How to Successfully Appeal a Water Damage Claim Denial in Florida: 2026 Complete Guide

Quick Answer

Appealing a water damage claim denial in Florida requires submitting independent inspection reports, moisture meter readings, and maintenance records within30 daysof the denial notice to prove the damage was sudden rather than gradual. Success depends on providing evidence-based documentation that counters insurer claims of negligence or long-term deterioration, with the option to file a bad faith lawsuit underFla. Stat. §624.155if the insurer unreasonably denies your claim.

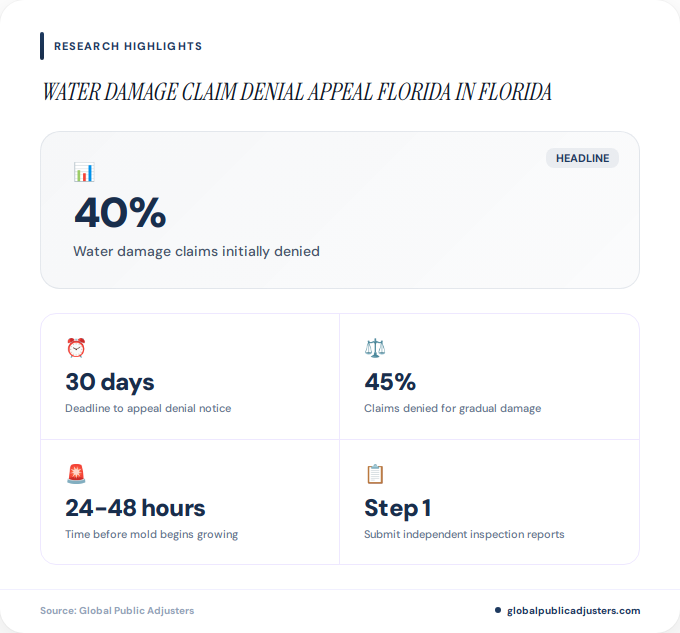

Did you know thatnearly 40% of water damage claims in Florida are initially deniedby insurance companies? If you’re among the thousands of homeowners in Tampa, Miami, Jacksonville, or Orlando facing a denial letter, you’re not alone. The good news: with the right approach, many denials can be successfully overturned.

In Florida’s humid climate, where a single afternoon thunderstorm can cause thousands of dollars in interior damage, understanding how to appeal a water damage claim denial is critical. Insurance companies often cite vague reasons like “gradual deterioration” or “lack of maintenance” to avoid paying legitimate claims, leaving homeowners scrambling to prove their case.

This comprehensive guide walks you through every step of thewater damage claim denial appeal process in Florida, from understanding why claims get denied to building an evidence-based appeal that stands up to scrutiny. Whether you’re dealing with burst pipes, storm damage, or appliance failures, this article provides the actionable strategies you need to fight back.

Why Are Water Damage Claims Denied in Florida?

Insurance companies in Florida deny water damage claims for several strategic reasons, often focusing on technical policy language and timing issues. Understanding these common denial reasons is your first step toward building a successful appeal.

The most frequent denial reason is thegradual damage exclusion. Insurers argue that the water damage occurred slowly over time due to poor maintenance rather than from a sudden, covered event. This distinction is crucial because standard homeowners policies in Florida cover sudden water damage (like burst pipes) but exclude damage from long-term leaks or deterioration.

Other common reasons include claims that you failed to maintain your property, missed filing deadlines, or that the damage falls under a policy exclusion. According toexperienced property damage attorneys, many denials also cite failure to mitigate further damage after the initial incident.

| Denial Reason | Percentage of Cases | Appeal Success Rate |

|---|---|---|

| Gradual Damage | 45% | 35-50% |

| Lack of Maintenance | 30% | 40-55% |

| Policy Exclusions | 15% | 20-30% |

| Missed Deadlines | 10% | 60-75% |

In Florida’s high-humidity environment, wheremold can begin growing within 24 to 48 hoursof water exposure, timing becomes critical. What starts as a covered sudden water event can quickly transform into a coverage dispute if you don’t act immediately to document damage and begin mitigation.

What Is the Difference Between Sudden and Gradual Damage?

The distinction between sudden and gradual water damage is the single most important factor in Florida water damage claim appeals. This technical difference determines whether your policy covers the loss or excludes it entirely.

