Public Adjuster Colorado in Florida: Complete 2026 Cross-State Licensing and Practice Guide

Quick Answer

There is no single profession called “public adjuster Colorado in Florida,” but rather public adjusters who hold dual licenses in both Colorado and Florida to operate across state lines. Only Florida-licensed public adjusters can legally represent policyholders on insurance claims within Florida, though many firms now maintain licenses in both states to serve clients nationwide with local expertise.

The insurance claims landscape has evolved dramatically in 2026, with property owners across the United States seeking expert representation from licensed public adjusters. An intriguing trend has emerged: the growing demand for public adjusters who hold licenses in multiple states, particularlyColorado and Florida. As hurricane season intensifies along Florida’s Gulf Coast and severe weather events impact Colorado’s Front Range, understanding cross-state licensing and how adjusters operate in different jurisdictions has become critical for both policyholders and industry professionals.

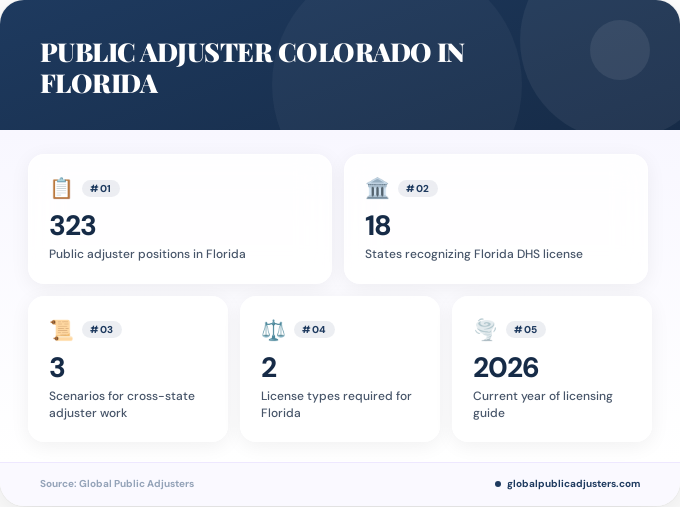

According to 2026 data,323 public adjuster positionsare currently available in Florida alone, with many requiring specialized state licensing. Meanwhile, adjusters working across state lines are commanding premium compensation packages, reflecting the specialized knowledge required to navigate different regulatory environments and serve clients in Tampa, Miami, Denver, and Colorado Springs effectively.

What Does “Public Adjuster Colorado in Florida” Really Mean?

The phrase “public adjuster Colorado in Florida” often causes confusion among property owners seeking claims assistance. This terminology typically refers to one of three scenarios: a Colorado-based public adjuster seeking to work on claims in Florida, a Florida adjuster with Colorado licensing, or a dual-licensed professional who operates in both states.

In Florida, the law is crystal clear.Only Florida-licensed public adjusters can legally represent policyholderson insurance claims within state boundaries. The Florida Department of Financial Services strictly enforces this requirement, with unlicensed adjusters facing significant penalties and potential fraud charges.Florida consumer protection guidelinesemphasize that anyone representing a policyholder in negotiations with an insurance company must hold the appropriate state license.

However, the insurance industry has adapted to meet growing demand. Many prominent firms now maintaindual licenses in both Colorado and Florida, enabling them to serve clients throughout both states with full legal authority. These firms understand the unique challenges of Florida’s hurricane-prone climate, from Tampa’s storm surge risks to Miami’s flooding concerns, while also navigating Colorado’s hail damage and wildfire claim complexities.

How Do Licensing Requirements Differ Between Colorado and Florida?

Colorado and Florida maintain distinctly different regulatory frameworks for public adjusters, reflecting each state’s unique insurance market and consumer protection priorities. Understanding these differences is essential for adjusters seeking to practice in both jurisdictions.

Florida’s licensing structureis comprehensive and rigorous. The state requires public adjusters to obtain either aFlorida 3-20 (resident) or 7-20 (non-resident) All-Lines Adjuster Licenseto represent policyholders. Additionally, Florida offers the prestigiousFlorida 70-20 Designated Home State (DHS) Adjuster License, which is recognized in18 statesincluding Colorado, Illinois, Kansas, and Virginia. This reciprocal recognition makes the Florida license highly valuable for adjusters planning multi-state practices.

