How Does a Public Adjuster Get Paid in Florida: Complete 2026 Fee Structure Guide

Quick Answer

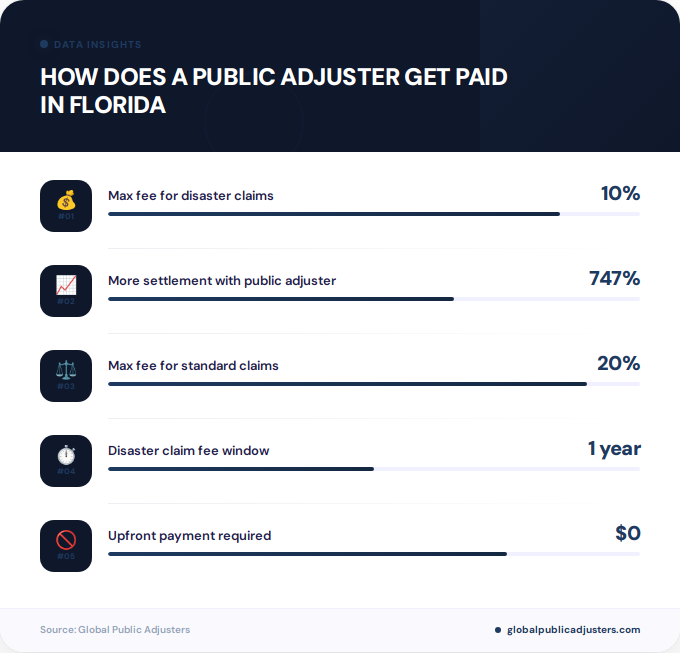

In Florida, public adjusters are paid through a contingency fee structure, receiving a pre-arranged percentage of only the “new money” they recover for policyholders. Florida law caps these fees at10% for disaster claims filed within one yearand20% for standard claims, with payment occurring only after the insurance company settles the claim and issues payment.

When your home in Miami, Orlando, Tampa, or anywhere across Florida suffers damage from a hurricane, fire, or water incident, understanding how does a public adjuster get paid in Florida becomes critical before signing any contract. Unlike company adjusters who work for insurance carriers, public adjusters representyou, the policyholder, and their compensation structure reflects this fundamental difference.

Here’s a surprising fact:policyholders who hire a public adjuster receive 747% more in settlement fundsthan those who navigate claims alone, according torecent industry research on public adjuster value. Despite this dramatic increase in recovery, many Florida homeowners remain unclear about the fee structure, legal protections, and payment timing that govern these professional relationships.

This comprehensive guide examines exactly how public adjusters are compensated in Florida, the state-mandated fee caps enacted to protect consumers, and what you can expect when youwork with a public adjuster to maximize your insurance settlement.

What Is the Contingency Fee Model for Public Adjusters?

The contingency fee model represents the cornerstone of how does a public adjuster get paid in Florida. Under this arrangement, the adjuster receivesno upfront payment, retainer, or hourly billing. Instead, their compensation is entirely contingent on successfully recovering additional funds from your insurance company.

This payment structure creates a powerful alignment of interests. The adjuster only benefits when you benefit, and the more they recover on your behalf, the higher their compensation. This model removes financial barriers for policyholders who might not have liquid assets to pay hourly consultants during a crisis.

Unlike attorney contingency fees that might range from 33% to 40% in personal injury cases, Florida strictly regulates public adjuster percentages throughstate statutes governing public adjuster compensation limits. These caps ensure fair compensation while preventing excessive fees during vulnerable times.

How Does Florida Law Cap Public Adjuster Fees?

Florida Statutes Section 626.854 establishes strict maximum percentages that public adjusters can charge based on the nature and timing of your claim. These regulations protect consumers while ensuring adjusters are fairly compensated for their expertise.

| Claim Type | Maximum Fee | Timing Requirements |

|---|---|---|

| Standard Claims | 20% | No specific deadline |

| Disaster Claims (State of Emergency) | 10% | Within 1 year of loss date |

| Supplemental Claims | 20% | On new recovery only |

| Post-Emergency Period Claims | 20% | After 1-year disaster window |

The10% cap for disaster claimsapplies when the Governor declares a state of emergency, which frequently occurs during hurricane season across coastal cities like Tampa, Fort Myers, and West Palm Beach. This reduced rate recognizes the widespread impact of catastrophic events and provides relief to affected communities.

According toFlorida’s Department of Financial Services guidelines for public adjusters, any contract that exceeds these statutory limits is unenforceable, and adjusters who violate these caps face disciplinary action, including license suspension or revocation.

