What Does a Public Adjuster Do in Tampa: Your Complete 2026 Guide

Quick Answer

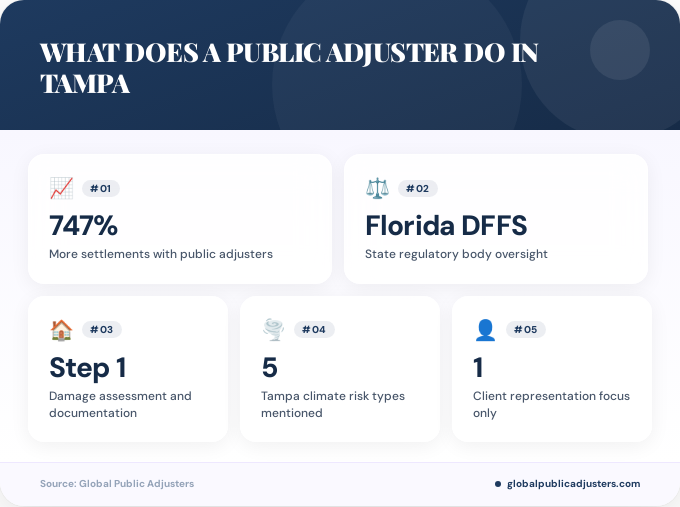

A public adjuster in Tampa is a licensed professional who represents homeowners and businesses exclusively during insurance claims, inspecting damage, documenting losses, preparing proof-of-loss reports, and negotiating with insurers for maximum settlements. Unlike insurance company adjusters who work for the insurer, public adjusters work solely for the policyholder and typically recover 747% more in settlements than those filing alone.

When a hurricane tears through Tampa Bay, or a hidden water leak destroys your South Tampa home, the insurance claim process can feel overwhelming. Did you know thathomeowners with public adjusters recover 747% more in settlementsthan those filing claims on their own? That staggering statistic reveals a critical gap in how most Tampa residents approach property damage claims, and why understanding what a public adjuster does can make the difference between financial hardship and full recovery.

Tampa’s unique coastal climate brings significant property risks, from hurricane-force winds to tropical storm flooding and persistent moisture damage. When disaster strikes, you’re not just dealing with repairs; you’re navigating complex insurance policies, documentation requirements, and negotiations with insurance company representatives whose interests don’t align with yours. This is where a public adjuster becomes invaluable.

Whether you’re a homeowner in Westchase dealing with roof damage, a business owner in Downtown Tampa facing fire loss, or a property manager in Carrollwood handling water intrusion, understandingwhat a public adjuster does in Tampaempowers you to make informed decisions during your most vulnerable moments.

What Is a Public Adjuster in Tampa?

A public adjuster in Tampa is alicensed insurance professional who works exclusively for policyholders, not insurance companies. Unlike the adjuster your insurance company sends to evaluate your claim, a public adjuster represents your interests throughout the entire claims process.

Public adjusters are regulated by theFlorida Department of Financial Services and must meet strict licensing requirements, including passing state examinations, completing background checks, posting bonds, and fulfilling apprenticeship requirements. This regulatory framework ensures that Tampa residents work with qualified professionals who understand both insurance law and local property damage issues.

The fundamental difference between a public adjuster and an insurance company adjuster lies in representation. While insurance adjusters work to minimize payouts for their employer (the insurance company), public adjusters maximize settlements for their client (you, the policyholder). This alignment of interests creates a powerful advocacy relationship, especially in a market like Tampa where property values and reconstruction costs continue to rise.

What Are the Core Responsibilities of a Public Adjuster in Tampa?

Public adjusters in Tampa perform comprehensive services that span the entire insurance claims lifecycle. Their responsibilities extend far beyond simple damage inspection, encompassing legal, technical, and negotiation expertise tailored to Florida’s unique property insurance landscape.

Damage Assessment and Documentation

The first critical responsibility involves conductingthorough property inspections to identify all damage, including hidden issues that untrained eyes might miss.Tampa public adjusters specialize in identifying hurricane, flood, wind, water leaks, fire, mold, and storm-related damagecommon to the region’s subtropical climate.

