP) | 30-45 days | Minor accidents, clear liability |

| Complex Injury Claims | 90+ days | Severe injuries, disputed liability |

Auto insurance claimsin Tampa typically move faster than property claims, especially for Personal Injury Protection (PIP) coverage. Florida requires insurers toaccept or reject PIP claims within 30 daysof receiving all required documentation. Simple collision claims with clear liability usually resolve within 30-45 days.

Property damage claimsvary widely depending on the cause and extent of damage. A leaking pipe in your South Tampa home might settle in 30-45 days, while hurricane damage affecting your entire roof structure could take 60-90 days or longer. Tampa’s position along the Gulf Coast means hurricane-related claims are particularly common and often face extended timelines due to regional demand.

Personal injury claimsrepresent the longest category, often extending well beyond 90 days. These cases require complete medical treatment records, long-term prognosis evaluations, and complex liability determinations. If you’ve been injured in a Tampa car accident on Dale Mabry Highway or Bayshore Boulevard, expect your claim to take several months, particularly if injuries are severe.

What Factors Affect Your Claim Timeline in Tampa?

Several specific factors influence how long an insurance claim takes in Tampa, from documentation completeness to seasonal considerations unique to Florida’s Gulf Coast.

Claim complexitystands as the primary timeline determinant. A straightforward claim with clear liability, complete documentation, and no disputes typically moves through the system efficiently. However, if fault is contested, injuries are severe, or multiple parties are involved, your claim timeline extends significantly as adjusters conduct thorough investigations.

Documentation quality and completenessdramatically impact processing speed. Claims supported by detailed photos, professional estimates, police reports, and comprehensive medical records move faster than those requiring repeated requests for additional information. Tampa claimants who submit thorough documentation upfront often see their claims resolved weeks earlier than those who provide incomplete information.

Insurance companies often use strategic delays on high-value claims, particularly those involving severe injuries or approaching policy limits. These delays aren’t accidental, they’re calculated to pressure claimants into accepting lower settlements. Understanding this tactic helps Tampa residents stand firm during negotiations.

Insurer workload and resourcessignificantly affect timelines, especially following major weather events. When hurricanes impact Tampa Bay, local adjusters become overwhelmed with claims, leading to processing delays that can extend timelines by 30-60 additional days. Insurance companies must prioritize claims, and yours might wait behind hundreds of others filed simultaneously.

Your cooperation and availabilityalso matters. Promptly responding to adjuster requests, scheduling inspections quickly, and maintaining open communication keeps your claim moving forward. Tampa claimants who are difficult to reach or slow to provide requested information inadvertently extend their own timelines.

Working with aqualified public adjuster in Floridacan help navigate these complexities and potentially accelerate your claim by ensuring all documentation is complete and professionally presented from the start.

How Can You Speed Up Your Insurance Claim in Tampa?

While you can’t control every aspect of your claim timeline, several strategic actions can help expedite the process and avoid unnecessary delays in Tampa.

Document everything immediately.Take comprehensive photos and videos of all damage before making any repairs. For Tampa property damage, photograph water lines, structural damage, affected belongings, and any visible causes like roof leaks or broken pipes. For auto accidents, document vehicle damage, accident scenes, and road conditions.

File your claim promptly.Florida law doesn’t penalize slight delays, but insurers process claims in the order received. Filing within 24-48 hours of the incident ensures your claim enters the queue quickly, particularly important during Tampa’s busy hurricane season when adjusters face heavy workloads.

Submit complete documentation upfront.Rather than waiting for the adjuster to request specific items, provide a comprehensive initial submission including estimates from licensed contractors, medical records, receipts for emergency repairs, and any relevant reports. Tampa claimants who front-load documentation often shave 10-20 days off their timelines.

Respond to requests immediately.When your adjuster asks for additional information, provide it within 24-48 hours. Delays in your response directly extend your overall timeline, as the 30-day coverage decision clock pauses until you submit requested materials.

Maintain detailed records.Keep a log of every communication with your insurance company, including dates, times, names of representatives, and discussion summaries. This documentation proves invaluable if disputes arise and helps you track whether your insurer is meeting Florida’s legal deadlines.

Consider professional representation.Complex claims often benefit from professional assistance.Public adjusters in Tampaunderstand local insurance practices, know how to compile compelling documentation, and can navigate the system more efficiently than most homeowners. Their expertise often results in faster settlements and higher payouts.

Why Do Some Tampa Insurance Claims Take Longer Than 90 Days?

Despite Florida’s 90-day guideline, many Tampa insurance claims extend well beyond this timeframe for legitimate and sometimes questionable reasons.

Severe injury casesnaturally require extended timelines because claimants shouldn’t settle before reaching maximum medical improvement. If you’re injured in a Tampa car accident, your attorney and insurer need complete medical documentation, long-term prognosis assessments, and final treatment costs before determining fair compensation. These cases commonly extend 6-12 months or longer.

