Public Adjusting Firm in Florida: Complete 2026 Guide to Claims Representation

Quick Answer

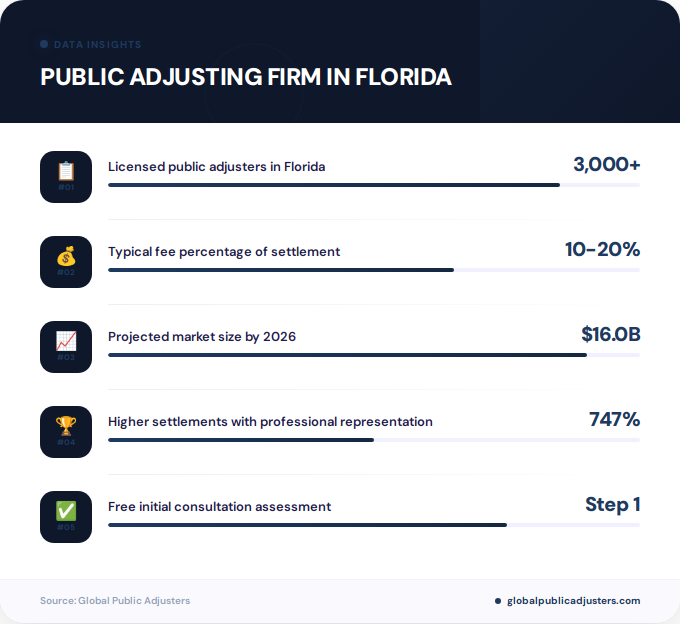

A public adjusting firm in Florida is a licensed business that represents policyholders (not insurance companies) during property insurance claims, working to document damage, estimate losses, and negotiate settlements. Florida has over 3,000 licensed public adjusters serving what is projected to be a $16.0 billion third-party claims adjusting market in 2026, with fees typically ranging from 10% to 20% of the claim settlement depending on the circumstances.

Did you know that Florida property insurance claims involving public adjusters have historically resulted in settlements up to747% higherthan claims handled without professional representation? In a state where hurricanes, flooding, and property damage are constant threats, this statistic underscores why thousands of Florida homeowners and businesses turn topublic adjusting firms in Floridaeach year.

Florida’s unique climate, high property values, and complex insurance environment have created the nation’s most active market for public adjusting services. Withmore than 3,000 licensed public adjustersworking across the state, from Miami to Tampa to Orlando, the profession has become essential for property owners navigating challenging insurance claims.

This comprehensive guide explores everything you need to know about public adjusting firms in Florida, including how they work, what they cost, licensing requirements, and how to choose the right firm for your property damage claim in 2026.

What Is a Public Adjusting Firm in Florida?

Apublic adjusting firm in Floridais a licensed business entity that employs or contracts with public adjusters to represent property owners during insurance claims. Unlike insurance company adjusters who work for the insurer, public adjusters work exclusively for you, the policyholder.

These firms operate under strict licensing requirements established by theFlorida Department of Financial Services under Chapter 626of Florida Statutes. Public adjusters must complete mandatory education, pass state exams, maintain continuing education, and carry appropriate insurance to protect clients.

Public adjusting firms provide comprehensive claims services including damage assessment, documentation preparation, loss estimation, policy review, and direct negotiation with insurance carriers. They handle all types of property damage claims, from minor water leaks to catastrophic hurricane damage affecting entire commercial complexes.

How Does a Public Adjusting Firm in Florida Work?

The process begins when a property owner contacts a public adjusting firm after experiencing property damage. Most firms offer free initial consultations to assess whether professional representation would benefit the claim. If you decide to proceed, you’ll sign a representation contract outlining the firm’s responsibilities and fee structure.

Once retained, thepublic adjusting firm in Floridatakes over communication with your insurance company. They conduct a comprehensive inspection of the damage, document everything with photographs and detailed notes, and prepare a complete claim package. This includes itemized damage estimates, policy analysis identifying all covered losses, and supporting documentation.