Sudden damagerefers to water intrusion that occurs unexpectedly and over a short period. Examples include a pipe that bursts during a freeze, a washing machine hose that ruptures, or roof damage from a hurricane that allows rain to enter your home. These events are typically covered under standard Florida homeowners insurance policies.

Gradual damageinvolves water intrusion that happens slowly over weeks, months, or years. This includes slow leaks behind walls, ongoing roof deterioration, or condensation buildup from poor ventilation. Insurance companies exclude this type of damage because it’s considered preventable through regular maintenance and inspection.

The challenge arises when insurers try to recharacterize sudden events as gradual damage. They may point to pre-existing conditions, minor water stains, or normal wear and tear to argue that your damage didn’t happen suddenly. According toFlorida insurance claim attorneys, this is where independent inspections become essential to proving your case.

Florida courts have consistently ruled that the burden of proof lies with the insurance company to demonstrate that damage was gradual rather than sudden. However, you must still provide evidence that supports a sudden occurrence, includingproper documentation from the moment you discover the damage.

What Are the Critical Deadlines for Appealing in Florida?

Florida law imposes strict deadlines throughout the water damage claim process, and missing any of these can permanently forfeit your rights. Understanding these timelines is essential for a successful appeal.

Initial Notice Period:You must notify your insurance company “as soon as practical” after discovering water damage. While Florida law doesn’t specify an exact timeframe, most policies require notice within a reasonable period, typically interpreted asa few days to one week.

Insurer Response Deadline:Once notified, Florida insurers must acknowledge your claim within14 daysand either pay or deny the claim within60 daysof receiving all requested documentation. Failure to meet these deadlines can trigger statutory penalties and bad faith claims.

Appeal Window:After receiving a denial letter, you typically have30 daysto file a formal dispute with your insurer or the Florida Department of Financial Services. Some policies may provide longer periods, so review your specific policy language carefully.

Supplemental Claims:Florida law allows you to reopen or supplement a property claim only if you provide notice within1 yearof the loss. For hidden damage discovered later (like mold behind walls), you have up to18 monthsto file a supplemental claim.

Lawsuit Filing Deadline:The statute of limitations for filing a lawsuit against your insurer is2 yearsfrom the date of loss, not from the date of denial. This means if your water damage occurred on January 1, 2025, you have until January 1, 2027 to file suit, regardless of when the claim was denied. Understandinghow long the entire claims process takescan help you plan accordingly.

What Evidence Do You Need to Win Your Appeal?

Winning a water damage claim denial appeal in Florida requires comprehensive, professional documentation that directly contradicts the insurer’s denial reasoning. The stronger and more objective your evidence, the higher your chances of success.

Independent Inspection Reports:Hire a licensed contractor, plumber, or public adjuster to conduct a thorough inspection and provide a written report. This report should specifically address the cause of damage, whether it was sudden or gradual, and the scope of necessary repairs. Independent reports carry significantly more weight than homeowner observations.

Moisture Meter Readings:Professional moisture detection equipment can prove when water intrusion occurred. High moisture readings in isolated areas support a sudden event claim, while widespread readings at similar levels might suggest gradual seepage. Document these readings with timestamped reports.

Maintenance Records:Compile all documentation showing regular home maintenance, including plumbing inspections, HVAC servicing, roof repairs, and preventive work. This evidence directly counters “lack of maintenance” denials. Receipts, invoices, and service reports from licensed professionals are essential.

Photographic and Video Evidence:Take extensive photos and videos immediately after discovering damage, during mitigation, and throughout the repair process. Include wide shots showing context and close-ups of specific damage. Date-stamp all media if possible.

According toFlorida real estate attorneys specializing in mold claims, documentation must create a clear timeline that proves the damage’s sudden nature. This becomes particularly important in Tampa, Miami, and other coastal Florida cities where high humidity can accelerate secondary damage.

Witness Statements:If neighbors, guests, or contractors witnessed the water event or its immediate aftermath, obtain written statements. These third-party accounts can corroborate your version of events.

Expert Reports:For complex cases, consider hiring forensic engineers or water damage specialists who can provide expert testimony about causation, timing, and industry standards. While these reports can cost anywhere from$1,500 to $5,000+, they often prove decisive in appeals.

How Do You File a Water Damage Claim Denial Appeal in Florida?

Filing a successful water damage claim denial appeal in Florida involves a systematic, well-documented process that demonstrates the insurer’s error while providing compelling evidence for coverage.