What Does “New Money” Mean in Public Adjuster Compensation?

The “new money” principle represents a critical consumer protection embedded in Florida public adjuster law. This concept means adjusters canonly charge their percentage on additional funds they recover, not on money the insurance company already agreed to pay before you retained their services.

For example, if your insurance company initially offered a $50,000 settlement and your public adjuster negotiates a final settlement of $125,000, the adjuster’s fee applies only to the$75,000 in new moneythey secured. At the standard 20% rate, the fee would be $15,000, leaving you with $110,000 total, compared to the original $50,000 you would have received.

This structure proves especially valuable for supplemental or reopened claims. Many Florida homeowners discover additional damage months after initial settlements, particularly withwater damage claims that reveal hidden issues over time. The 20% fee applies exclusively to the supplemental recovery, not the original settlement amount.

When Does a Public Adjuster Get Paid in Florida?

Understanding when payment occurs is as important as understanding how does a public adjuster get paid in Florida. The payment timeline follows a strict “pay when you pay” model that protects policyholders from upfront financial risk.

The public adjuster receives no payment until:

- The insurance company issues a final settlement decision

- The insurance carrier cuts the settlement check

- The policyholder receives their funds

In most cases, the insurance company lists the public adjuster as aco-payee on the settlement check. This means the check requires endorsement from both you and your adjuster before it can be deposited. The adjuster deducts their contractual percentage, then forwards your portion directly to you.

This co-payee arrangement, detailed inFlorida Statute 626.854 governing adjuster contracts, provides transparency and ensures both parties receive their agreed-upon amounts simultaneously. The process typically takes 2 to 6 weeks from final settlement approval to check issuance, depending on the insurance carrier’s payment procedures.

For clients working with adjusters in Jacksonville, Orlando, or Miami on complex claims involving multiple policy coverages, payment may occur in stages as different aspects of the claim are settled. Each payment follows the same co-payee process, with the adjuster’s percentage calculated on each disbursement.

How Much Do Public Adjusters Actually Earn in Florida?

While the fee structure explains how does a public adjuster get paid in Florida, understanding actual earnings provides context for evaluating the profession and what to expect from your adjuster’s experience level. Income varies significantly based on caseload, claim complexity, and years in practice.

Hourly Equivalent:$23.33/hour

Source: 2026 Industry Data

Includes bonuses and profit-sharing

Varies by firm and location

Building client relationships

Developing expertise

Depends on firm structure

Training and mentorship included

According tocomprehensive Florida public adjuster salary data compiled in 2026, six-figure incomes typically require several years of relationship-building and proven value. Experienced adjusters in high-demand markets like Orlando and Tampa often exceed $100,000 annually through a combination of high-value claims and efficient case management.

Geographic location significantly impacts earnings. Top-paying Florida cities for public adjusters include:

- Orlando: High volume of property claims, diverse housing stock

- Miami: Complex high-value properties, frequent weather events

- Tampa: Growing market, coastal property exposure

The initial investment to become licensed remains relatively modest. Licensing costs in Florida total approximately$710, covering application fees, surety bond, examination, license issuance, background check, and appointment fees. This accessible entry point attracts professionals from construction, insurance, and real estate backgrounds.

What’s the Difference Between Disaster and Standard Claim Fees?

The distinction between disaster and standard claims creates significant practical differences in how does a public adjuster get paid in Florida. Understanding this difference helps policyholders anticipate costs based on their specific situation.

Disaster Claims (10% fee cap):

Disaster claims arise when the Governor declares a state of emergency, typically following hurricanes, tropical storms, or widespread catastrophic events. Florida’s hurricane-prone geography means coastal residents from Pensacola to Key West frequently experience these declarations.

The reduced 10% fee reflects both consumer protection during widespread crisis and the typically higher claim volumes adjusters handle during disaster periods. For a $200,000 hurricane damage settlement, the adjuster would receive $20,000 under the disaster rate, compared to $40,000 under standard rates.

Critically, the 10% rate only applies if you retain the adjusterwithin one year of the loss date. If you wait longer than 12 months to hire representation, the claim reverts to the standard 20% cap, even if it originated from a declared disaster.

Standard Claims (20% fee cap):

Standard claims include all non-disaster losses such as isolated fires, burst pipes, theft, vandalism, or individual property damage incidents. These claims don’t involve gubernatorial emergency declarations and follow the 20% maximum fee structure.