Liability disputessignificantly extend timelines when fault isn’t clear. Multi-vehicle accidents on Tampa’s I-4 corridor, slip-and-fall cases with shared responsibility, or property damage with questionable causes all require thorough investigation, potentially involving expert witnesses, accident reconstructionists, or engineering reports.

According toFlorida insurance settlement laws, companies can extend timelines beyond 90 days when exceptional circumstances exist, including ongoing investigations or complex liability determinations.

Strategic delays by insurersrepresent a concerning reality. Insurance companies sometimes intentionally slow high-value claims, hoping claimants will accept lower settlements out of frustration or financial pressure. This practice is particularly common with claims approaching policy limits or involving significant damages.

Policy coverage disputesextend timelines when insurers question whether your policy actually covers the claimed damage. These disputes might involve exclusions, coverage limits, or questions about whether damage resulted from a covered peril. Resolving these disputes often requires legal interpretation of policy language.

Catastrophic eventscreate widespread delays throughout Tampa. When hurricanes, major storms, or other disasters affect the entire region, insurers invoke “extraordinary circumstances” provisions, effectively pausing normal timeline requirements while they manage overwhelming claim volumes.

How Do Hurricanes Affect Claim Timelines in Tampa?

Tampa’s location on Florida’s Gulf Coast makes hurricane impacts a critical consideration when estimating insurance claim timelines. These massive weather events fundamentally alter the claims landscape.

Following major hurricanes, Tampa insurance adjusters face unprecedented workloads. A single hurricane can generate thousands of claims across Hillsborough County within days, overwhelming local insurance resources. During these periods, claim timelines routinely extend to90-180 daysor longer as adjusters work through massive backlogs.

Florida law recognizes these challenges by allowing insurers to invoke “extraordinary circumstances” provisions following declared disasters. This essentially gives companies additional time beyond standard 90-day requirements, though they must still demonstrate good faith efforts to process claims efficiently.

Tampa homeowners filing hurricane claims should expect initial adjuster visits within 1-3 weeks post-storm, preliminary damage assessments within 30-45 days, and final settlements potentially taking 4-6 months depending on damage severity and regional claim volume. Complex structural damage requiring engineering assessments extends timelines further.

The 2024 hurricane season highlighted these challenges, with many Tampa Bay area residents still resolving claims months after storms passed. Insurance companies prioritize life-safety issues and severe structural damage, meaning less critical claims wait longer in the queue.

When Should You Hire a Public Adjuster in Tampa?

Certain situations strongly indicate you should consider professional assistance to navigate Tampa’s insurance claim process effectively.

Hire a public adjuster if your claim exceeds $10,000.Larger claims justify the professional fee through significantly improved settlement amounts.Public adjuster fees in Floridatypically range from 10% to 20% of your settlement, but their expertise often increases payouts by 30% to 50% or more, far exceeding their cost.

Complex damage assessments warrant professional help.If your Tampa property suffered structural damage, significant water intrusion affecting multiple systems, or hurricane damage with both wind and water components, a public adjuster’s technical expertise ensures nothing gets overlooked in damage assessments.

Disputes with your insurer signal the need for representation.If your insurance company denies your claim, offers an unreasonably low settlement, or questions coverage, a public adjuster or attorney levels the playing field. They understand Florida insurance law, know how to challenge unfair denials, and can escalate issues to the state Department of Financial Services if necessary.

Time constraints justify professional assistance.If you’re overwhelmed with work, live out of state, or simply don’t have time to manage the extensive documentation and communication required, hiring apublic adjusterremoves this burden while likely improving your outcome.

Tampa residents dealing withwater damage claimsor other complex property issues often find that professional adjusters not only speed the process but also secure substantially higher settlements than they could achieve independently.

Key Takeaways

- Standard timelines:Most insurance claims in Tampa resolve within 30-90 days, with simple property and auto claims on the shorter end and complex injury cases extending beyond 90 days.

- Florida legal requirements:Insurers must acknowledge claims within 14 days, issue coverage decisions within 30 days of receiving complete documentation, and provide final payment or denial within 90 days unless exceptional circumstances exist.

- Documentation is critical:Complete, professional documentation submitted upfront significantly accelerates claim processing and often results in higher settlements.

- Hurricane impacts:Major weather events in Tampa dramatically extend timelines to 90-180+ days due to overwhelming claim volumes affecting local adjusters.

- Strategic delays occur:High-value claims sometimes face intentional delays from insurers hoping claimants will accept lower settlements, particularly for severe injuries or claims approaching policy limits.

- Professional help matters:Public adjusters and attorneys often expedite complex claims while securing 30-50% higher settlements, particularly for claims exceeding $10,000 or involving disputes.