Documentation involves high-resolution photography, detailed written reports, moisture readings, structural assessments, and comprehensive inventories of damaged personal property. This evidence forms the foundation of your claim and must withstand scrutiny from insurance company representatives and, if necessary, legal proceedings.

Policy Review and Coverage Analysis

Public adjusters meticulously review your insurance policy to identifyevery coverage provision that applies to your loss. Many Tampa homeowners don’t fully understand their policy limits, exclusions, or additional coverage options like ordinance and law provisions, which can significantly impact settlement amounts.

This analysis helps determine the maximum potential recovery and identifies areas where insurance companies might attempt to deny or reduce legitimate claims. Understanding your policy’s nuances is especially critical in Tampa, where flood insurance, windstorm coverage, and sinkhole provisions create complex coverage scenarios.

Proof-of-Loss Preparation

One of the most technical responsibilities involves preparing comprehensiveproof-of-loss reportsthat meet insurance company standards. Tampa public adjusters typically use industry-standard software like Xactimate to generate detailed estimates that insurance companies cannot easily dispute.

These reports itemize every damaged component, apply current material and labor costs specific to the Tampa market, and account for code upgrade requirements. The precision of these documents directly correlates with settlement outcomes, making this expertise invaluable for complex claims.

Negotiation and Settlement Advocacy

Perhaps the most valuable responsibility isnegotiating directly with insurance company adjustersto secure maximum settlements. Public adjusters understand insurer tactics, know when initial offers undervalue claims, and possess the documentation to justify higher payouts.

This negotiation process can involve multiple rounds of discussions, supplemental damage discoveries, and strategic pressure points that leverage policy language and legal precedents. For Tampa residents unfamiliar with insurance negotiations, this professional advocacy levels the playing field against well-resourced insurance companies.

How Does a Public Adjuster Work in Tampa?

The public adjuster process in Tampa follows a structured workflow designed to maximize efficiency and settlement outcomes. Understanding this process helps policyholders know what to expect when engaging these professionals.

Initial Consultation and Damage Inspection

Most Tampa public adjusters offerfree initial consultations and damage inspections. During this meeting, they assess your property damage, review your insurance policy, and explain how they can help. This no-obligation evaluation allows you to understand your claim’s potential value before committing to representation.

If you decide to proceed, you’ll sign a contingency fee agreement that outlines the adjuster’s compensation (typically 10-20% of the final settlement, though exact percentages vary by contract and claim complexity). Thecritical advantage of this arrangementis that you pay nothing unless your claim recovers funds.

Claim Filing and Documentation

The public adjuster handles all claim filing paperwork, ensuring submissions meet insurance company deadlines and requirements. They compile supporting documentation, including damage photos, repair estimates, policy coverage analyses, and loss inventories.

This comprehensive submission prevents the common delays that occur when insurance companies request additional information or claim incomplete documentation. Tampa’s high claim volume during hurricane season makes timely, complete submissions especially important for faster processing.

Ongoing Communication and Updates

Throughout the process, your public adjuster serves as theprimary point of contact with your insurance company. They handle all phone calls, emails, and correspondence, shielding you from the stress and time commitment that claims typically require.

Regular updates keep you informed of claim progress, settlement offers, and any additional information needed. This communication transparency ensures you remain in control of decisions while benefiting from professional representation.

Settlement Negotiation and Resolution

Once the insurance company makes an initial offer, your public adjuster evaluates it against their independent damage assessment. If the offer falls short (which commonly occurs), they present counterarguments supported by documentation, expert opinions, and policy language interpretations.

This back-and-forth continues until reaching a settlement both parties accept, or until it becomes clear that litigation may be necessary. While public adjusters cannot represent you in court (that requires an attorney), they can work collaboratively with legal counsel if disputes escalate to lawsuits.

| Public Adjuster Role | Insurance Adjuster Role |

|---|---|

| Represents policyholder interests | Represents insurance company interests |

| Works to maximize settlement | Works to minimize payout |

| Paid by policyholder (contingency fee) | Paid by insurance company (salary) |

Why Should Tampa Residents Hire a Public Adjuster?

