When to Hire a Public Adjuster in Florida: Complete 2026 Guide

Quick Answer

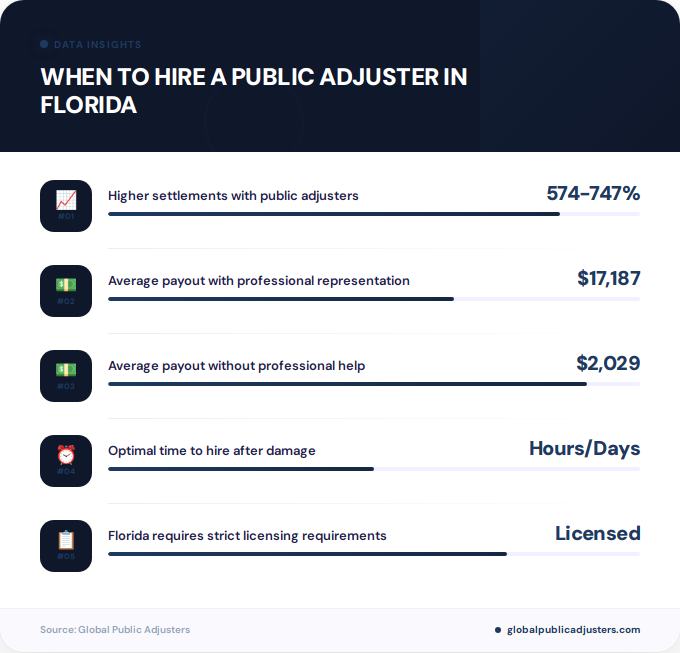

You should hire a public adjuster in Florida immediately after discovering property damage, especially for large or catastrophic losses like hurricanes, fires, or major flooding. Data shows policyholders using public adjusters receive 574% to 747% higher settlements, with disaster claims averaging $17,187 versus just $2,029 for those who go it alone.

Imagine filing an insurance claim after a hurricane damages your Miami home, only to receive a settlement offer that covers barely a fraction of your actual losses. You’re not alone. Thousands of Florida property owners face this exact scenario every year, leaving money on the table simply because they navigated the claims process without professional representation.

The decision ofwhen to hire a public adjuster in Floridacan literally mean the difference between a $2,029 settlement and a $17,187 payout on the same claim. These aren’t hypothetical numbers, they’re actual statistical averages from Florida’s public adjuster industry data. Understanding the critical timing windows, regulatory frameworks, and strategic advantages of professional claims representation can transform your insurance recovery experience.

This comprehensive guide breaks down exactly when Florida property owners should engage a public adjuster, backed by the latest 2026 regulatory updates, real financial impact data, and expert insights from industry professionals across the state.

What Is a Public Adjuster and How Do They Work in Florida?

Apublic adjusteris a licensed professional who represents policyholders, not insurance companies, in the property claims process. Unlike company adjusters who work for your insurer, public adjusters are your advocate, working exclusively to maximize your settlement.

In Florida, public adjusters must meet stringent licensing requirements that includestate-mandated apprenticeships and examinationsnot found in most other states. These professionals handle everything from damage assessment and documentation to negotiating directly with insurance companies on your behalf.

The Florida public adjuster landscape operates under strict ethical standards, with consistently low complaint rates reflecting the profession’s commitment to quality representation. When you hire a licensed public adjuster, you’re accessing specialized expertise in policy interpretation, damage valuation, and insurance law specific to the Sunshine State’s unique property challenges.

When Is the Optimal Time to Hire a Public Adjuster in Florida?

The single most important answer towhen to hire a public adjuster in Floridais simple:as soon as possible after discovering damage. Unlike what many property owners believe, you don’t need to wait until you’ve filed a claim or received an initial settlement offer.

Industry experts consistently recommend engaging a public adjuster immediately after experiencing a loss, even before filing your claim. This early intervention allows the adjuster to properly document damage, prevent evidence loss, and position your claim for maximum recovery from day one.

For homeowners inOrlando, Tampa, Jacksonville, and throughout Florida, this means contacting a public adjuster within hours or days of damage occurrence, not weeks or months later. Thedecision to hire a public adjuster in Orlandoshould be made during your initial damage assessment, not after accepting a lowball offer.

