How Do Public Adjusters Get Paid in Florida: Complete 2026 Fee Structure Guide

Quick Answer

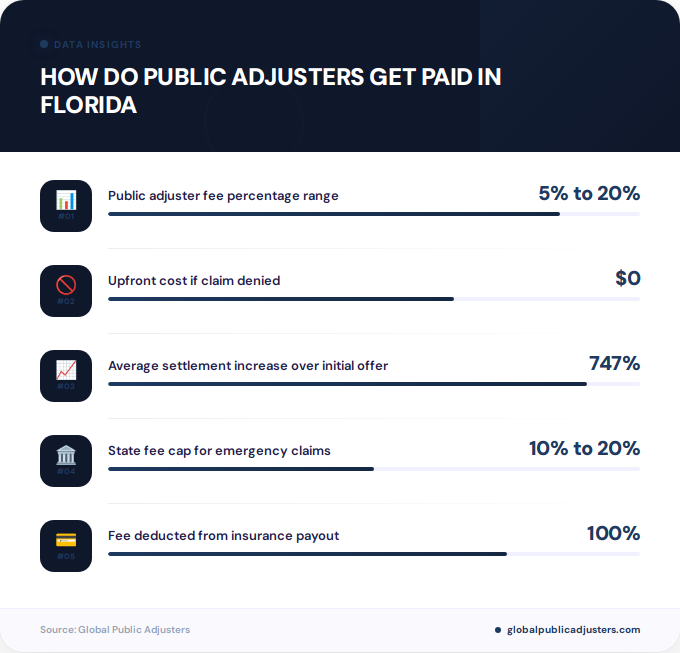

In Florida, public adjusters work on a contingency basis and get paid a pre-arranged percentage (typically 5% to 20%) of your final insurance settlement. You pay nothing upfront and owe nothing if your claim is denied. The state caps fees at 10% for declared emergencies during the first year and 20% for non-disaster claims.

Did you know that after Hurricane Ian devastated Southwest Florida in 2022, over65% of homeowners who used a public adjuster received settlement increases averaging 747% higherthan their initial insurance company offer? Yet many property owners across Jacksonville, Orlando, and Miami still hesitate to hire representation, primarily due to confusion about how do public adjusters get paid in Florida.

Understanding the payment structure for public adjusters is crucial before filing any significant property insurance claim. Unlike insurance company adjusters who work for the insurer,public adjusterswork exclusively for you, and their compensation model reflects this fundamental difference.

This comprehensive guide breaks down the exact fee structures, legal caps, and payment timelines governing public adjuster compensation in Florida for 2026 and 2027, helping you make an informed decision about professional claim representation.

What Is the Contingency Fee Model for Public Adjusters?

Public adjusters in Florida operate exclusively on acontingency fee basis, meaning they only get paid when you receive a settlement from your insurance company. This “no recovery, no fee” model aligns the adjuster’s financial interests directly with yours, creating a powerful incentive to maximize your claim payout.

Unlike attorneys who might charge hourly rates or require upfront retainers,public adjusters collect their fees as a percentage of the final settlement amount. This approach makes professional claim representation accessible to homeowners regardless of their immediate financial situation, which is especially important after disasters like hurricanes that impact communities from Tampa Bay to the Florida Keys.

The contingency model also provides significant consumer protection. If your claim is denied entirely or results in zero payout, you oweabsolutely nothingto the public adjuster. This risk-sharing arrangement means the adjuster only succeeds financially when you do, eliminating conflicts of interest that might exist in other payment structures.

How Are Public Adjuster Fees Structured in Florida?

When considering how do public adjusters get paid in Florida, the answer centers on percentage-based fees calculated from your total insurance settlement. The typical range varies from5% to 20%of the claim payment, depending on several factors including claim complexity, timing, and the type of loss event.

In practice, most experienced public adjusters in the Orlando, Jacksonville, and Miami metropolitan areas charge rates that regress or decrease as the settlement amount increases. For example, a$50,000 settlement might carry a 15% fee ($7,500), while a larger$500,000 settlement might be assessed at 10% ($50,000), reflecting economies of scale in the adjuster’s work.

