How to Navigate the Water Damage Insurance Claim Process in Tampa: A Complete 2026 Guide

Quick Answer

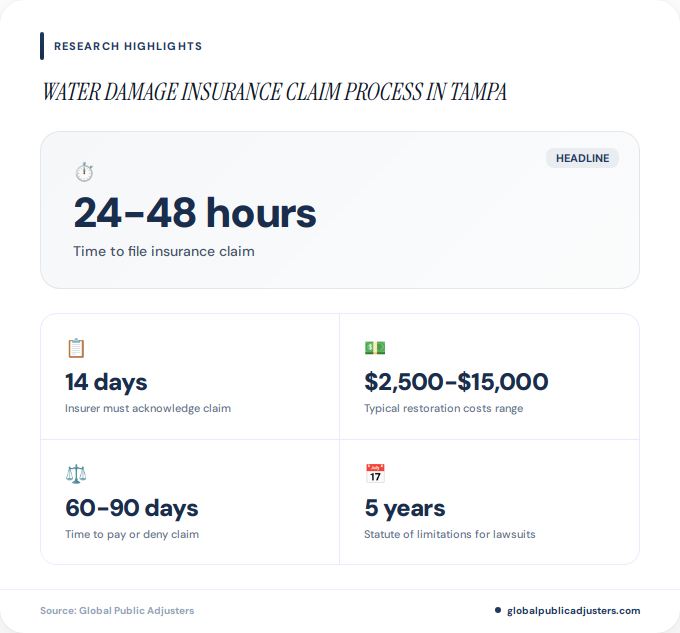

The water damage insurance claim process in Tampa requires immediate action within 24-48 hours of discovery, thorough documentation proving the damage was sudden and accidental, and strict adherence to Florida Statute 627.70131 which mandates insurers acknowledge claims within 14 days and pay or deny within 60-90 days. Tampa homeowners should expect restoration costs ranging from $2,500 to $15,000 or more depending on severity, and many complex claims benefit from professional representation given Florida’s five-year statute of limitations for breach of contract lawsuits.

When a pipe bursts in your Hyde Park bungalow at 2 AM or your Bayshore Beautiful condo floods during a summer thunderstorm, knowing the exact steps for thewater damage insurance claim process in Tampacan mean the difference between a fully reimbursed restoration and a denied claim. In 2026, Florida insurers are scrutinizing water damage claims more intensely than ever, with a sharp rise in denials based on the distinction between sudden events and gradual deterioration.

Tampa’s humid subtropical climate and frequent severe weather patterns make water damage one of the most common insurance claims in the region. Yet many homeowners make critical mistakes in the first 24 hours that permanently compromise their claim’s success. This comprehensive guide walks you through every phase of the process, backed by current Florida statutes, expert legal insights, and real cost data specific to the Tampa Bay area.

What Is the Water Damage Insurance Claim Process in Tampa?

Thewater damage insurance claim process in Tampafollows a structured sequence mandated by Florida law and individual policy terms. Unlike other states, Florida Statute 627.70131 establishes strict timelines that protect policyholders from indefinite delays while requiring homeowners to act promptly.

The process begins the moment you discover water damage. Your immediate priorities are stopping the water source if possible, preventing further damage through emergency mitigation, and contacting your insurance carrier.Tampa’s risk management guidelinesemphasize that timely notification is critical for claim approval.

Once reported, your insurer must acknowledge receipt within14 daysand initiate an investigation. An adjuster will be assigned to inspect the damage, review your policy coverage, and determine whether the loss qualifies as a covered peril. The entire claim must be paid or formally denied within60 to 90 daysdepending on specific circumstances.

| Phase | Timeline | Action Required |

|---|---|---|

| Discovery and Emergency Response | 0-24 hours | Stop water, document damage, begin mitigation |

| Insurance Notification | 24-48 hours | File claim with carrier |

| Insurer Acknowledgment | Within 14 days | Insurer confirms receipt, assigns adjuster |

| Inspection and Evaluation | 14-30 days | Adjuster visits, estimates prepared |

| Payment or Denial | Within 60-90 days | Claim resolved or formal denial issued |

Understanding these timelines empowers Tampa homeowners to identify when insurers are violating state law. If your claim sits unacknowledged past 14 days or unpaid beyond 90 days without justification, you may have grounds for a bad faith insurance lawsuit under Florida’s consumer protection statutes.

What Immediate Actions Should You Take After Water Damage?