Critical Timing Windows for Different Claim Types

Why: Evidence preservation is critical; damage can worsen; competition for adjusters increases

Why: Fire scenes change rapidly; structural issues emerge; insurance companies respond fast

Why: Mold develops within 24-48 hours; secondary damage spreads; policy coverage questions arise

Why: Complex assessment needed; disputes over causation common; hidden damage requires expertise

For Florida residents dealing with water damage specifically, understandingspecialized water damage claim procedurescan be crucial to your recovery timeline.

What Do the Numbers Show? The Financial Impact of Hiring a Public Adjuster

The financial data supporting public adjuster representation is overwhelming. According tocomprehensive industry statistics compiled by the Florida Association of Public Insurance Adjusters, the settlement differences are dramatic and consistent.

| Claim Type | With Public Adjuster | Without Public Adjuster | Difference |

|---|---|---|---|

| Non-Disaster Claims | $9,379 | $1,391 | 574% higher |

| Catastrophic/Hurricane Claims | $17,187 | $2,029 | 747% higher |

These numbers represent actual claim outcomes from Florida policyholders. For a typical hurricane claim inTampaorMiami, the difference between handling it yourself and hiring a professional can exceed$15,000or more on a single claim.

The question isn’t whether hiring a public adjuster makes financial sense, it’s whether you can afford not to, especially on claims exceeding $10,000 in estimated damage. Even after paying the adjuster’s fee, policyholders consistently come out significantly ahead.

Which Types of Claims Benefit Most from Public Adjusters?

While virtually any property claim can benefit from professional representation, certain scenarios create particularly strong cases forwhen to hire a public adjuster in Florida.

Large or Catastrophic Loss Claims

Hurricane damage, complete roof replacements, fire losses, and major flooding events represent the highest-stakes claims where professional representation delivers maximum value. For these catastrophic events, the complexity of damage assessment, policy interpretation, and negotiation requires specialized expertise.

Florida homeowners facing these scenarios should consider hiring a public adjuster before even contacting their insurance company. The adjuster can guide initial documentation, prevent critical mistakes, and establish a strong foundation for your claim from the outset.

Disputed or Denied Claims

If your insurance company has disputed coverage, denied your claim, or offered a settlement that seems unreasonably low,this is exactly when you need professional representation. Public adjusters specialize in these challenging situations, bringing policy expertise and negotiation skills that level the playing field.

Many Florida property owners don’t realize they can appeal denied claims or challenge lowball offers. A public adjuster transforms a seemingly final decision into a negotiable position, often recovering substantial settlements on claims that initially appeared hopeless.

Complex Commercial Property Claims

Business owners inJacksonville,Orlando, and throughout Florida face unique challenges with commercial property claims. These involve business interruption calculations, inventory losses, equipment damage, and complex policy provisions that require professional interpretation.

For commercial claims, hiring a public adjuster isn’t just recommended, it’s practically essential. The financial stakes and complexity justify professional representation in virtually every scenario.

What Are the 2026 Florida Regulations and Fee Structures?

Florida maintains some of the nation’s most comprehensive public adjuster regulations, recently updated with significant changes affecting both fees and timelines. Understanding these2026 statutory requirements under Florida Statute 626.854helps property owners make informed decisions.

Current Fee Caps and Structure

| Claim Type | Maximum Fee | Timeline |

|---|---|---|

| Disaster Claims (State of Emergency) | 10% | Within 1 year of loss |

| Non-Disaster/Standard Claims | 20% | All standard claims |

These fees are calculated as a percentage of the total claim payment you receive, meaning the adjuster only gets paid when you get paid. This contingency structure aligns incentives perfectly: your adjuster’s compensation directly depends on maximizing your settlement.

For detailed information about costs and fee structures, Florida property owners can review comprehensive guides onhow public adjusters get paid in Florida.

New Timeline Requirements

The 2026 statute also reduced claim supplement timelines significantly. Public adjusters now have12 monthsfor new claims and18 monthsfor existing claims from the date of loss to file supplemental claims. This compressed timeline makes early hiring even more critical.

Consumer Protections

Florida law provides strong consumer protections when hiring a public adjuster:

- 10-day cooling-off period: You can cancel any public adjuster contract within 10 days of signing with no penalty

- 30-day emergency cancellation: For claims tied to a state of emergency, you have 30 days from the loss date to cancel

- Required licensing: All public adjusters must maintain active Florida licenses and carry errors and omissions insurance

- Written contracts: All agreements must be in writing with clear fee disclosures

What Warning Signs Indicate You Need a Public Adjuster Now?