The decision to hire a public adjuster in Tampa comes down to three compelling factors: settlement outcomes, time savings, and stress reduction. Each offers tangible benefits that far outweigh the contingency fee investment.

Dramatically Higher Settlements

The most persuasive reason is financial.Research shows homeowners with public adjusters recover 747% more in settlementsthan those navigating claims independently. This statistic isn’t surprising when you consider that insurance companies employ teams of adjusters, lawyers, and consultants to minimize payouts.

Without professional representation, most Tampa homeowners lack the technical knowledge to identify all covered damages, understand policy nuances, or counter lowball settlement offers. A public adjuster’s expertise directly translates to thousands or even tens of thousands of additional dollars in your pocket.

Time Efficiency and Convenience

Insurance claims consume enormous time and energy. Between documenting damage, researching contractors, communicating with adjusters, and negotiating settlements, the average claim requires dozens of hours over several weeks or months.

For Tampa residents managing careers, families, and the immediate aftermath of property damage, this time commitment proves overwhelming. Public adjusters handle every aspect of the process, allowing you to focus on temporary housing, family needs, and life continuity while they manage the bureaucratic complexities.

Expertise in Tampa-Specific Challenges

Tampa’s insurance landscape presents unique complications. Hurricane deductibles often differ from standard policy deductibles. Flood damage requires separate federal flood insurance claims. Wind versus water damage attribution affects coverage under different policy sections. Sinkholes create specialized claim requirements.

Local public adjusters understand these Tampa-specific nuances and how they impact claims. They know which contractors provide reliable estimates, which insurance companies use particular tactics, and how local building codes affect reconstruction requirements. This regional expertise proves invaluable for navigating Florida’s complex property insurance environment.

“The complexity of insurance claims in Tampa has increased significantly due to frequent weather events and evolving policy language. Public adjusters provide critical advocacy that ensures policyholders receive the full benefits they’ve paid premiums to secure. Their local expertise in Tampa’s building codes and weather patterns makes them indispensable during major losses.” – Tampa Insurance Law Expert

What Tampa-Specific Challenges Do Public Adjusters Handle?

Tampa’s geographic location along Florida’s Gulf Coast creates unique property damage scenarios that require specialized adjuster knowledge. Understanding these local challenges explains why choosing a Tampa-based public adjuster offers advantages over out-of-state firms.

Hurricane and Tropical Storm Damage

Tampa faces persistent hurricane threats during the annual June-to-November season. These powerful storms generatemultiple damage types simultaneously: wind damage to roofs and siding, water intrusion from wind-driven rain, flooding from storm surge, and secondary mold growth from prolonged moisture exposure.

Public adjusters in Tampa understand how to document and categorize each damage type to maximize coverage under different policy provisions. They know that wind damage falls under homeowners policies while flooding requires separate National Flood Insurance Program claims, and they coordinate both processes for comprehensive recovery.

Water Damage and Moisture Issues

Tampa’s subtropical humidity and frequent afternoon thunderstorms create persistent moisture challenges.Local public adjusters regularly handle claims for water leaks, plumbing failures, roof leaks, and resulting mold contamination.

These claims often involve disputes about when damage occurred, whether it resulted from sudden accidents (covered) or gradual deterioration (excluded), and the extent of necessary remediation. Tampa public adjusters use moisture meters, thermal imaging, and mold testing to document conditions that support covered loss arguments.

Sinkhole and Foundation Issues

Florida’s limestone geology creates sinkhole risks throughout the Tampa Bay area. When foundation cracks, floor settling, or structural damage appear, determining whether sinkholes caused the damage becomes critical for coverage.

Florida law requires insurers to investigate sinkhole claims when policyholders present supporting evidence. Public adjusters coordinate with structural engineers and geologists to document conditions, interpret test results, and argue for coverage when sinkholes contribute to property damage.

Fire and Smoke Damage

While less frequent than weather events, fire claims present significant documentation challenges. Public adjusters inventory all damaged personal property, assess structural damage, and quantify smoke odor remediation needs.