The first hours after water damage occurs determine whether your claim succeeds or fails.Industry experts emphasize documentation as the strongest defenseagainst claim denials, and that documentation begins the instant you discover the problem.

Step 1: Stop the water source immediately.If a pipe burst, shut off the main water valve. If a roof leak, place temporary tarps. Document that you took reasonable steps to prevent additional damage, as most policies require this “duty to mitigate.”

Step 2: Document everything before touching anything.Use your smartphone to create timestamped video walkthroughs of every affected room. Capture water levels, damaged belongings, visible mold, and structural damage. Take close-up photos of serial numbers on damaged appliances and electronics.

Step 3: Begin emergency mitigation.Extract standing water, set up fans and dehumidifiers, and move salvageable items to dry areas. Tampa’s high humidity means mold can begin growing within 24-48 hours, so rapid drying is essential. Keep all receipts for equipment rental or professional services.

Step 4: Contact your insurance carrier within 24-48 hours.Most policies require “prompt notice,” and delays can provide grounds for denial. Have your policy number ready and request a claim number for all future correspondence.

In Tampa’s neighborhoods like Westchase and New Tampa where newer construction is common, homeowners should also check whether their builder’s warranty covers certain water intrusion issues. This separate coverage can supplement insurance proceeds.

What Are Florida’s Legal Timelines for Water Damage Claims?

Florida Statute 627.70131 establishes concrete deadlines that protect policyholders from indefinite claim delays, but it also imposes strict requirements on homeowners. Understanding these reciprocal obligations is essential for anyone navigating thewater damage insurance claim process in Tampa.

14-Day Acknowledgment Requirement:Upon receiving notice of your claim, your insurer must acknowledge receipt within 14 days. This acknowledgment should include the name and contact information of the assigned adjuster and an explanation of the next steps.

60-Day General Payment Deadline:For most claims, insurers must either pay the claim or issue a formal written denial within 60 days after receiving proof of loss.Legal experts note that late payments trigger statutory interest charges, which can add significant costs for insurers who delay without justification.

90-Day Extended Deadline:When claims are complex or require additional investigation, insurers have up to 90 days from receiving your sworn proof-of-loss statement. However, they must provide written explanation for why additional time is needed.

| Deadline Type | Timeline | Consequence of Violation |

|---|---|---|

| Claim Acknowledgment | 14 days from notice | Potential bad faith claim |

| Payment or Denial (standard) | 60 days from proof of loss | Interest charges begin accruing |

| Payment or Denial (complex) | 90 days from proof of loss | Statutory penalties possible |

| File New/Reopened Claim | 1 year from date of loss | Claim barred permanently |

| File Supplemental Claim | 18 months from date of loss | Additional damages not covered |

| File Breach of Contract Lawsuit | 5 years from denial or underpayment | Legal action barred |

Thefive-year statute of limitationsfor breach of contract lawsuits in Florida gives homeowners substantial time to pursue legal remedies if their claim is wrongfully denied or underpaid. However, the one-year deadline to file new claims means you cannot wait indefinitely to report damage.

If you discover additional damage after your initial claim is settled, you have 18 months from the date of loss to file a supplemental claim. This is particularly relevant in Tampa where hidden moisture damage behind walls may not appear until months after the initial event.

How Should You Document Water Damage for Insurance?

Documentation quality directly correlates with claim success rates. In 2026, Florida insurers are using advanced photo analysis and moisture detection reports to verify claims, making thorough evidence collection more important than ever for thewater damage insurance claim process in Tampa.

Visual Documentation:Create a comprehensive photo and video record showing the full extent of damage. Include wide shots establishing room context and close-ups showing specific damage. Capture ceiling stains, wall discoloration, warped flooring, damaged baseboards, and any visible mold growth. Include something for scale in photos, like a ruler or common object.

Written Inventory:List every damaged item with purchase dates and original costs if known. For electronics, note model and serial numbers. For furniture and appliances, photograph brand labels. This itemized list becomes your sworn proof of loss.

Professional Reports:Hire a licensed water damage restoration company to perform moisture readings and create a drying log. These psychrometric reports show moisture levels in building materials and track drying progress, proving you took reasonable mitigation steps. Many Tampa restoration companies serving areas like Temple Terrace and Carrollwood provide these reports as part of their emergency response.