Several factors influence where your specific fee falls within the legal range. Complex commercial claims involving multiple policy coverages typically command higher percentages than straightforward residential property damage. Similarly, claims filed long after the loss event may justify higher fees due to the additional investigative work required to document damages retrospectively.

For homeowners inFlorida communities frequently impacted by severe weather, understanding these fee dynamics helps set realistic expectations when engaging professional representation after hurricanes, tropical storms, or flooding events.

What Are the Legal Fee Caps Under Florida Law?

Florida law establishes strict statutory limits on how much public adjusters can charge, with different caps applying based on whether the claim arises from a declared state of emergency. These regulations, codified inFlorida Statute 626.854, protect consumers while ensuring adjusters can operate sustainable practices.

| Claim Type | First Year Fee Cap | After First Year |

|---|---|---|

| Declared Emergency | 10% | 20% |

| Non-Disaster Claims | 20% | 20% |

| Pre-Paid Claim | 0% | 0% |

| Rapid Policy Limit Payment | 1% | 1% |

The10% cap for declared emergenciesrepresents temporary consumer protection during crisis periods when hurricanes, wildfires, or other catastrophic events impact large regions of Florida. This reduced rate applies only during the first year following the Governor’s emergency declaration, recognizing that homeowners face extraordinary financial pressures immediately after disasters.

An important nuance concerns the “rapid payment” provision. If your insurance company pays the full policy limit within14 days of the lossor10 days of contract execution, the public adjuster fee drops to just 1%. This incentivizes quick, fair settlements while protecting adjusters from working extensive hours for inadequate compensation on legitimately straightforward claims.

Additionally,Florida law prohibits public adjusters from collecting any fee if payment was issued before the contract signing date. This prevents adjusters from taking credit for settlements already negotiated or determined before their involvement, ensuring you only pay for value actually delivered.

When Do Public Adjusters Get Paid in Florida?

Understanding the timeline for how do public adjusters get paid in Florida helps clarify the risk-free nature of their services. Payment occurs only after three specific conditions are met: the insurance company issues a settlement offer, you review and accept that offer, and the insurer processes the payment.

In practical terms, this means your public adjuster might work on your claim forweeks or even months before receiving any compensation. During this time, they’re conducting property inspections, documenting damages, preparing detailed estimates, negotiating with insurance company adjusters, and potentially challenging lowball offers through the appraisal process.

The payment mechanism itself is straightforward. When your insurance company issues the settlement check, it typically deducts the agreed-upon adjuster fee and issues two separate payments: one to you for the net settlement amount, and one to the public adjuster for their earned fee. This direct payment structure eliminates any awkwardness about collecting fees and provides clear documentation for tax purposes.

For homeowners working withexperienced Florida public adjusters, this payment timeline reinforces the contingency model’s consumer-friendly nature. You’re never paying for services in advance, never gambling on uncertain outcomes, and never at financial risk beyond the opportunity cost of the adjuster’s percentage.

How Do Emergency and Non-Emergency Claims Differ?

The distinction between emergency and non-emergency claims significantly impacts how do public adjusters get paid in Florida, particularly in the aftermath of major weather events that frequently strike the state. A “declared emergency” refers specifically to situations where the Governor issues an executive order declaring a state of emergency, typically following hurricanes, tropical storms, or widespread catastrophic events.

For residents of coastal communities from Pensacola to Key West, hurricane-related claims almost always fall under the emergency designation. When Hurricane Nicole impacted the Daytona Beach area in 2022, for example, the resulting property damage claims qualified for the reduced10% fee capduring the first year following the Governor’s declaration.

Non-emergency claims encompass everyday losses like isolated fire damage, plumbing failures, roof leaks unrelated to storms, or vandalism. For a homeowner in Jacksonville experiencing a kitchen fire or a Tampa resident dealing with water damage from a burst pipe, the standard20% fee capapplies regardless of when the claim is filed.