They also navigate additional living expense claims when fire damage renders homes uninhabitable, ensuring insurance companies cover reasonable temporary housing costs during reconstruction. This financial support proves essential for Tampa families displaced from their homes for weeks or months.

What Is the Difference Between a Public Adjuster and an Insurance Adjuster?

The distinction between public adjusters and insurance company adjusters represents the most fundamental concept in understanding property insurance claims. These two professionals serve opposite sides of the same transaction, creating fundamentally different outcomes for policyholders.

Representation and Loyalty

Insurance company adjusters (also called company adjusters or staff adjusters) work directly for insurance carriers. Their salaries, performance reviews, and career advancement depend on managing claim costs favorably for their employer. While most conduct themselves professionally, their loyalty lies with the insurance company, not the policyholder.

Public adjusters work exclusively for policyholders under contractual agreements. Their success depends entirely on maximizing client settlements, creating perfect alignment between their interests and yours. This represents a crucial difference in how claims are evaluated and negotiated. To learn more about these distinctions, review our guide onpublic adjuster versus insurance adjuster differences in Florida.

Compensation Structure

Company adjusters receive salaries or hourly wages regardless of individual claim outcomes. Some insurance companies even incentivize adjusters to keep claim costs below certain thresholds, creating direct conflicts of interest with policyholder recovery.

Public adjusters work on contingency, earning a percentage of the final settlement (no recovery means no fee). This compensation model ensures they pursue every dollar of legitimate coverage, as their payment directly correlates with your settlement amount.

Expertise and Specialization

Insurance company adjusters often handle hundreds of claims across multiple property types, damage scenarios, and geographic areas. This broad exposure provides general knowledge but limits deep expertise in specific damage types or local conditions.

Public adjusters typically specialize in particular claim types (water damage, fire, hurricane claims) within specific geographic markets. Tampa public adjusters develop expert-level knowledge of local building codes, contractor costs, weather patterns, and regional insurance company tactics that company adjusters rotating through multiple territories cannot match.

Negotiation Dynamics

When company adjusters negotiate, they’re essentially negotiating with themselves (their employer). They present settlement offers designed to resolve claims economically for the insurance company. Accepting these initial offers often leaves significant money on the table.

Public adjusters create genuine negotiation dynamics by presenting independent damage assessments, challenging undervalued estimates, and leveraging policy language that company adjusters might overlook or downplay. This adversarial-yet-professional relationship produces fair outcomes that reflect actual damage and policy coverage.

How Much Does a Public Adjuster Cost in Tampa?

Understanding public adjuster fees helps Tampa property owners make informed decisions about representation. The investment often pays for itself many times over through increased settlements.

Contingency Fee Structure

Tampa public adjusters typically work on contingency, charging a percentage of the final settlement. While exact percentages vary based on claim complexity, damage severity, and contract terms,fees generally range from 10% to 20% of the total recovery.

This structure eliminates upfront costs and financial risk for policyholders. If the adjuster recovers nothing, you owe nothing. The fee only applies to successful settlements, aligning incentives perfectly between adjuster and client.

Fee Variations Based on Claim Factors

Several factors influence where fees fall within the typical range. Hurricane claims during declared emergencies may have different fee caps under Florida law. Complex commercial claims involving business interruption often command higher percentages due to increased work requirements.

Simple residential claims with clear damage and cooperative insurers might settle at lower percentage ranges, while disputed claims requiring extensive documentation, multiple inspections, or prolonged negotiations justify higher fees. The key is that pricing varies based on your specific project’s complexity and the adjuster’s expected time investment.

When evaluating fees, consider the alternative. Recovering 100% of a $50,000 settlement on your own sounds better than 85% of a $150,000 settlement secured by a public adjuster, until you realize the adjuster’s expertise netted you an additional $77,500 after fees. The value proposition becomes clear when you focus on net recovery rather than gross percentages.

Value Beyond Settlement Amounts

Public adjuster fees also purchase time, stress reduction, and expertise you cannot easily quantify. The dozens of hours you’d spend researching policies, documenting damage, obtaining estimates, and negotiating have real economic value through lost work time or family disruption.