Step 1: Review the Denial Letter Thoroughly.Your denial letter must explain the specific policy provisions or exclusions the insurer relies on. Look for vague language, incorrect facts, or misapplied policy terms. Document every assertion the insurer makes, as you’ll need to address each point in your appeal.

Step 2: Review Your Policy.Read your entire insurance policy, paying special attention to covered perils, exclusions, definitions, and claims procedures. Compare the policy language to the denial reasoning. Many homeowners discover that insurers misinterpret or misapply their own policy terms.

Step 3: Gather Your Evidence.Compile all documentation described in the previous section: inspection reports, maintenance records, photos, moisture readings, and expert assessments. Organize everything chronologically with a detailed index.

Step 4: Draft Your Appeal Letter.Write a formal appeal letter that:

- References your policy number and claim number

- Clearly states you are appealing the denial

- Systematically addresses each denial reason with specific evidence

- Cites relevant policy language supporting coverage

- Includes a timeline of events demonstrating sudden damage

- Attaches all supporting documentation

- Requests specific action (claim approval and payment)

- Sets a reasonable deadline for response (typically 30 days)

Step 5: Submit Through Proper Channels.Send your appeal via certified mail with return receipt requested to create a paper trail. Also send a copy to the Florida Department of Financial Services Division of Consumer Services. Keep copies of everything.

Step 6: Follow Up.If you don’t receive acknowledgment within 14 days, follow up in writing. Florida law requires insurers to acknowledge communications promptly. Consider working witha public adjuster who specializes in appealsto navigate this process professionally.

Step 7: Consider Appraisal or Mediation.Many Florida policies include appraisal clauses that allow disputes over theamountof loss to be resolved through a panel of appraisers. While this process doesn’t typically override coverage denials, it can establish the true cost of repairs, making litigation more attractive to pursue if necessary.

When Should You Consider a Bad Faith Lawsuit?

If your appeal is denied or ignored, a bad faith insurance lawsuit may be your most powerful option. UnderFlorida Statute §624.155, insurers can face significant penalties for unreasonably denying or delaying claims.

Bad faith occurs when an insurer fails to act in good faith toward its policyholders. In Florida, this includes denying a claim without a reasonable basis, failing to conduct a proper investigation, or refusing to pay a claim when liability is clear.Insurance defense attorneys notethat bad faith claims have become increasingly common in 2026 as insurers tighten claim approval standards.

You should consider a bad faith lawsuit when:

- The insurer denied your claim despite clear evidence of coverage

- The company failed to conduct a reasonable investigation

- The insurer missed statutory deadlines without justification

- The denial reasoning contradicts the policy language

- The company refused to communicate or respond to your appeal

- Your independent experts directly contradict the insurer’s findings

Bad faith lawsuits can recover not only the original claim amount but also consequential damages, attorney fees, and in some cases punitive damages. This makes pursuing bad faith financially viable even for moderate-sized claims. However, you must first exhaust internal appeals and provide the insurer notice of your bad faith claim before filing suit.

The timeline for bad faith claims differs from standard claim denials. You should consult with a Florida insurance attorney within the2-year statute of limitationsfor property claims to explore all options. Many attorneys offer free consultations to evaluate whether your case merits bad faith pursuit.

Working withexperienced public adjusters in Floridacan strengthen your position before you reach the lawsuit stage, as they document every interaction and build a comprehensive claim file that demonstrates the insurer’s unreasonable conduct.

How Does Mold Impact Your Water Damage Claim?

Mold presents one of the most contentious issues in Florida water damage claims. The state’s humid climate creates ideal conditions for rapid mold growth, turning a straightforward water damage claim into a complex coverage dispute.

Most Florida homeowners policies providelimited mold coverage, typically capped at$10,000 to $25,000. However, this coverage only applies when mold results from a covered peril and the homeowner took reasonable steps to mitigate the damage. If mold grows due to your failure to dry out the property promptly, the insurer may deny coverage entirely.

In Florida’s climate, mold can begin growing within24 to 48 hoursof water exposure. This creates an urgent timeline: you must immediately begin mitigation (water extraction, dehumidification, air circulation) while simultaneously documenting the damage for your claim. Delays in mitigation often provide insurers with grounds to deny mold-related damage.

The key distinction insurers examine is whether mold resulted from:

- A covered sudden water event with prompt mitigation:Usually covered up to policy limits

- A covered event with delayed mitigation:May be partially covered or denied based on failure to mitigate

- Gradual moisture intrusion:Typically excluded entirely

- High humidity without a specific water event:Excluded as maintenance issue

If your water damage claim includes mold, document the exact timeline of events: when you discovered the water, when you began mitigation efforts, when you notified the insurer, and when mold was discovered. Professional mold inspections with air quality testing can prove the extent and cause of mold growth.