Many policyholders working with adjusters onwater damage claims in Orlandoor fire damage cases throughout Florida fall under this standard category. The higher percentage reflects the typically lower claim volume and individualized attention these cases require.

Why Do Policyholders Still Come Out Ahead Despite Fees?

The mathematical reality of public adjuster representation consistently demonstrates that policyholders receive substantially more money even after paying the contingency fee. This value proposition addresses the common concern about whether the fees are “worth it.”

Research indicates policyholders hiring public adjusters recover747% more in settlement fundsthan those navigating claims independently. This dramatic difference stems from several factors:

- Expert damage assessment:Adjusters identify damage that untrained eyes miss

- Policy interpretation:Professional understanding of coverage triggers and exclusions

- Documentation expertise:Proper evidence compilation that satisfies carrier requirements

- Negotiation experience:Proven strategies for maximizing settlements

- Time investment:Full-time focus that most policyholders cannot match

Consider a real-world scenario: Your insurance company offers $75,000 for hurricane damage. You hire a public adjuster who negotiates a $225,000 settlement. At the 10% disaster rate, you pay $22,500 in fees but receive $202,500, net gain of$127,500 more than the original offer.

Even at the standard 20% rate, the mathematics favor professional representation. For policyholders dealing withcomplex property damage claims that require extensive documentation, the adjuster’s expertise translates directly into recovered dollars that far exceed their fees.

How Do Public Adjuster Rates Vary Across Florida Cities?

While Florida law sets maximum fee caps uniformly across the state, practical variations emerge based on regional market conditions, claim complexity, and local property values. Understanding these geographic nuances helps set realistic expectations regardless of your location.

Major Metropolitan Areas:

Orlando, Miami, Tampa, and Jacksonville represent Florida’s largest markets for public adjusters. These cities experience high claim volumes, diverse property types, and competitive adjuster markets. Most adjusters in these areas charge at or near the statutory maximums (10% for disasters, 20% for standard claims) due to high demand and complex urban property portfolios.

Miami’s unique condominium market and high-rise properties create specialized expertise requirements. Adjusters handling these claims often maintain the full 20% rate due to the intricate nature of association policies, shared building elements, and multiple coverage layers.

Coastal Communities:

Cities like Fort Lauderdale, Naples, Clearwater, and Sarasota face frequent hurricane exposure, creating consistent demand for disaster claim expertise. The 10% emergency rate typically applies during active hurricane seasons, though adjusters may negotiate toward the higher end of permissible ranges for particularly complex coastal properties.

Central and North Florida:

Inland communities experience different loss patterns, with more fire, theft, and non-weather-related claims falling under standard 20% rates. Competition among adjusters in these markets sometimes leads to negotiated rates below statutory maximums, particularly for straightforward claims with clear liability.

When evaluating how does a public adjuster get paid in Florida relative to your location, focus less on regional rate variations (which remain constrained by statute) and more on the adjuster’s specific experience with your property type and loss cause. An adjuster atGlobal Public Adjusterswith proven expertise in your claim category delivers better value than a lower-cost generalist.

People Also Ask

Can I negotiate a public adjuster’s fee below the statutory maximum?

Yes, public adjuster fees are negotiable within the statutory caps. While many adjusters charge the maximum permitted rates, you can propose lower percentages, particularly for straightforward claims or high-value settlements where even a reduced percentage yields substantial compensation for the adjuster’s work.

Do public adjusters charge upfront fees or retainers in Florida?

No, legitimate Florida public adjusters work exclusively on contingency and cannot charge upfront fees, retainers, or hourly rates. Any adjuster requesting payment before settling your claim violates Florida regulations and should be reported to the Department of Financial Services.

What happens if my public adjuster doesn’t recover any additional money?

If your public adjuster fails to secure any new money beyond what the insurance company already offered, you owe them nothing under the contingency fee structure. This no-recovery, no-fee arrangement protects policyholders from financial risk when hiring representation.

Are public adjuster fees tax-deductible in Florida?

Public adjuster fees may be tax-deductible as miscellaneous expenses related to determining a casualty loss, though specific deductibility depends on your tax situation and whether you itemize deductions. Consult a tax professional for guidance specific to your circumstances and the current tax code.

How long does it take for a public adjuster to get paid after settlement?

Public adjusters typically receive payment within 2 to 6 weeks after the insurance company issues the settlement check, as they are listed as co-payees on the payment. The timeline depends on the carrier’s processing speed and how quickly both parties endorse and deposit the check.