Additionally, professional representation reduces the emotional toll of confronting insurance company resistance, claim delays, and lowball settlement offers. For many Tampa residents recovering from property disasters, this peace of mind justifies the fee investment independent of settlement outcomes. For a detailed breakdown of costs, see our comprehensive guide onpublic adjuster fees in Florida.

What Qualifications Do Tampa Public Adjusters Need?

Florida maintains stringent licensing requirements for public adjusters, ensuring Tampa residents work with qualified professionals. Understanding these requirements helps you evaluate potential adjusters and verify their credentials.

State Licensing Process

All public adjusters practicing in Tampa must hold active licenses from theFlorida Department of Financial Services. The licensing process requires passing comprehensive state examinations covering insurance law, policy interpretation, claims handling, ethics, and Florida-specific regulations.

Applicants must also complete criminal background checks, submit fingerprints for FBI review, and demonstrate financial responsibility through surety bonds. These requirements weed out unqualified or unethical practitioners, protecting consumers from incompetent representation.

Continuing Education Requirements

Florida requires licensed public adjusters to complete24 hours of continuing education every two yearsto maintain their licenses. These courses cover emerging insurance issues, legal updates, new technologies, and ethical standards.

This ongoing education requirement ensures Tampa public adjusters stay current with evolving insurance policies, claims technologies, and legal precedents that affect claim outcomes. When hiring an adjuster, verify their license is active and in good standing through the Florida Department of Financial Services website.

Apprenticeship and Experience

Beyond formal education, public adjusters gain practical expertise through apprenticeships under experienced professionals. This hands-on training teaches them to recognize damage types, document losses effectively, use estimating software, and navigate insurer-specific claims processes.

When evaluating Tampa public adjusters, ask about their experience with claims similar to yours. An adjuster with 15 years handling hurricane damage brings more value to wind and flood claims than someone specializing in fire losses. Match adjuster expertise to your specific damage type for optimal results. Learn more aboutFlorida public adjuster licensing requirementsto verify credentials.

Professional Associations

Many qualified adjusters belong to professional organizations like theNational Association of Public Insurance Adjusters (NAPIA)or the Florida Association of Public Insurance Adjusters (FAPIA). These memberships indicate commitment to ethical standards, professional development, and industry best practices.

While not required, association membership signals professionalism and provides additional consumer protections through codes of ethics and dispute resolution processes.Industry associations also provide resources demonstrating the tangible value public adjusters bring to policyholders.

When Should You Hire a Public Adjuster in Tampa?

Timing matters when engaging public adjuster services. While you can hire representation at any point during the claims process, earlier engagement typically produces better outcomes.

Immediately After Damage Occurs

The ideal time to hire a public adjuster isimmediately after discovering property damage, before filing your insurance claim. Early involvement allows adjusters to document initial conditions, prevent secondary damage, and ensure claim filings include all necessary information.

This proactive approach prevents common mistakes like inadequate damage documentation, missed coverage provisions, or statements to insurance companies that later complicate claims. Tampa residents facing hurricane damage, major water intrusion, or fire losses benefit most from immediate public adjuster engagement. For guidance on optimal timing, see our article onwhen to hire a public adjuster.

After Receiving Unsatisfactory Settlement Offers

Even if you’ve already filed a claim, hiring a public adjuster after receiving a lowball settlement offer can salvage poor outcomes. Adjusters can review insurance company assessments, identify undervalued damages, and reopen negotiations with supporting documentation.

This mid-stream intervention works best before you’ve accepted and cashed settlement checks, which often contain legal language releasing insurers from further obligations. If you suspect your settlement undervalues your damage, consult a public adjuster before signing anything.

For Complex or High-Value Claims

Certain claim types virtually require professional representation due to their complexity.Hurricane damage involving both wind and flood coverage, commercial property losses including business interruption, claims exceeding $100,000, or disputes over damage causation all benefit from public adjuster expertise.

Similarly, if your insurance company denies your claim, disputes coverage, or requests extensive documentation you’re unsure how to provide, a public adjuster can navigate these challenges far more effectively than most property owners. For hurricane-related claims specifically, review our guide onhurricane damage claims and public adjusters.