The “one-year rule” creates an important planning consideration. If you discover hurricane damage but wait more than 12 months after the emergency declaration to hire a public adjuster, the reduced 10% rate no longer applies. The fee structure reverts to the standard 20% maximum, even though the damage originated from the declared emergency event.

This timing dynamic makes early engagement crucial for Florida homeowners.Working with a qualified public adjuster promptly after disastersnot only accelerates your recovery but also ensures you benefit from the consumer-protective fee caps established under emergency provisions.

What Contract Requirements Must Florida Public Adjusters Follow?

SinceJuly 1, 2023, Florida has enforced stringent contract requirements that govern how public adjusters formalize fee agreements with clients. These regulations, implemented to protect consumers and ensure transparency, mandate that all public adjuster engagements be documented through written contracts signed by the named insured.

The contract must clearly specify the exact percentage or fee structure the adjuster will charge, the circumstances under which that fee applies, and how payment will be calculated and collected.These written agreements cannot be modified verbally and require formal amendmentsif any terms change during the claim process.

For homeowners in Orlando, Miami, and other Florida cities, this contract requirement provides important legal protections. You have the right to review the agreement carefully, ask questions about any provisions you don’t understand, and even seek independent legal counsel before signing. Reputable public adjusters welcome this scrutiny because transparent contracts build trust and prevent disputes later.

The statute also prohibits public adjusters from collecting fees without a properly executed written contract. This means you should never work with an adjuster who promises to “work out the details later” or suggests verbal agreements are sufficient. These practices violate Florida law and could indicate an unlicensed or unethical operator.

Additional contract provisions must address cancellation rights, the scope of services the adjuster will provide, and clear disclosure of any potential conflicts of interest. For property owners navigatingcomplex insurance claim appeals or denials, these contractual protections ensure professional accountability throughout the process.

Are There Alternative Payment Arrangements Beyond Percentage Fees?

While contingency percentage fees dominate the Florida public adjuster industry,alternative payment arrangementsare emerging for specific claim types and client situations. These alternatives include hourly rates, flat fees, and hybrid models that combine elements of different compensation structures.

Hourly rate arrangements typically range from$150 to $500 per hourdepending on the adjuster’s experience, credentials, and the claim’s complexity. This model makes sense for smaller claims where a percentage fee might be disproportionately high relative to the work required. For example, a $5,000 water damage claim charged at 20% would cost $1,000, but the actual work might only require three to four hours of professional time.

Flat fee arrangements offer predictable costs for straightforward claims with clear parameters. A public adjuster might quote a fixed$2,500 to $7,500 feefor documenting and negotiating a specific type of loss, regardless of the final settlement amount. This approach appeals to commercial clients and property owners who prefer budget certainty, though it’s less common in residential markets.

Hybrid models combine a reduced percentage rate with either a minimum fee or hourly charges for specific services. These arrangements attempt to balance the incentive alignment of contingency fees with the fairness of hourly billing for administrative tasks. However, they add complexity and are rarely used except in highly specialized commercial claims.

When discussing payment options with public adjusters, ask specifically about alternatives if your situation seems unusual. A$3,000 roof leak claimmight warrant hourly billing, while a$250,000 hurricane damage claimclearly justifies the standard percentage approach. Professional adjusters will recommend the structure that best serves your interests while ensuring fair compensation for their expertise.

Key Takeaways

- Contingency-only model:Florida public adjusters work on a “no recovery, no fee” basis, charging a percentage of your final settlement only when you receive payment.

- Fee caps vary by emergency status:Declared emergency claims are capped at 10% during the first year, while non-disaster claims allow up to 20% throughout.

- Typical range of 5% to 15%:Most public adjusters in Florida charge within this range, with rates often decreasing as settlement amounts increase.

- Direct payment from insurance settlement:The adjuster’s fee is deducted from your claim payment by the insurance company, so you never write a separate check.

- Written contracts required since July 2023:All fee arrangements must be documented in signed written agreements specifying exact percentage rates and terms.

- Zero cost if claim denied:You owe nothing to your public adjuster if your claim results in no payment from the insurance company.