The firm then submits the claim to your insurance company and handles all negotiations.Professional insurance claims adjusters in Floridaunderstand policy language, coverage limitations, and negotiation tactics that maximize settlements. They respond to insurance company questions, counter lowball offers, and push for fair compensation based on policy terms.

According toStrategic Claim Consultants’ analysis of public adjuster effectiveness, professional representation ensures that insurance carriers properly apply policy terms and pay all covered losses rather than minimizing payouts to protect their bottom line.

What Is the Size of Florida’s Public Adjusting Market?

Florida’s public adjusting industry is the largest and most sophisticated in the United States. The state’s third-party administrators and insurance claims adjusters market isestimated at $16.0 billion in 2026, reflecting the enormous scale of property insurance activity in the Sunshine State.

Several factors drive Florida’s massive public adjusting market. The state faces constant weather-related risks including hurricanes, tropical storms, flooding, and severe thunderstorms. Florida’s high property values and dense coastal development create significant insurance exposure. Additionally, Florida’s insurance market has experienced increased claim disputes and carrier insolvencies, making professional representation more valuable.

| Market Metric | 2026 Florida Data | Significance |

|---|---|---|

| Market Revenue | $16.0 billion | Third-party claims adjusting industry size |

| Licensed Adjusters | 3,000+ | Active public adjusters serving Florida |

| Average Compensation | $68,829/year | Median adjuster earnings (range $61K–$104K) |

The concentration of public adjusting firms is highest in South Florida counties including Miami-Dade, Broward, and Palm Beach, followed by Tampa Bay, Orlando, and Jacksonville metro areas. This distribution reflects population density, property values, and historical storm exposure.

How Much Does a Public Adjusting Firm Charge in Florida?

Public adjusting firms in Florida typically work on acontingency fee basis, meaning they receive a percentage of your final insurance settlement. This arrangement aligns the firm’s interests with yours, as they only get paid when you receive payment from your insurer.

Florida law caps public adjuster feesat specific levels depending on the claim circumstances. For standard property damage claims filed under normal circumstances, the maximum fee is20% of the settlement amount. However, for claims filed within the first year after a governor-declared state of emergency or catastrophe, the fee cap drops to10%.

In practice, fees typically range from10% to 20% of the total settlement, with exact percentages negotiated based on claim complexity, property value, damage severity, and timing. Larger commercial claims may negotiate lower percentages due to higher settlement amounts. Some firms charge additional fees for supplemental claims (additional damage discovered after initial settlement).

Pricing for public adjusting services varies based on your specific claim circumstances, property type, damage extent, and policy complexity. Reputable firms provide transparent contracts clearly stating fee percentages and explaining when fees apply. Always review the contract carefully and ask questions about any provisions you don’t understand before signing.

It’s important to understand when fees are calculated. Most contracts specify that fees apply to the gross settlement amount (before deducting your deductible). Some firms also charge fees on depreciation amounts recovered through Recoverable Depreciation clauses.Understanding public adjuster costs in Orlandoand throughout Florida helps you make informed decisions about representation.

What Are Florida’s Licensing Requirements for Public Adjusters?

Florida maintains some of the nation’s most rigorous licensing standards for public adjusters. All public adjusters operating in Florida must be licensed through the Florida Department of Financial Services and comply with Chapter 626 of Florida Statutes.

To obtain a Florida public adjuster license, candidates must complete approved pre-licensing education, pass a state examination demonstrating knowledge of insurance policies and claims handling, submit fingerprints for background checks, and meet character and fitness standards. Licensed adjusters must also maintain continuing education requirements to keep their licenses active.

Public adjusting firms themselves must register with the state and ensure that all adjusters working on Florida claims hold valid licenses. Firms must carry errors and omissions insurance to protect clients from professional mistakes. The Department of Financial Services maintains public records of all licensed adjusters, disciplinary actions, and complaint histories.