When You Lack Time or Expertise

Practical considerations also drive hiring decisions. If your career, family responsibilities, or physical limitations prevent you from investing dozens of hours in claims management, a public adjuster provides essential support.

Similarly, if you lack construction knowledge, insurance policy literacy, or negotiation experience, professional representation ensures you don’t inadvertently harm your claim through procedural mistakes or uninformed decisions.

How to Choose the Right Public Adjuster in Tampa

Selecting the right public adjuster significantly impacts your claim outcome. Tampa’s market includes numerous qualified professionals, but finding the best fit for your specific needs requires careful evaluation.

Verify Licensing and Credentials

Start by confirming any prospective adjuster holds anactive Florida public adjuster license. Check the Florida Department of Financial Services website for license status, disciplinary actions, and complaint histories. Avoid adjusters operating without proper credentials or those licensed in other states but not Florida.

Also verify the adjuster carries errors and omissions insurance and maintains the required surety bond. These protections safeguard you if the adjuster makes costly mistakes or engages in unethical conduct.

Evaluate Local Experience

Prioritize Tampa-based adjusters with extensive local experience over national firms rotating adjusters through your market.Local expertise in Tampa’s weather patterns, building codes, and insurance company tacticsproduces superior results.

Ask how many claims they’ve handled in Tampa, their familiarity with your neighborhood’s construction types, and their relationships with local contractors and engineers who might support your claim. This regional knowledge proves invaluable during complex claims.

Review Specialization and Track Record

Match adjuster specialization to your claim type. If you’re filing aroof damage claim, choose someone with extensive roofing claim experience. For water damage, select an adjuster familiar withwater intrusion claims and mold remediation.

Request references from previous Tampa clients with similar claims. Contact these references to ask about settlement outcomes, communication quality, and overall satisfaction. Reputable adjusters willingly provide this information and demonstrate proven track records.

Compare Fee Structures and Contracts

Obtain written fee agreements from multiple adjusters before deciding. Compare not just percentages but also contract terms covering when fees are earned, how costs are handled, and what happens if you’re unsatisfied with services.

Avoid adjusters demanding large upfront fees (red flag) or those unwilling to explain fee calculations. Legitimate public adjusters work on contingency and clearly communicate all financial terms before you commit.

Assess Communication and Professionalism

Your initial interactions reveal how adjusters will handle your claim. Responsive communication, clear explanations, and professional presentations indicate quality service. If an adjuster seems rushed, vague about processes, or dismissive of questions, keep searching.

Trust matters enormously in this relationship. You’re granting access to your property, sharing financial information, and relying on someone to advocate for your interests. Choose an adjuster who inspires confidence through competence, transparency, and genuine concern for your recovery.

| Evaluation Factor | What to Look For | Red Flags |

|---|---|---|

| Licensing | Active Florida license, clean record | No license, out-of-state only, disciplinary actions |

| Experience | Local Tampa presence, similar claim expertise | No local experience, generalist approach |

| Fees | Contingency-based, written agreement | Large upfront fees, vague terms |

Key Takeaways

- Public adjusters in Tampa represent policyholders exclusively, not insurance companies, creating advocacy relationships that maximize claim settlements through expert damage assessment, policy interpretation, and skilled negotiation.

- Homeowners with public adjusters recover 747% more in settlementsthan those filing independently, demonstrating the substantial financial value professional representation provides during complex property insurance claims.

- Tampa’s unique climate challenges require specialized expertise, including hurricane damage, flood claims, moisture issues, sinkholes, and other weather-related losses that demand local knowledge of building codes and insurance tactics.

- Public adjusters work on contingency fees typically ranging from 10-20%of final settlements, eliminating upfront costs and aligning their success directly with maximizing your recovery.

- Florida licensing requirements ensure public adjusters meet strict standards, including state examinations, background checks, continuing education, and bonding that protect consumers from unqualified practitioners.

- Hiring a public adjuster immediately after damage occurs produces optimal results, allowing comprehensive documentation, proper claim filing, and strategic negotiation from the outset of the process.