Communication Records:Keep copies of every email, text message, and letter exchanged with your insurer. Note the date, time, and content of phone conversations. If your adjuster makes verbal commitments about coverage, follow up with an email confirming “per our conversation today, you indicated that…”

Contractor Estimates:Obtain at least two independent estimates from licensed Tampa contractors for repair costs. These third-party assessments provide a reality check against your insurer’s estimate and can reveal undervaluation.

Why Does “Sudden and Accidental” Matter for Tampa Claims?

The most common reason for water damage claim denials in Florida is the insurer’s determination that damage was “gradual” rather than “sudden and accidental.”Standard homeowners policies explicitly exclude damage resulting from wear and tear, and insurers aggressively apply this exclusion.

Covered: Sudden and Accidental

- Pipe bursts from frozen temperatures or sudden pressure failure

- Washing machine hose rupture flooding your laundry room

- Roof damage from a specific storm allowing water intrusion

- Toilet overflow from a mechanical failure

- Water heater tank catastrophic failure

Not Covered: Gradual and Predictable

- Slow leaks from deteriorating pipe joints over months

- Seepage through cracks in foundation that developed gradually

- Condensation damage from chronically poor ventilation

- Roof leak from worn shingles that should have been replaced

- Groundwater seepage from inadequate drainage

The distinction becomes murky in real-world scenarios. What if a pipe gradually weakened over time but the actual rupture happened suddenly? Florida courts generally favor policyholders when the precipitating event was sudden, even if underlying conditions contributed.

In Tampa’s older neighborhoods like Seminole Heights where many homes date from the 1920s-1940s, this distinction is particularly contentious. Insurers may argue that water damage in historic homes results from deferred maintenance rather than covered perils. Building a strong case requires proving the specific triggering event was sudden, regardless of building age.

What Are Typical Water Damage Restoration Costs in Tampa?

Water damage restoration costs in Tampa vary dramatically based on the extent of damage, affected materials, presence of contamination, and required structural repairs.Recent Tampa Bay area data shows restoration costs typically range from $2,500 to $15,000 or significantly higherfor extensive damage involving multiple rooms or structural compromise.

Several factors influence where your claim falls within this range:

Water Category:Clean water from supply lines costs less to remediate than gray water from appliances or black water from sewage or flooding. Category 3 black water requires extensive disinfection and often material removal.

Affected Materials:Drywall and carpet can often be dried if addressed within 48 hours, while hardwood flooring may require replacement. Tile generally survives, but the subfloor beneath may need replacement.

Square Footage:A single bathroom flood might cost $2,500 to $6,000 to restore, while whole-home flooding can reach $30,000 to $75,000 or more depending on the home’s size and finishes.

Mold Remediation:If mold growth occurs before mitigation begins, add $1,500 to $10,000 or more for professional remediation. Tampa’s humidity accelerates mold growth, making rapid response critical.

Structural Repairs:Damage to framing, electrical systems, or HVAC ductwork substantially increases costs. Foundation issues or compromised load-bearing walls require engineering assessments and specialized repairs.

For homeowners in premium Tampa neighborhoods like Davis Islands or South Tampa with high-end finishes, restoration costs trend toward the upper ranges. Custom tile work, hardwood flooring, and designer fixtures cannot simply be replaced with builder-grade materials, andprofessional public adjustersensure your settlement reflects actual replacement costs.

Keep in mind that pricing varies based on your specific project scope, material selections, and quality expectations. Always obtain multiple detailed estimates from licensed Tampa contractors and avoid choosing solely based on the lowest bid, as this often leads to substandard work that may not fully resolve moisture issues.

Why Do Water Damage Claims Get Denied in Florida?

Understanding common denial reasons helps Tampa homeowners avoid pitfalls in thewater damage insurance claim process. In 2026, Florida insurers are denying claims at higher rates than in previous years, citing more stringent interpretations of policy language.

1. Delayed Reporting:Many policies require “immediate” or “prompt” notice. Waiting weeks to report damage gives insurers grounds to argue you violated policy conditions. Even if Florida law allows claim filing up to one year after loss, your specific policy may require faster notification.

2. Maintenance-Related Damage:If your adjuster finds evidence of poor maintenance like rusted pipes, worn roof shingles, or deteriorated caulking, they may deny the claim as gradual damage. Regular home maintenance documentation helps counter these arguments.

3. Excluded Perils:Standard policies exclude flooding from external water sources, sewer backup (unless you purchased that endorsement), and groundwater seepage. Understanding exactly what your Tampa-area policy covers prevents filing non-covered claims.