- Take immediate action:Filing promptly, documenting thoroughly, and responding quickly to adjuster requests can shave weeks off your Tampa insurance claim timeline.

People Also Ask

How long does it take to get a settlement in Tampa after a car accident?

Simple car accident settlements in Tampa typically take30-45 daysfor PIP claims and60-90 daysfor third-party liability cases. Complex accidents involving severe injuries or disputed fault often extend beyond 90 days and may take several months to resolve fully.

Can an insurance company delay my claim indefinitely in Tampa?

No, Florida law prevents indefinite delays by requiring coverage decisions within 30 days and final payment within 90 days. However, insurers can extend timelines beyond 90 days by claiming “exceptional circumstances” such as ongoing investigations, catastrophic events, or complex liability determinations that require additional time to resolve properly.

What happens if my Tampa insurer doesn’t respond in 30 days?

While Florida law requires responses within 30 days, no automatic penalty occurs for missed deadlines. You can file a complaint with the Florida Department of Financial Services, pursue legal action for bad faith if delays are unreasonable, or hire a public adjuster or attorney to escalate your claim and pressure the insurer to act.

Does my Tampa claim take longer if I have severe injuries?

Yes, severe injury claims routinely extend beyond 90 days because you shouldn’t settle before reaching maximum medical improvement. Insurers need complete treatment records, long-term prognosis assessments, and final cost calculations. These claims commonly take 6-12 months or longer, particularly with high policy limits or disputed liability.

How do I know if my Tampa insurance claim is taking too long?

Your claim likely faces unreasonable delays if: your insurer hasn’t acknowledged it within 14 days, hasn’t issued a coverage decision 30+ days after receiving complete documentation, or hasn’t provided payment/denial within 90 days without valid exceptional circumstances. Document all communications and consider filing a state complaint or hiring professional representation.

Will hiring a Tampa public adjuster speed up my claim?

Public adjusters often expedite claims by submitting complete, professional documentation upfront and navigating insurance company processes efficiently. While they can’t override legal timelines, their expertise eliminates common delays caused by incomplete submissions, documentation issues, or communication problems that typically extend claim processing times by weeks.

Frequently Asked Questions

What is the average time for a Tampa property insurance claim to be paid?+

Most Tampa property insurance claims are paid within45-90 daysfrom the initial filing date. Simple claims like minor water damage or theft may resolve in 30-45 days, while more complex hurricane damage or structural issues typically take 60-90 days or longer depending on damage extent and documentation completeness.

How long do I have to file an insurance claim in Tampa after damage occurs?+

While Florida law doesn’t specify an exact deadline for reporting damage, most insurance policies require prompt notification, typically within days to weeks of discovering damage. For best results, file your Tampa claim within 24-72 hours of the incident to ensure timely processing and avoid potential coverage disputes about delayed reporting.

What should I do if my Tampa insurance claim is denied?+

If your Tampa claim is denied, request a detailed written explanation from your insurer, review your policy to understand the denial basis, and gather additional evidence supporting your claim. Consider hiring a public adjuster or insurance attorney to challenge the denial, file an appeal with your insurance company, or submit a complaint to the Florida Department of Financial Services.

Do Tampa auto insurance claims take less time than property claims?+

Generally yes, simple Tampa auto insurance claims often resolve faster than property claims, typically within 30-45 days for straightforward accidents. However, auto claims involving severe injuries, multiple parties, or liability disputes can take just as long or longer than property claims, sometimes extending 90 days or several months.

Can I make emergency repairs before the adjuster sees my Tampa property damage?+

Yes, you should make necessary emergency repairs to prevent further damage to your Tampa property, but document everything thoroughly first with photos and videos. Save all receipts for emergency repairs, as your insurance policy typically covers reasonable costs to prevent additional damage even before the adjuster’s inspection.

What happens if I disagree with my Tampa insurance adjuster’s damage estimate?+

If you disagree with your adjuster’s estimate, obtain independent estimates from licensed Tampa contractors, document all damage thoroughly with photos and videos, and submit this evidence to your insurer requesting reconsideration. Many Tampa policyholders hire public adjusters to provide professional damage assessments and negotiate better settlements when disputes arise.

How much do public adjusters charge in Tampa for insurance claims?+

Related:How to Navigate the Water Damage Insurance Claim Process in Tampa: A Complete 2026 Guide

Related:Public Adjuster Colorado in Florida: Complete 2026 Cross-State Licensing and Practice Guide

Public adjusters in Tampa typically charge10% to 20%of your final settlement amount, with fees varying based on claim complexity, damage extent, and whether the claim is still open or already denied. The investment often pays for itself through significantly higher settlements, with many clients receiving 30-50% more than initial insurance company offers. Learn more abouthow public adjusters get paid in Florida.