When considering apublic adjusting firm in Florida, always verify that the firm and individual adjusters are properly licensed. You can check license status through the Florida Department of Financial Services website. Working with unlicensed adjusters is illegal in Florida and provides no legal protections if problems arise.

Why Should You Hire a Public Adjusting Firm in Florida?

The primary benefit of hiring a public adjusting firm is professional expertise in navigating complex insurance claims. Insurance policies contain technical language, coverage limitations, and subtle clauses that affect claim outcomes. Public adjusters understand these nuances and ensure all covered losses are properly documented and claimed.

Florida’s insurance environment has become increasingly challenging for policyholders. Many carriers have tightened claim handling procedures, increased documentation requirements, and scrutinized claims more aggressively.Professional representation levels the playing fieldwhen dealing with experienced insurance company adjusters and legal teams.

Public adjusting firms also save you significant time and stress. Managing an insurance claim while simultaneously dealing with property damage, displacement, business interruption, and repairs is overwhelming. The firm handles all communication with the insurance company, allowing you to focus on your life and business.

For complex claims involving extensive damage, multiple building systems, or business interruption, professional documentation and estimation are essential. Public adjusters use industry-standard software, work with specialized contractors, and prepare comprehensive claim packages that withstand insurance company scrutiny. This thoroughness often results in substantially higher settlements than policyholders achieve on their own.

Understanding when to hire a public adjuster in Floridacan significantly impact your claim outcome. While you can hire an adjuster at any point during your claim, earlier engagement typically produces better results.

What Results Can You Expect From a Florida Public Adjuster?

Data on public adjuster effectiveness demonstrates significant value for policyholders. A Florida legislative analysis examining Citizens Property Insurance claims from 2008 to 2009 found dramatic differences between claims handled with and without public adjusters.

For catastrophic claims (typically hurricane damage), public-adjuster-involved claims resulted in payments747% higherthan claims without professional representation. For non-catastrophic claims (such as water damage, fire, or other losses), settlements averaged574% higherwith public adjuster involvement.

Claim Type:Hurricanes, major storms

Time Period:2008-2009 data

Claim Type:Water, fire, general damage

Time Period:2008-2009 data

Negotiation:Expert-level

Policy Knowledge:Advanced

These statistics reflect several factors. Public adjusters identify damage and coverage that policyholders often miss. They prepare detailed estimates using professional software and pricing databases. They understand policy language and argue effectively for coverage of disputed items. They negotiate persistently and professionally to maximize settlements.

Individual results vary based on specific circumstances including policy terms, damage extent, documentation quality, and carrier practices. However, the data consistently shows that professional representation produces substantially better outcomes for Florida policyholders across all claim types.

How Do You Choose the Right Public Adjusting Firm in Florida?

Selecting the rightpublic adjusting firm in Floridarequires careful consideration of several factors. Start by verifying licensing and credentials through the Florida Department of Financial Services. Confirm that the firm and individual adjusters hold active, clean licenses with no recent disciplinary actions.

Experience matters significantly in public adjusting. Look for firms with proven track records handling claims similar to yours. A firm specializing in residential hurricane damage may not be the best choice for a complex commercial water loss. Ask about specific experience with your property type, damage type, and insurance carrier.

Check references and reviews from past clients. Reputable firms should readily provide references and have positive online reviews. Be cautious of firms with numerous complaints or unresolved issues. Professional associations like the National Association of Public Insurance Adjusters indicate industry commitment and professional standards.

Interview multiple firms before deciding. Ask about their claim handling process, communication practices, fee structure, and estimated timeline. Understand exactly what services they provide and what responsibilities remain yours. A quality firm will answer all questions thoroughly and never pressure you to sign immediately.