Colorado’s approach differs significantly. The state does not require specific licensing for company or independent adjusters in many categories, though public adjusters representing policyholders must meet certain requirements. This less restrictive environment has led many adjusters to pursue the Florida DHS license as their primary credential, which then provides authority to work in Colorado.

| Licensing Aspect | Florida | Colorado |

|---|---|---|

| Primary License Type | 3-20 (resident) or 7-20 (non-resident) | Public Adjuster License (specific requirements) |

| DHS Recognition | 70-20 recognized in 18 states | Accepts Florida 70-20 DHS |

| Regulatory Stringency | Highly regulated with strict enforcement | Less restrictive for some categories |

For professionals consideringhow to become a claims adjuster in Florida, the licensing pathway involves pre-licensing education, passing state examinations, and meeting continuing education requirements. The investment in proper licensing ensures adjusters can serve clients in Tampa, Orlando, Jacksonville, and throughout Florida’s diverse insurance landscape.

Why Are Dual-Licensed Adjusters Becoming More Common?

The insurance industry in 2026 has witnessed a significant shift toward dual-licensed public adjusters who maintain credentials in multiple states. This trend reflects several converging factors: increased natural disaster frequency, remote work capabilities, and clients with multi-state property portfolios.

National firms are leading this movement.Companies likeRockwall National Public Adjustersand Prime Adjustments now maintain licenses in both Colorado and Florida, enabling seamless service for clients regardless of property location. This dual-licensing strategy provides several advantages: immediate response capabilities when disasters strike either state, deeper understanding of regional claim challenges, and the ability to serve clients who own properties in both states.

The Florida 70-20 DHS license has become particularly attractive for adjusters seeking multi-state practices. Since this license is recognized in Colorado and 17 other states, it serves as a powerful credential for establishing credibility across jurisdictions. Adjusters holding this license can confidently work in Denver metro, Colorado Springs, and throughout the Front Range while maintaining their Florida authority.

This trend aligns withwhen to hire a public adjuster in Floridaconsiderations, as property owners benefit from working with professionals who understand comparative claim handling across different regulatory environments. A dual-licensed adjuster can draw on experience from both states to maximize claim outcomes.

What Are the Salary and Income Differences?

Compensation for public adjusters varies significantly between Colorado and Florida, reflecting differences in cost of living, claim volume, regulatory environment, and market maturity. Understanding these income disparities helps adjusters make informed career decisions and helps clients understand the value proposition of experienced professionals.

As of 2026,Florida public adjusters earn $100,000 to $120,000 annuallyin full-time positions, often supplemented by commission and performance bonuses. The state’s high volume of hurricane, flood, and wind damage claims creates consistent demand for adjuster services. Many Florida positions aresales-driven and commission-based, requiring adjusters to generate their own client leads while offering substantial upside for top performers.

Colorado public adjusters typically earn$50,000 to $80,000 annually, with top performers at firms like Noble Public Adjusting Group reaching six-figure incomes through exceptional client service and claim negotiation skills. While the base compensation is lower than Florida, Colorado’s lower cost of living in many areas outside Denver can make these salaries competitive in terms of purchasing power.

Structure:Commission-based with bonuses

Job Listings:323 positions (2026)

Key Markets:Tampa, Miami, Orlando, Jacksonville

Top Performers:Six-figure potential

Schedule:Flexible, remote options

Key Markets:Denver, Colorado Springs, Boulder

Advantage:Multi-state client base

Flexibility:Choose high-value markets

Positioning:Elite specialist status

Dual-licensed adjusters who maintain active practices in both states often command the highest compensation, with income ranging from$120,000 to $200,000 or more annually. These professionals can strategically focus on the most lucrative claims in either market, travel to where disaster-related demand is highest, and serve premium clients with multi-state property portfolios.

When consideringpublic adjuster fees in Florida, it’s important to understand that adjusters typically work on contingency. Their fees are tied directly to claim outcomes, incentivizing maximum settlements for clients while allowing adjusters to earn premiums commensurate with their expertise.

What Are Florida’s Specific Public Adjuster Regulations?

Florida maintains some of the nation’s most comprehensive public adjuster regulations, designed to protect consumers while ensuring professional standards across the industry. These rules directly impact how Colorado-licensed adjusters can operate within Florida and what clients should expect when working with licensed professionals.

Fee caps represent a cornerstone of Florida’s regulatory framework.For claims tied to a state-declared emergency (hurricanes, tropical storms, etc.), public adjusters can chargeno more than 10% of the claim paymentfor one year following the emergency declaration. After that initial year, the fee cap increases to20% of the settlement amount. These limitations protect vulnerable policyholders during catastrophic events while ensuring adjusters receive fair compensation for their expertise.

Florida also provides strong consumer protection through contract cancellation rights. Clients may cancel a public adjuster contract within10 business days without penaltyunder normal circumstances. For contracts signed during a state-declared emergency, the cancellation period extends to30 days, giving property owners additional time to make informed decisions during stressful post-disaster periods.