- Alternative arrangements available:Hourly rates ($150 to $500/hour) or flat fees may work better for very small, straightforward claims, though percentage fees remain standard for most residential property damage.

People Also Ask

Do I have to pay a public adjuster upfront in Florida?

No, public adjusters in Florida work strictly on contingency, meaning you pay nothing upfront. They only receive compensation as a percentage of your final settlement after the insurance company issues payment.

What happens if my claim is denied after hiring a public adjuster?

If your insurance claim is fully denied and results in zero payout, you owe nothing to the public adjuster. The contingency fee model means they only get paid when you receive a settlement from your insurance company.

Are public adjuster fees tax deductible in Florida?

Public adjuster fees may be tax deductible as casualty loss expenses in certain situations, but tax treatment depends on your specific circumstances. Consult with a tax professional to determine if your adjuster fees qualify for deductions under current IRS rules.

Can a public adjuster negotiate their fee percentage in Florida?

Yes, public adjusters can negotiate their fee percentage within the legal caps established by Florida law. While statute sets maximum rates (10% to 20% depending on claim type), individual adjusters may agree to lower percentages based on claim size, complexity, or competitive factors.

How is the public adjuster fee calculated on partial settlements?

The public adjuster fee is calculated as a percentage of the total amount paid by the insurance company, including any supplemental payments. If multiple payments are issued over time, the percentage applies to each payment as received, based on the terms outlined in your contract.

Do public adjusters charge extra for emergency inspections in Florida?

No, reputable public adjusters working on contingency do not charge additional fees for emergency inspections or after-hours work. All services, including initial property assessments, documentation, and negotiations, are covered under the single contingency percentage specified in your contract.

Frequently Asked Questions

What is the average public adjuster fee in Florida for hurricane claims?+

For hurricane and storm-related claims filed within the first year of a declared emergency, the legal maximum fee is 10%. Most experienced public adjusters charge within the 8% to 10% range for these claims, depending on complexity and claim size. After the first year, fees can increase up to the 20% statutory cap.

Can I negotiate the public adjuster fee before signing a contract?+

Yes, public adjuster fees are negotiable within the legal caps set by Florida statute. While many adjusters have standard rates, they may reduce their percentage for larger claims, repeat clients, or straightforward cases. Always discuss fee expectations upfront and ensure the agreed-upon percentage is clearly documented in your written contract before signing.

When does the public adjuster receive payment after settlement?+

The public adjuster receives payment immediately when the insurance company issues the settlement check. Typically, the insurer deducts the adjuster’s fee directly from the settlement amount and issues separate payments to you and your adjuster simultaneously, eliminating the need for you to handle the payment transaction.

Are there any hidden fees beyond the stated percentage?+

Reputable public adjusters working on contingency do not charge hidden fees, hourly rates, or administrative charges beyond the stated percentage in your contract. All services including inspections, documentation, estimates, and negotiations are covered under the single contingency fee. If an adjuster mentions additional charges, review the contract carefully and consider seeking a second opinion.

What if I’m not satisfied with the settlement my public adjuster negotiated?+

You are never obligated to accept a settlement offer, even if your public adjuster recommends it. If you reject a settlement offer, your adjuster typically continues negotiating at no additional cost under the contingency agreement. However, if you accept a settlement and later have regrets, you cannot recover the adjuster’s already-paid fee.

Do public adjusters in Florida charge differently for residential versus commercial claims?+

While the same statutory fee caps apply to both residential and commercial claims, commercial property claims often involve more complexity and may command fees at the higher end of the legal range. Some commercial clients negotiate hybrid fee structures combining hourly rates for specific services with reduced contingency percentages, though standard percentage fees remain most common.

Is it worth paying a public adjuster fee for small claims?+

Related:How Does a Public Adjuster Get Paid in Florida: Complete 2026 Fee Structure Guide

For claims under $10,000, the value proposition depends on the complexity and your confidence in handling the process yourself. Many public adjusters will still take smaller claims on contingency, but some may recommend hourly billing to ensure fair compensation for both parties. Always request a free consultation to discuss whether professional representation makes financial sense for your specific situation.