- Choosing the right Tampa public adjuster requires verifying credentials, evaluating local experience, reviewing specialization in your claim type, comparing fee structures, and assessing communication quality and professionalism throughout initial consultations.

People Also Ask

How long does a public adjuster take to settle a claim in Tampa?

Settlement timelines vary significantly based on claim complexity, damage extent, and insurance company responsiveness, typically ranging from 30 days for straightforward claims to several months for complex hurricane or commercial losses. Tampa public adjusters work to expedite the process while ensuring thorough documentation supports maximum settlements.

Can I hire a public adjuster after my claim is denied?

Yes, public adjusters can review denied claims, identify errors in insurance company assessments, gather additional supporting evidence, and request claim reconsideration or file appeals. However, engaging an adjuster before filing or immediately after denial typically produces better outcomes than waiting until appeals deadlines approach.

Do public adjusters handle both residential and commercial claims in Tampa?

Most Tampa public adjusters handle both residential and commercial property claims, though some specialize in one sector. Commercial claims often involve additional complexities like business interruption, equipment losses, and liability exposures that require specialized expertise beyond standard homeowner claims.

What is the difference between a public adjuster and a public insurance adjuster?

These terms refer to the same profession; “public adjuster” and “public insurance adjuster” are used interchangeably. Both describe licensed professionals who represent policyholders during insurance claims, distinguishing them from insurance company adjusters who work for insurers.

Can a public adjuster help with flood insurance claims in Tampa?

Yes, experienced public adjusters handle National Flood Insurance Program (NFIP) claims and private flood insurance, navigating unique federal regulations and documentation requirements. Tampa’s coastal location makes flood claim expertise particularly valuable when storm surge or heavy rainfall causes property damage.

Will hiring a public adjuster delay my insurance claim settlement?

Public adjusters typically accelerate settlements by submitting complete, accurate documentation that prevents insurance company requests for additional information. While thorough claims may take slightly longer initially, comprehensive preparation reduces overall processing time and prevents the delays caused by incomplete filings or disputed valuations.

Frequently Asked Questions

Do I need a public adjuster for small claims in Tampa?+

While public adjusters primarily benefit complex or high-value claims, even small claims can benefit from professional representation if you lack time, insurance expertise, or negotiation confidence. Most adjusters offer free consultations to assess whether their services would add value to your specific situation, allowing you to make informed decisions.

How do I verify a public adjuster’s license in Tampa?+

Visit the Florida Department of Financial Services website and use their licensee search tool to verify any public adjuster’s active license status, view disciplinary history, and confirm credentials. You can also request the license number directly from the adjuster and cross-reference it with state records before signing any contracts.

What documentation should I gather before meeting a public adjuster?+

Bring your insurance policy declarations page, any correspondence with your insurance company, photos or videos of damage, repair estimates you’ve obtained, and documentation of temporary repairs or mitigation efforts. This information helps adjusters quickly assess your situation and provide accurate preliminary evaluations during initial consultations.

Can I negotiate public adjuster fees in Tampa?+

Public adjuster fees are often negotiable, particularly for large claims or straightforward damage scenarios. However, focus on overall value rather than just the lowest percentage, as experienced adjusters with proven track records of higher settlements often justify their fees through superior results that exceed the cost difference.

What happens if I’m unhappy with my public adjuster’s performance?+

Review your contract’s termination provisions, which typically allow either party to end the relationship with written notice. You may owe fees for work completed before termination, so address concerns directly with your adjuster first to resolve issues before considering contract termination or filing complaints with state regulators.

Will using a public adjuster affect my insurance rates in Tampa?+

Hiring a public adjuster itself does not directly affect your insurance rates; however, filing claims (regardless of representation) can impact future premiums. The decision to file claims should balance recovery needs against potential rate increases, a consideration your public adjuster can help you evaluate based on damage severity and policy terms.

How quickly should I contact a public adjuster after Tampa property damage?+

Contact a public adjuster as soon as possible after discovering damage, ideally within 24-48 hours for time-sensitive situations like water intrusion or ongoing weather threats. Early engagement allows proper damage documentation, prevents secondary issues, and ensures you meet insurance policy notification deadlines while evidence remains fresh.