The Florida Department of Financial Services actively monitors for unlicensed adjusters and fraudulent practices. AnInsurance Fraud Hotline at 1-800-378-0445allows consumers to report suspicious activity, including adjusters encouraging overstated claims or operating without proper licensing. This enforcement mechanism protects both ethical adjusters and the property owners they serve.

Recent guidelines for public adjuster contracts in Floridahave further strengthened transparency requirements, mandating clear disclosure of fees, services, and adjuster responsibilities. These regulations ensure property owners in Tampa, Fort Myers, and throughout Florida’s coastal communities understand exactly what they’re agreeing to when hiring professional representation.

How Can a Colorado Adjuster Work in Florida Legally?

Colorado-based public adjusters seeking to serve Florida clients must navigate specific licensing pathways to ensure full legal compliance. The process requires understanding reciprocity agreements, obtaining proper credentials, and maintaining ongoing education in both jurisdictions.

The most straightforward path involves obtaining theFlorida 7-20 Non-Resident All-Lines Adjuster License. This credential allows out-of-state adjusters to represent Florida policyholders legally without establishing Florida residency. The application process includes passing the Florida adjuster examination, submitting fingerprints for background checks, and demonstrating good standing in their home state.

Alternatively, Colorado adjusters already holding certain professional credentials may qualify forlicensing by endorsement, which recognizes equivalent out-of-state licenses and professional experience. This pathway typically requires proof of active licensing in Colorado, clean regulatory history, and completion of Florida-specific continuing education requirements.

For adjusters planning extensive Florida operations, establishing a Florida-based business entity and obtaining resident licensing may provide advantages. This approach signals commitment to the Florida market, builds local credibility with Tampa and Miami clients, and simplifies ongoing compliance with state regulations.

Conversely,discussions among insurance appraisal professionalsreveal that Florida adjusters seeking Colorado work benefit from the state’s recognition of the Florida 70-20 DHS license. This reciprocity eliminates redundant licensing requirements and allows immediate practice in Colorado once the Florida credential is obtained.

Understandinghow public adjusters get paid in Floridais essential for Colorado adjusters entering the market. The contingency-based model means adjusters must develop strong negotiation skills, damage assessment expertise, and client communication abilities to succeed in Florida’s competitive environment.

Many successful dual-licensed adjusters maintain professional memberships in organizations serving both states, attend regional continuing education conferences, and build referral networks that span Colorado’s mountain communities and Florida’s coastal cities. This integrated approach positions adjusters as true cross-state specialists rather than outsiders attempting to practice in unfamiliar jurisdictions.

For property owners seeking representation, working withGlobal Public Adjustersensures access to properly licensed professionals who understand both state regulatory environments. Our team maintains all necessary credentials to serve clients throughout Florida, including Tampa’s unique storm damage challenges, while bringing insights from diverse markets including Colorado.

People Also Ask

Can a Colorado public adjuster represent me on a Florida claim?

Only if the Colorado adjuster also holds a valid Florida license (3-20, 7-20, or 70-20 DHS). Florida law requires all public adjusters representing policyholders within the state to maintain proper Florida licensing, regardless of where they’re based or what other state licenses they hold.

What is the Florida 70-20 DHS license?

The Florida 70-20 Designated Home State (DHS) license is a prestigious adjuster credential recognized in 18 states including Colorado. It allows adjusters to practice in multiple jurisdictions without obtaining separate licenses in each state, making it highly valuable for multi-state insurance professionals.

How much do public adjusters charge in Florida versus Colorado?

Florida has statutory fee caps: 10% for emergency-declared claims (first year) and up to 20% for other claims. Colorado lacks specific statutory caps, allowing market-based fee negotiations typically ranging from 8% to 15% depending on claim complexity, though individual agreements vary based on specific circumstances and claim values.

Why would someone want dual licenses in Colorado and Florida?

Dual licensing enables adjusters to serve clients in both states legally, respond to disasters regardless of location, serve clients with multi-state properties, and command premium fees as specialized cross-jurisdictional experts. It also provides income stability by accessing two distinct insurance markets with different seasonal claim patterns.

Are Florida public adjusters more experienced than Colorado adjusters?

Not necessarily, though Florida’s higher claim volume (hurricanes, tropical storms) means adjusters there often handle more claims annually. Colorado adjusters develop specialized expertise in hail damage, wildfire claims, and winter storm losses. The best adjusters in both states demonstrate exceptional skills, and dual-licensed professionals combine insights from both markets.

What happens if an unlicensed adjuster represents me in Florida?

Using an unlicensed adjuster can void your representation agreement, expose you to liability, and result in no legal recourse if the adjuster performs inadequately. Florida actively prosecutes unlicensed adjusters, and insurance companies may refuse to negotiate with improperly credentialed representatives, potentially harming your claim outcome.