For Orlando, Jacksonville, and Tampa homeowners, where summer humidity regularly exceeds75%, even minor water intrusion can quickly escalate. Consider professional water extraction and drying services within hours of discovering water damage to protect both your property and your insurance claim.

What Does an Appeal Cost and How Long Does It Take?

Understanding the costs and timeline for appealing a water damage claim denial in Florida helps you plan your approach and decide whether to handle the appeal yourself or hire professionals.

Cost Considerations:

DIY appeals cost relatively little, typically$200 to $800for documentation, certified mailing, and perhaps one professional inspection report. However, DIY appeals have lower success rates when dealing with complex denials or significant claim amounts.

Hiring a public adjuster typically costs10% to 20%of the final settlement amount, with fees only charged if the claim is successfully resolved. For a$50,000claim, this means$5,000 to $10,000in fees, but public adjusters often recover substantially more than homeowners can achieve independently. Learn more aboutstandard public adjuster fees in Floridato understand the investment.

Attorney representation for appeals or litigation operates on contingency fees (typically33% to 40%of recovery) or hourly rates ranging from$250 to $500+ per hourdepending on the attorney’s experience and location. Miami and Tampa attorneys generally charge higher rates than those in smaller Florida cities.

Timeline Expectations:

The appeal process timeline varies significantly based on your approach and the insurer’s responsiveness:

| Appeal Method | Typical Timeline | Success Rate |

|---|---|---|

| DIY Internal Appeal | 30-60 days | 25-35% |

| Public Adjuster Appeal | 45-90 days | 45-65% |

| Appraisal Process | 60-120 days | 60-75% |

| Attorney Negotiation | 90-180 days | 65-80% |

| Litigation to Settlement | 12-24 months | 75-85% |

Keep in mind that Florida’s legal system experiences significant case backlogs, particularly in South Florida counties. If your case proceeds to litigation, expect longer timelines than the averages shown above. However, the threat of litigation often motivates insurers to settle during the appeal or mediation phase.

Many homeowners find that working with professionals early in the process actually saves time and money by avoiding multiple rounds of denied appeals. Understandinghow public adjusters structure their feescan help you make an informed decision about representation.

People Also Ask

Can I appeal if the insurer says it was gradual damage?

Yes, you can and should appeal gradual damage denials with evidence proving the damage was sudden. This includes independent inspection reports showing a specific failure point, moisture meter readings indicating recent water intrusion, and maintenance records demonstrating regular upkeep that should have detected gradual issues.

What happens if I miss the 30-day appeal deadline in Florida?

Missing the internal appeal deadline doesn’t automatically forfeit your rights, but it complicates the process. You still have up to 2 years from the date of loss to file a lawsuit challenging the denial. However, insurers may argue you waived your appeal rights, so it’s critical to act quickly and document any reasons for delay.

Do I need a lawyer or can a public adjuster handle my appeal?

Public adjusters excel at documentation, damage assessment, and negotiating with insurers during the initial appeal phase. Attorneys become necessary when the insurer continues to deny the claim after appeal, when bad faith is suspected, or when litigation becomes inevitable. Many homeowners start with a public adjuster and add an attorney if needed.

Can my insurance company drop me after I appeal a claim denial?

In Florida, insurers can non-renew your policy after a claim (even an appealed one), but they cannot cancel mid-term except for non-payment or fraud. Non-renewal requires 120 days’ notice for property policies. This risk shouldn’t prevent you from appealing a legitimate claim, as you can find alternative coverage.

What is the success rate for water damage claim appeals in Florida?

Overall success rates vary between 35% and 80% depending on the appeal method, quality of evidence, and reason for initial denial. Appeals with professional representation and comprehensive documentation succeed at significantly higher rates than DIY appeals, particularly for claims over $20,000.

How does Florida’s climate affect water damage claim appeals?

Florida’s high humidity and frequent storms create unique challenges in distinguishing sudden damage from gradual deterioration. Insurers often argue that water damage in Florida is maintenance-related due to the harsh climate, making professional inspections and regular maintenance documentation even more critical for successful appeals in Tampa, Miami, Orlando, and other humid Florida cities.