4. Inadequate Mitigation:If you failed to take reasonable steps to prevent additional damage after discovering the problem, insurers may deny subsequent damage. This is why documenting your immediate response is critical.

5. Vacancy or Unoccupancy:If your home was unoccupied for 30-60 consecutive days (specific periods vary by policy), many carriers invoke vacancy clauses to deny or limit coverage. Tampa’s seasonal resident population should be particularly aware of this exclusion.

6. Pre-Existing Damage:If adjusters determine damage existed before your policy effective date or before the claimed event, they will deny coverage for that damage. This is why pre-insurance home inspections and photos are valuable.

If your claim is denied, you have appeal rights. Request the denial in writing with specific policy language cited. Many denials are overturned on appeal, especially whenyou hire a public adjuster in Floridawho understands policy interpretation and appeals procedures.

When Should You Hire a Public Adjuster in Tampa?

Public adjusters work exclusively for policyholders, not insurance companies, and their expertise can dramatically increase settlement amounts. For Tampa homeowners navigating complex claims, professional representation often proves invaluable.

Ideal Scenarios for Public Adjuster Involvement:

Consider hiring a public adjuster when your claim involves extensive damage exceeding $10,000, multiple affected areas, or structural repairs.Water damage adjusters in Floridabring specialized knowledge of moisture detection, proper remediation protocols, and accurate cost estimating.

Public adjusters prove especially valuable when insurers dispute the cause of damage, claim it was gradual rather than sudden, or offer settlements that seem inadequate for full restoration. They understand policy language nuances and know how to document claims to maximize coverage.

In Tampa’s competitive insurance market, carriers increasingly lowball initial offers, expecting homeowners to accept without question. Public adjusters negotiate from detailed estimates and comprehensive damage assessments, often securing settlements 2-3 times higher than initial offers.

Public adjusters also handle the administrative burden of the claims process, coordinating inspections, obtaining contractor estimates, preparing sworn proof-of-loss statements, and managing all insurer communications. For busy Tampa professionals or elderly homeowners, this service alone justifies the fee.

Understanding Public Adjuster Fees:

Florida law caps public adjuster fees at 20% for non-emergency claims and 10% for declared emergencies. Some adjusters charge flat fees for smaller claims.Public adjuster fees in Floridaare typically paid only if your claim succeeds, making this a low-risk investment for homeowners.

The key question is not whether the adjuster’s fee is worth it, but rather whether you could achieve the same settlement on your own. For complex Tampa water damage claims, the answer is typically no. Professional representation increases both the likelihood of approval and the settlement amount.

People Also Ask

How soon must I report water damage to my insurer in Tampa?

Report water damage to your insurance carrier within 24-48 hours of discovery for optimal claim success. While Florida law allows claim filing up to one year after loss, most policies require “prompt notice,” and delays can provide grounds for denial or reduced settlements.

Does homeowners insurance cover all types of water damage?

No. Standard homeowners policies cover sudden and accidental water damage from internal sources like burst pipes but exclude flooding from external sources, gradual damage from maintenance issues, and often sewer backup unless you purchase additional endorsements.

What happens if my Tampa water damage claim is denied?

Request a written denial with specific policy citations, then file an appeal with additional documentation supporting your claim. Many Tampa homeowners successfully overturn denials with help from public adjusters or attorneys who understand Florida insurance law and policy interpretation.

How long does the water damage claims process take in Florida?

Under Florida Statute 627.70131, insurers must acknowledge claims within 14 days and pay or deny within 60-90 days depending on complexity. Simple claims may resolve in 30-45 days, while disputed or complex claims can extend several months.

Should I start repairs before the insurance adjuster inspects?

Perform emergency mitigation immediately to prevent additional damage, but document everything before starting. Most policies require you to mitigate further loss, but delay permanent repairs until after the adjuster inspects unless emergency circumstances require immediate action.

Can I choose my own contractor for water damage restoration in Tampa?

Yes. You have the right to select your own contractor for repairs regardless of any preferred vendor list your insurer provides. However, your settlement is based on reasonable and necessary costs, so obtain multiple estimates to demonstrate market rates.

Frequently Asked Questions

What documentation do I need to file a water damage claim in Tampa?+

You need timestamped photos and videos of all damage, a written inventory of damaged items with values, contractor estimates for repairs, receipts for emergency mitigation expenses, and professional moisture readings if available. Keep all communication records with your insurer and maintain a detailed timeline of events from discovery through claim resolution.