Frequently Asked Questions

How long does it take to get a Florida adjuster license for a Colorado resident?+

The process typically takes 4 to 8 weeks from application submission to license issuance. This includes completing pre-licensing education, passing the state examination, submitting fingerprints and background checks, and awaiting Florida Department of Financial Services approval. Expedited processing may be available during peak disaster seasons.

What types of claims do Florida public adjusters handle most frequently?+

Florida public adjusters primarily handle hurricane damage, wind and hail claims, water damage from tropical storms, roof damage, flooding (when covered), and sinkhole claims in certain regions. In Tampa specifically, hurricane-related wind damage and storm surge claims represent the majority of cases, especially following major weather events that impact the Gulf Coast.

Can I hire a public adjuster before filing my insurance claim in Florida?+

Yes, hiring a public adjuster before filing is often advantageous. They can document damage comprehensively from the start, ensure your initial claim submission is thorough and accurate, and prevent common mistakes that lead to claim denials or undervalued settlements. Many Florida property owners contact adjusters immediately after discovering damage to maximize claim outcomes.

Do dual-licensed adjusters charge higher fees than single-state adjusters?+

Fees are primarily determined by state regulations (like Florida’s statutory caps) rather than the number of licenses an adjuster holds. However, dual-licensed adjusters with extensive multi-state experience may position themselves as premium specialists, potentially commanding fees at the higher end of allowable ranges due to their broader expertise and proven track record across different regulatory environments.

What continuing education is required for Florida public adjusters?+

Florida requires licensed public adjusters to complete continuing education credits every licensing period to maintain active status. Requirements include courses on ethics, Florida insurance law updates, and industry best practices. Dual-licensed adjusters must meet continuing education requirements in both Florida and Colorado to maintain credentials in both states.

How do I verify a public adjuster’s Florida license status?+

Visit the Florida Department of Financial Services website and use their license verification tool to confirm an adjuster’s credentials, check for disciplinary actions, and verify their license is current and in good standing. Always verify licensing before signing any representation agreement, especially when working with adjusters claiming multi-state credentials.

What should Tampa homeowners look for when hiring a public adjuster?+

Tampa homeowners should verify Florida licensing, ask about experience with similar claims (hurricane, wind, water damage), request references from recent clients, understand the fee structure clearly, and ensure the adjuster has local market knowledge including Tampa-specific building codes, typical repair costs, and relationships with local contractors. Experience with Gulf Coast hurricane claims is particularly valuable in the Tampa area.

Key Takeaways

- Only Florida-licensed public adjusters can legally represent policyholders on claims within Florida, regardless of licenses held in other states like Colorado.

- TheFlorida 70-20 DHS license is recognized in 18 states including Colorado, making it the premier credential for multi-state insurance professionals.

- Florida public adjusters earn $100,000 to $120,000 annuallywhile Colorado adjusters earn $50,000 to $80,000, with dual-licensed professionals commanding $120,000 to $200,000+ through multi-market practices.

- Florida fee caps limit charges to 10% for emergency claims (first year) and 20% for non-emergency claims, providing consumer protection while ensuring fair adjuster compensation.

- 323 public adjuster positions are available in Florida as of 2026, reflecting strong demand for licensed professionals in the state’s active insurance market.

- Dual-licensed adjusters offer distinct advantagesincluding immediate disaster response in either state, expertise across different claim types, and the ability to serve clients with multi-state property portfolios.

- Proper licensing verification is criticalbefore hiring any public adjuster, with Florida’s Department of Financial Services providing online verification tools to confirm credentials and check disciplinary history.

The intersection of Colorado and Florida public adjuster licensing represents an evolving frontier in the insurance claims industry. As natural disasters become more frequent and severe, property owners increasingly benefit from working with professionals who understand multiple regulatory environments and can bring insights from diverse markets to maximize claim outcomes.

Whether you’re a homeowner in Tampa facing hurricane damage, a Colorado adjuster seeking to expand your practice into Florida’s lucrative market, or a dual-licensed professional serving clients across both states, understanding the legal requirements, income opportunities, and regulatory frameworks is essential for success. The key lies in proper licensing, ongoing education, and commitment to ethical representation that serves clients’ best interests.

For Florida property owners seeking expert claims representation, partnering with a properly licensed public adjuster makes the difference between accepting an insurance company’s initial offer and receiving the full compensation you deserve.Contact Global Public Adjusterstoday to connect with licensed professionals who understand both Florida’s unique regulatory environment and best practices from markets nationwide, including Colorado’s specialized claim handling approaches.