Review the representation contract carefully before signing. Ensure you understand the fee percentage, when fees apply, how supplemental claims are handled, and contract termination provisions. Don’t hesitate to negotiate terms or request clarifications.Reputable public adjusting firmswant informed clients and transparent relationships.

Local expertise is valuable in Florida’s diverse insurance market.Public adjusters in Tampa,Jacksonville, and other Florida cities often have specific experience with regional carriers, local building codes, and area-specific damage patterns that benefit your claim.

What Are Current Trends in Florida Public Adjusting?

Florida’s public adjusting industry continues evolving in response to market conditions, regulatory changes, and policyholder needs. Several key trends are shaping the profession in 2026 and beyond.

Increased specialization is a major trend. Rather than handling all claim types, many firms now focus on specific niches such as hurricane damage, water intrusion, commercial losses, or high-value residential properties. This specialization allows deeper expertise and better outcomes in complex situations.

Technology adoption has accelerated dramatically. Modern public adjusting firms use drones for roof and property inspections, thermal imaging to detect hidden water damage, 3D scanning for accurate measurements, and sophisticated estimating software. These tools improve documentation quality and claim presentation.

The regulatory environment continues tightening. Florida has implemented stricter fee caps after declared emergencies, enhanced licensing requirements, and increased oversight of public adjuster practices. These changes aim to protect consumers while maintaining professional standards. Reputable firms embrace these regulations as protecting both clients and the profession.

Knowing when you need a public adjusterhas become clearer as firms provide better education about their services. Many firms now offer free claim reviews, educational resources, and transparent information about when professional representation adds value versus when policyholders can reasonably handle claims themselves.

Post-disaster claim volume remains a persistent challenge. After major hurricanes or widespread storm events, demand for public adjusters far exceeds supply. This creates extended wait times and sometimes attracts less-qualified firms seeking quick profits. Building relationships with established firms before disasters strike can ensure access to quality representation when you need it most.

People Also Ask

What is the difference between a public adjuster and an insurance adjuster?

A public adjuster works for the policyholder and represents your interests during the claim, while an insurance adjuster works for the insurance company and represents the carrier’s interests. Public adjusters are paid by you to maximize your settlement, whereas company adjusters are paid by insurers to minimize payouts.

How long does a public adjuster have to settle a claim in Florida?

Florida law requires insurance companies to settle claims within specific timeframes, typically 90 days for most property claims, but the public adjuster’s timeline depends on claim complexity, insurer responsiveness, and documentation requirements. Most claims are resolved within 3 to 6 months, though complex or disputed claims can take longer.

Can I switch public adjusters in Florida?

Yes, you can switch public adjusters in Florida, though your original contract may contain provisions about fees for work already completed. Review your contract’s termination clause carefully and consult with a new adjuster before making changes to understand potential obligations and ensure continuous representation.

Do public adjusters work on denied claims in Florida?

Yes, many public adjusting firms in Florida specialize in appealing denied claims. They review the denial reasoning, gather additional evidence, identify policy provisions that support coverage, and submit appeals with comprehensive documentation that addresses the insurer’s concerns.

What types of claims do Florida public adjusters handle?

Florida public adjusters handle all types of property insurance claims including hurricane damage, water damage, fire and smoke damage, theft, vandalism, mold, roof damage, sinkhole claims, and business interruption losses. Most firms handle both residential and commercial claims, though some specialize in specific damage types or property categories.

Are public adjuster fees tax deductible in Florida?

Public adjuster fees may be tax deductible as casualty loss expenses or business expenses depending on the property type and circumstances. Consult with a tax professional about your specific situation, as tax treatment depends on whether the property is personal residence, rental property, or business property.

Frequently Asked Questions

When should I contact a public adjusting firm in Florida?+

Contact a public adjusting firm as soon as possible after discovering property damage, ideally before filing your insurance claim. Early involvement allows the adjuster to document damage before repairs begin, ensure proper claim filing, and establish your representation before the insurance company begins its investigation.