Key Takeaways: Winning Your Water Damage Claim Denial Appeal in Florida

- Act immediately:Florida’s30-dayappeal window and2-yearlawsuit deadline are strict. Begin gathering evidence and filing your appeal as soon as you receive the denial letter.

- Focus on sudden vs. gradual:The majority of denials hinge on this distinction. Professional inspection reports, moisture readings, and maintenance records are essential to proving sudden damage.

- Document everything:From the moment you discover water damage through the entire appeal process, maintain comprehensive photographic, written, and expert documentation.

- Challenge vague denials:If the insurer’s denial letter uses vague language or fails to cite specific policy provisions, point this out in your appeal with supporting evidence.

- Consider professional help early:Public adjusters and attorneys have significantly higher success rates than DIY appeals, particularly for claims over$20,000. Their fees are often contingent on success.

- Don’t ignore mold:In Florida’s climate, address water damage within24 to 48 hoursto prevent mold growth that can complicate or void your claim.

- Bad faith is a powerful tool:If the insurer acts unreasonably, denies without investigation, or misses statutory deadlines, a bad faith claim can recover far more than the original claim amount plus attorney fees.

Conclusion: Take Control of Your Water Damage Claim Appeal

Appealing a denied water damage claim in Florida requires strategy, evidence, and often professional assistance, but it’s absolutely worth pursuing. With40% of initial water damage claimsbeing denied and appeal success rates ranging from35% to 80%depending on your approach, the odds improve dramatically when you understand the process and leverage the right resources.

Whether you’re dealing with a burst pipe in Tampa, hurricane damage in Miami, or appliance failure in Jacksonville, the principles remain consistent: prove the damage was sudden, demonstrate proper maintenance, document everything, and meet all deadlines. Florida’s consumer protection laws and bad faith statutes provide powerful leverage when insurers act unreasonably.

Don’t let a denial letter be the final word on your claim. If you’re facing a water damage claim denial appeal in Florida,contact our experienced team of public adjustersfor a free consultation. We’ve successfully appealed hundreds of denials across Florida, recovering millions of dollars for homeowners who were initially told “no” by their insurance companies.

Your home is your largest investment. Fight for the coverage you’ve paid for with a strategic, evidence-based appeal that holds your insurer accountable. The sooner you act, the stronger your position becomes.

Frequently Asked Questions

How long does the Florida water damage claim appeal process typically take?+

The appeal timeline varies from 30 days for simple internal appeals to 12-24 months if litigation becomes necessary. Most professionally managed appeals resolve within 45-180 days through negotiation or mediation, avoiding the need for lengthy court proceedings.

Can I file a bad faith lawsuit immediately after my claim is denied?+

No, Florida law requires you to exhaust internal appeals and provide the insurer with formal notice of your bad faith claim before filing suit. This notice gives the insurer one final opportunity to resolve the claim before facing potential penalties, attorney fees, and punitive damages in court.

What is the most common mistake homeowners make when appealing water damage claim denials?+

The most common mistake is relying solely on personal observations and photos without obtaining independent professional inspections and expert reports. Insurers heavily discount homeowner evidence, so third-party documentation from licensed contractors, engineers, or public adjusters is essential for credibility.

Does hiring a public adjuster guarantee my appeal will succeed?+

No professional can guarantee success, but public adjusters significantly improve your odds through expert documentation, policy analysis, and negotiation skills. Success rates increase from 25-35% for DIY appeals to 45-65% with public adjuster representation, making them a valuable investment for substantial claims.

Will my insurance premiums increase if I successfully appeal a claim denial?+

Premium increases depend on your insurer’s underwriting guidelines and Florida’s regulatory environment, not on whether you appealed. Any claim payment, whether after initial approval or successful appeal, may impact future premiums. However, this shouldn’t deter you from pursuing legitimate claims you’ve paid to have covered.

Can I appeal a water damage claim denial if I’ve already started repairs?+

Yes, you can still appeal even after beginning repairs, though it’s more challenging. Document all work extensively with before photos, contractor reports, and receipts. Florida law actually requires you to mitigate further damage, so necessary emergency repairs shouldn’t prevent an appeal if properly documented.

What percentage of water damage appeals succeed in Florida courts?+

Cases that reach litigation (after failed internal appeals) have a 75-85% success rate for plaintiffs, though many settle before trial. This high success rate reflects that only the strongest cases with clear evidence of coverage or bad faith proceed to court, while weaker cases settle or are abandoned earlier in the process.