Does flood insurance cover water damage in Tampa homes?+

Flood insurance covers water damage from external sources like storm surge, heavy rain, or river overflow, which standard homeowners policies exclude. If water enters through your roof during a storm and then pools on floors, this may be covered by homeowners insurance. However, rising water from outside requires separate flood insurance available through the National Flood Insurance Program or private carriers.

How much does water damage restoration cost in Tampa?+

Water damage restoration in Tampa typically ranges from $2,500 to $15,000 or substantially more depending on severity, affected square footage, water category, and required repairs. Minor bathroom floods may cost $2,500-$6,000, while whole-home restoration can exceed $30,000-$75,000. Mold remediation adds $1,500-$10,000 or more if growth is extensive. Pricing depends heavily on your specific circumstances, materials, and quality expectations.

Will filing a water damage claim increase my Tampa homeowners insurance rates?+

Filing a claim can potentially increase your rates or affect renewal, particularly if you file multiple claims within a short period. However, Florida’s competitive insurance market and state regulations limit arbitrary rate increases. Many Tampa homeowners find that properly documented legitimate claims have minimal long-term rate impact, especially for first-time claims.

What is the difference between a public adjuster and an insurance adjuster?+

Insurance adjusters work for the insurance company and represent the carrier’s interests in minimizing payouts. Public adjusters work exclusively for policyholders and are licensed professionals who maximize your settlement. Public adjusters charge a percentage of the settlement (typically 10-20% in Florida) but often secure substantially higher payouts than homeowners could achieve independently.

Can I reopen a water damage claim if I discover additional damage later?+

Yes, Florida law allows supplemental claims for additional damage discovered after your initial claim closes, provided you file within 18 months of the original date of loss. This is particularly important for hidden moisture damage behind walls or under flooring that may not appear immediately. Document new damage thoroughly and notify your carrier promptly.

What should I do if my Tampa insurer delays my water damage claim beyond legal deadlines?+

If your insurer violates Florida’s statutory deadlines (14 days for acknowledgment, 60-90 days for payment or denial), document the delays and send written notice demanding compliance. If delays continue, consult a Florida insurance attorney about potential bad faith claims. You may be entitled to statutory interest, penalties, and attorney fees if the insurer acted in bad faith.

Key Takeaways

- Act immediatelywhen water damage occurs in your Tampa home by stopping the source, documenting everything before cleanup, and notifying your insurer within 24-48 hours to comply with policy requirements.

- Understand Florida’s legal timelinesunder Statute 627.70131, which requires insurers to acknowledge claims within 14 days and pay or deny within 60-90 days, with interest charges for late payments.

- Distinguish sudden vs. gradual damagein your claim documentation, as standard policies cover sudden and accidental events but exclude gradual deterioration from deferred maintenance.

- Document comprehensivelywith timestamped photos, videos, written inventories, professional moisture readings, contractor estimates, and records of all mitigation efforts and insurer communications.

- Budget appropriatelyfor restoration costs ranging from $2,500 to $15,000 or significantly more depending on damage extent, water category, and structural repairs required.

- Consider professional representationfrompublic adjustersfor complex claims, denials, or disputes, as they typically secure substantially higher settlements.

- Know your appeal rightsif claims are denied, and understand the five-year statute of limitations for breach of contract lawsuits if insurers act in bad faith.

Taking Control of Your Water Damage Claim

Navigating thewater damage insurance claim process in Tamparequires knowledge, documentation, and persistence. From the moment water begins pooling in your Palma Ceia home to the final settlement check, every action you take influences your claim’s outcome.

Tampa homeowners face unique challenges from the region’s humidity, aging infrastructure in historic neighborhoods, and an insurance market increasingly scrutinizing water damage claims. By understanding Florida’s legal framework, documenting damage comprehensively, and knowing when to seek professional help, you protect your largest investment and ensure full recovery from unexpected water events.

If you’re currently dealing with water damage or facing a denied or underpaid claim, don’t navigate this complex process alone.Contact our experienced teamtoday for a free claim evaluation. We’ve helped hundreds of Tampa-area homeowners maximize their settlements and hold insurers accountable to their policy obligations.

Related:Public Adjuster Colorado in Florida: Complete 2026 Cross-State Licensing and Practice Guide

Remember, you have rights under Florida law, and insurers must honor their contractual commitments. With proper preparation and expert guidance, you can successfully navigate the claims process and restore your home to its pre-loss condition.