Certain situations create immediate red flags suggesting you should hire a public adjuster in Florida without delay. Recognizing these warning signs can prevent significant financial losses.

Your Insurance Company Is Delaying or Avoiding Communication

If your insurer takes weeks to respond to calls, misses inspection appointments, or repeatedly requests the same documentation, these delay tactics often indicate they’re hoping you’ll accept a low offer out of frustration. A public adjuster cuts through these stalling tactics with professional pressure and formal communication protocols.

The Initial Settlement Offer Seems Unreasonably Low

Insurance companies often make lowball initial offers testing whether you’ll accept without question. If your gut tells you the offer doesn’t come close to covering your actual losses, trust that instinct. Public adjusters specialize in challenging these inadequate offers with detailed documentation and expert valuation.

Your Claim Involves Multiple Types of Damage

When a single event causes roof damage, water intrusion, structural issues, and interior damage, the complexity multiplies exponentially. These multi-faceted claims require comprehensive assessment and documentation that most property owners can’t provide without professional help.

The Insurance Company Questions Causation or Coverage

If your insurer suggests that your damage isn’t covered under your policy, occurred before the policy period, or resulted from maintenance issues rather than a covered peril, you’re facing policy interpretation disputes that demand professional expertise. These coverage disputes represent exactly when to hire a public adjuster in Florida.

For property owners facing claim denials, understanding theappeal process and representation optionsbecomes critical to protecting your rights.

How Do You Hire a Public Adjuster in Florida?

The process of engaging a public adjuster in Florida follows clear steps designed to protect both parties and ensure professional standards.

Step 1: Research and Verify Licensing

Always verify your public adjuster holds an active Florida license through the Department of Financial Services. Licensed adjusters have met stringent education, experience, and examination requirements. TheNational Association of Public Insurance Adjusters provides searchable directoriesof qualified professionals.

Step 2: Initial Consultation

Most public adjusters offer free initial consultations to evaluate your claim and explain their services. During this meeting, discuss the scope of damage, policy coverage, and the adjuster’s experience with similar claims. Ask about their success rate, typical timelines, and communication protocols.

Step 3: Review and Sign the Contract

Read the public adjuster contract carefully, ensuring you understand the fee structure, services included, and cancellation terms. Florida law requires contracts to be in writing with clear fee disclosures. Don’t sign until you’re completely comfortable with all terms.

Step 4: Document and Assess

Once hired, your public adjuster will comprehensively document your property damage, review your insurance policy, and develop a claim strategy. This includes photographing damage, compiling repair estimates, and identifying all applicable coverage provisions.

Step 5: File and Negotiate

The adjuster prepares and submits your claim to the insurance company, then handles all subsequent communication and negotiation. You’ll receive regular updates on progress and settlement offers, with final decisions always remaining in your control.

ForOrlandohomeowners specifically seeking local expertise, connecting withexperienced Florida public adjusterswho understand regional challenges can make a significant difference in claim outcomes.

Is It Ever Too Late to Hire a Public Adjuster?

Many Florida property owners wonderwhether timing limits exist for engaging professional representation. The answer depends on your specific situation and where you are in the claims process.

Before Settlement: Almost Never Too Late

As long as your claim remains open and unsettled, hiring a public adjuster remains a viable option. Even if you’ve been negotiating for months, a fresh professional perspective can often unlock additional recovery that seemed impossible.

After Partial Settlement: Sometimes Possible

If you’ve accepted a partial settlement but believe additional damage exists or was undervalued, public adjusters can sometimes file supplemental claims. However, this becomes more challenging once you’ve signed releases or final settlement agreements.

After Final Settlement: Very Limited Options

Once you’ve accepted a final settlement and signed a release, options become extremely limited. Some scenarios involving newly discovered damage or insurance company fraud might allow reopening, but these represent rare exceptions.

The clear takeaway: the earlier you hire a public adjuster, the more options and leverage you maintain. Waiting until after settlement severely restricts what even the best professional can accomplish.