How do I verify a public adjuster’s license in Florida?+

Verify public adjuster licenses through the Florida Department of Financial Services website by searching their license lookup database. You can search by name or license number to confirm active status, view license history, and check for any disciplinary actions or complaints.

What should I look for in a public adjusting contract?+

Look for clear fee percentages, specific services provided, contract duration and termination provisions, how supplemental claims are handled, and whether fees apply before or after your deductible. The contract should specify communication expectations, reporting frequency, and any circumstances where additional fees might apply beyond the stated percentage.

Can a public adjuster guarantee a specific settlement amount?+

No ethical public adjuster can guarantee a specific settlement amount because final settlements depend on policy terms, damage extent, documentation, and insurer decisions. Be wary of adjusters making promises about specific settlement amounts, as this is a red flag indicating potential unprofessional practices.

Will hiring a public adjuster delay my claim settlement?+

Hiring a public adjuster may initially extend the claim timeline because they conduct thorough documentation and prepare comprehensive claim packages, but this often results in faster final resolution because properly documented claims face fewer disputes. The investment in upfront time typically prevents lengthy back-and-forth negotiations and produces better final outcomes.

Do I need a public adjuster if my insurance company already sent an adjuster?+

Yes, you can and often should hire a public adjuster even after the insurance company sends their adjuster. The company adjuster represents the insurer’s interests, while your public adjuster represents you, ensuring all damage is properly identified, documented, and claimed under your policy terms.

What if I disagree with my public adjuster’s approach?+

Communicate concerns directly with your public adjuster, as most disagreements stem from misunderstandings about strategy or process. A professional firm will explain their approach, answer questions, and adjust tactics based on your input. If problems persist, review your contract’s termination provisions and consider seeking a second opinion from another firm.

Key Takeaways

- Public adjusting firms in Florida represent policyholders, not insurance companies, during property damage claims and work to maximize settlements under policy terms.

- Florida’s public adjusting market is valued at $16.0 billion in 2026, with over 3,000 licensed adjusters serving property owners across the state.

- Fees typically range from 10% to 20% of claim settlements, with Florida law capping catastrophe claims at 10% and standard claims at 20%.

- Data shows settlements 574% to 747% higherwhen policyholders use public adjusters compared to handling claims independently.

- All Florida public adjusters must be licensedthrough the Department of Financial Services and comply with Chapter 626 requirements.

- Early engagement produces better results, so contact a public adjusting firm as soon as possible after discovering property damage.

- Verify credentials, check references, and review contracts carefullybefore hiring any public adjusting firm to ensure professional, ethical representation.

Navigating Florida’s complex property insurance environment requires expertise, persistence, and detailed knowledge of policy terms and claims procedures. A qualifiedpublic adjusting firm in Floridaprovides professional representation that levels the playing field when negotiating with insurance carriers.

Whether you’re dealing with hurricane damage in Miami, water intrusion in Tampa, fire loss in Jacksonville, or any other property damage across Florida, professional representation can significantly impact your claim outcome. The data clearly demonstrates that policyholders who hire public adjusters receive substantially higher settlements than those who handle claims independently.

Related:How to Get Your Florida Public Adjuster License in Orlando: Complete 2026 Licensing Guide

Related:Florida Public Adjusters License in Orlando: Complete 2026 Licensing Guide

Related:Fire Claims Adjuster in Jacksonville: Your Complete 2026 Guide to Fire Damage Recovery

Related:How to File an Insurance Claim in Florida: Jacksonville Homeowners and Auto Policy Holders Guide

Related:How to Appeal an Insurance Claim Denial in Orlando: Your Complete 2026 Guide

If you’re facing a property insurance claim in Florida, don’t navigate the process alone.Contact our experienced teamfor a free claim review. We’ll assess your situation, explain your options, and help you make informed decisions about professional representation. Our licensed adjusters serve property owners throughout Florida with transparent pricing, ethical practices, and proven results.