Can a public adjuster charge different rates for different types of claims?

No, Florida law establishes maximum percentages based on claim timing and disaster declarations, not claim type. An adjuster cannot charge 15% for fire claims and 20% for water claims, all standard non-disaster claims fall under the same 20% maximum regardless of the cause of loss.

Frequently Asked Questions

What is the maximum a public adjuster can charge in Florida?+

Florida law caps public adjuster fees at 10% for disaster claims filed within one year of the loss date and 20% for all standard non-disaster claims. These maximums apply to the total settlement amount or new money recovered, and any contract exceeding these limits is unenforceable under Florida Statute 626.854.

Do I pay my public adjuster if the insurance company denies my claim?+

No, you owe nothing to your public adjuster if your claim is denied and no settlement is recovered. The contingency fee structure means payment only occurs when you receive funds from the insurance company. If you later appeal the denial successfully with the adjuster’s continued assistance, their fee would apply to that eventual recovery.

Can I cancel my public adjuster contract if I’m unhappy with their service?+

Florida provides a 3-business-day rescission period after signing a public adjuster contract during which you can cancel without penalty. After this period, cancellation terms depend on your contract provisions, though most agreements allow termination with written notice. If settlement occurs after you terminate, fees may still apply based on the adjuster’s contribution to the final recovery.

How does the co-payee process work when my public adjuster gets paid?+

The insurance company issues a settlement check listing both you and your public adjuster as payees, requiring both signatures for deposit. Your adjuster typically handles the deposit, deducts their contractual percentage, then issues you a check for your portion. This transparent process ensures both parties receive their agreed amounts simultaneously and provides a clear paper trail of the transaction.

What qualifies as a disaster claim for the 10% fee cap in Florida?+

A disaster claim qualifies for the reduced 10% fee when the Florida Governor issues a state of emergency declaration covering your area and you retain the adjuster within one year of the loss date. These declarations typically follow hurricanes, tropical storms, or widespread catastrophic events. Individual isolated losses do not qualify regardless of severity.

Should I hire a public adjuster immediately after damage or wait for the insurance company’s offer?+

Hiring a public adjuster immediately after damage typically yields better results than waiting for an initial offer, as they document the loss properly from the start, prevent common policyholder mistakes, and establish the full scope of damage before repairs begin. Early involvement also ensures you meet disaster claim timing requirements if applicable and strengthens your negotiating position throughout the process.

Are there circumstances where public adjuster fees exceed statutory caps?+

No, Florida law prohibits public adjusters from charging fees exceeding statutory caps under any circumstances. Contracts with higher percentages are void and unenforceable. If an adjuster charges above the 10% disaster cap or 20% standard cap, you can file a complaint with the Florida Department of Financial Services, which may result in disciplinary action against the adjuster’s license.

Key Takeaways: Understanding How Public Adjusters Get Paid in Florida

- Contingency-only payment:Florida public adjusters receive no upfront fees, retainers, or hourly charges, they are paid exclusively through a percentage of the settlement they secure for you.

- Statutory fee caps protect consumers:Florida law limits fees to 10% for disaster claims filed within one year and 20% for all standard claims, with contracts exceeding these limits being unenforceable.

- “New money” principle:Adjusters only charge fees on additional funds they recover beyond what the insurance company initially offered, ensuring you never pay for settlements you would have received anyway.

- Co-payee payment process:Insurance companies list adjusters on settlement checks, requiring both signatures and creating transparent documentation of the fee deduction and your net recovery.

- Proven value proposition:Research shows policyholders hiring public adjusters recover 747% more in settlement funds, meaning net recovery after fees dramatically exceeds independent claim handling results.

- Geographic considerations:While state law standardizes maximum rates, adjuster expertise in your specific property type and loss cause matters more than location when evaluating representation value.

- No recovery, no fee guarantee:If your adjuster fails to secure additional settlement funds, you owe nothing, eliminating financial risk from professional representation during the claims process.

Get Expert Public Adjuster Representation for Your Florida Claim

Understanding how does a public adjuster get paid in Florida is just the first step. The real question is whether you’re maximizing your insurance settlement or leaving thousands of dollars on the table. With our proven track record of recovering 747% more for policyholders than they would receive independently, our contingency fee structure means you only win when you win.

Whether you’re dealing with hurricane damage in Miami, water damage in Orlando, fire loss in Tampa, or any property claim throughout Florida, our licensed public adjusters provide expert representation with transparent fees capped by state law. We handle everything from initial damage assessment through final settlement negotiation.