Key Takeaways

- Hire immediately after damage occurs: The optimal time to hire a public adjuster in Florida is within 24-48 hours of discovering property damage, before filing your claim

- Financial impact is substantial: Florida data shows 574% to 747% higher settlements for policyholders using public adjusters, depending on claim type

- Fee structures are regulated: 2026 Florida law caps fees at 10% for disaster claims (within one year) and 20% for non-disaster claims, paid only when you receive payment

- Large and disputed claims benefit most: Hurricane damage, fire losses, denied claims, and complex commercial properties see the greatest value from professional representation

- Strong consumer protections exist: Florida provides 10-day cooling-off periods and 30-day emergency cancellation rights on all public adjuster contracts

- Verify licensing always: Only work with Florida-licensed public adjusters who meet state education, experience, and examination requirements

- Earlier is always better: While hiring a public adjuster after settlement is sometimes possible, early engagement provides maximum leverage and recovery potential

People Also Ask

Can I hire a public adjuster before filing an insurance claim?

Yes, hiring a public adjuster before filing is actually ideal timing. They can guide initial documentation, help you understand policy coverage, and ensure your claim is properly structured from the start for maximum recovery potential.

Do public adjusters work for insurance companies?

No, public adjusters represent only policyholders, never insurance companies. Company adjusters work for insurers, while public adjusters are your advocate, paid by you to maximize your settlement rather than minimize the insurer’s payout.

How long does the public adjuster claims process take in Florida?

Timeline varies by claim complexity, but most Florida claims with public adjusters resolve within 30 to 120 days. Complex claims or those involving litigation may extend longer, while straightforward claims can settle in as little as a few weeks.

Can I switch to a public adjuster after starting with my insurance company?

Yes, you can hire a public adjuster at any point before final settlement, even if you’ve already been working directly with your insurance company. Many policyholders engage public adjusters after receiving lowball initial offers or experiencing communication problems.

What happens if I’m not satisfied with my public adjuster?

Florida law provides a 10-day cooling-off period to cancel any public adjuster contract without penalty. For disaster-related claims, you have 30 days from the loss date to cancel. After these periods, contract terms govern the relationship, though ethical adjusters will work to resolve any dissatisfaction.

Are public adjuster fees worth it for small claims?

For claims under $5,000, the cost-benefit calculation becomes more marginal. However, even on smaller claims, Florida data shows public adjusters recover significantly more than the fee costs. The decision depends on claim complexity, your comfort with the process, and whether coverage disputes exist.

Frequently Asked Questions

What is the difference between a public adjuster and a claims adjuster?+

A claims adjuster (or company adjuster) works for the insurance company and represents their interests in minimizing payouts. A public adjuster works exclusively for you, the policyholder, and is paid to maximize your settlement. They serve opposite sides in the negotiation process.

How much does a public adjuster cost in Florida?+

Florida law caps public adjuster fees at 10% of your settlement for disaster claims filed within one year of the loss, and 20% for non-disaster claims. Fees are contingency-based, meaning you pay nothing unless you receive a settlement. The percentage is calculated on your total claim payment.

Can a public adjuster reopen a closed claim?+

In limited circumstances, yes. If newly discovered damage emerges that wasn’t apparent during initial settlement, or if the insurance company engaged in fraud or bad faith, reopening may be possible. However, once you’ve signed a final release, options become very restricted, making early hiring crucial.

What should I look for when choosing a public adjuster in Florida?+

Verify active Florida licensing, check experience with your specific claim type, ask for references from recent clients, ensure they carry errors and omissions insurance, and review their fee structure carefully. Local experience in your area (Orlando, Tampa, Miami, Jacksonville) can also provide valuable regional expertise.

Will hiring a public adjuster delay my claim settlement?+

Not typically. While thorough documentation and negotiation take time, public adjusters often accelerate the process by submitting complete, professional claims that require less back-and-forth. The slightly longer timeline usually results in significantly higher settlements that more than justify the wait.

Do I need a public adjuster for water damage claims?+

Water damage claims frequently benefit from public adjuster representation because of complex coverage questions, rapid secondary damage development, and common disputes over causation and policy limits. Florida’s humidity makes water damage particularly complicated, often justifying professional assessment and negotiation.

What if my insurance company says I don’t need a public adjuster?+

Related:How Long Does an Insurance Claim Take in Tampa?

Related:How to Navigate the Water Damage Insurance Claim Process in Tampa: A Complete 2026 Guide

Insurance companies have a financial incentive to discourage public adjuster representation since it typically results in higher payouts. You have the absolute right to hire a public adjuster at any time, and insurance companies cannot penalize you or deny claims based on that decision. Trust your own judgment about whether you need professional help.