Insurance Claims Public Adjuster in Florida: Your Complete 2026 Guide

Quick Answer

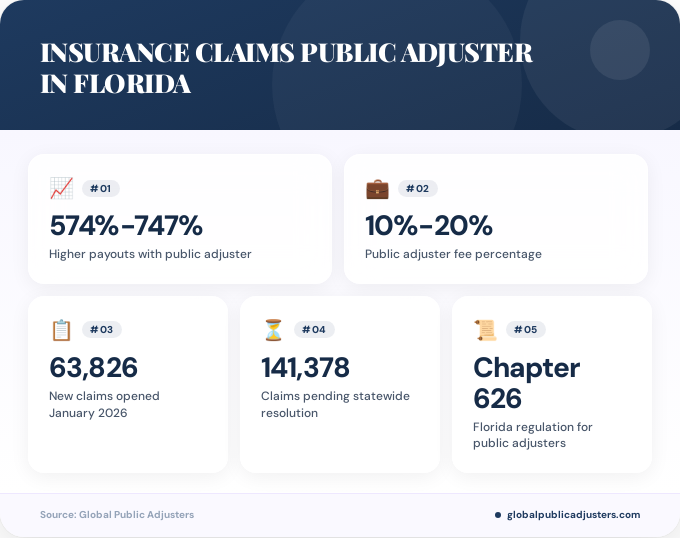

An insurance claims public adjuster in Florida is a licensed professional who represents policyholders during property insurance claims, handling everything from damage assessment to settlement negotiation for a fee typically between 10% and 20% of the claim payment. Florida public adjusters are regulated by the Department of Financial Services under Chapter 626 and have historically secured 574% to 747% higher payouts for policyholders compared to claims handled without professional representation.

Did you know that property insurance claims handled by public adjusters in Florida have historically resulted in settlements574% to 747% higherthan those negotiated directly by policyholders? With63,826 new property insurance claimsopened in January 2026 alone and over141,000 claims still pending statewide, understanding how an insurance claims public adjuster in Florida can protect your interests has never been more critical.

Florida’s unique position as the hurricane capital of the United States, combined with recent property insurance market volatility, creates an environment where professional claims advocacy isn’t just valuable, it’s often essential. Whether you’re dealing with hurricane damage, water intrusion, fire loss, or any other property claim, the right public adjuster can mean the difference between a settlement that barely covers repairs and one that fully compensates your loss.

This comprehensive guide explores everything Florida property owners need to know about public adjusters, from licensing and regulations to costs, effectiveness, and when professional representation makes financial sense. We’ll examine the latest 2026 market statistics, recent legislative reforms, and how thepublic adjusting landscapecontinues to evolve across major metropolitan areas like Miami, Tampa, Orlando, and Jacksonville.

What Is a Public Adjuster in Florida?

An insurance claims public adjuster in Florida is astate-licensed professionalwho works exclusively on behalf of policyholders during insurance claims. Unlike insurance company adjusters who represent the insurer’s interests, public adjusters advocate for property owners to secure fair and complete settlements.

Public adjusters handle every aspect of the claims process, including initial damage assessment, policy review, documentation preparation, repair cost estimation, and settlement negotiation. They’re regulated underPart VI of Chapter 626, Florida Statutes, which establishes licensing requirements, professional standards, and consumer protections.

The role differs significantly from other claims professionals. While company adjusters work to minimize payouts and attorneys typically handle litigation (often at higher costs), public adjusters focus on maximizing settlements through documentation and negotiation without necessarily resorting to lawsuits. This approach often proves faster and more cost-effective than litigation while still securing substantially higher payouts than policyholders can achieve alone.

Florida Insurance Claims Market Statistics 2026

Florida’s property insurance landscape continues to demonstrate unprecedented activity in 2026. According to theFlorida Office of Insurance Regulation’s January 2026 report, the state saw63,826 new property insurance claimsopened in a single month, with141,378 total claims pending resolutionstatewide.

The claims adjusting industry itself has grown into a significant economic force. The Third-Party Administrators and Insurance Claims Adjusters sector reached a market size of$16.0 billion in 2026, ranking as Florida’s 7th-highest revenue industry and representing5.2% of the state’s GDP.

| Metric | Value | Source Period |

|---|---|---|

| New Claims (Jan 2026) | 63,826 | January 2026 |

| Pending Claims | 141,378 | January 2026 |

| Industry Market Size | $16.0 billion | 2026 |

| Percentage of State GDP | 5.2% | 2026 |

Employment data reveals the concentration of claims professionals across Florida’s major metropolitan areas. The Tampa-St. Petersburg-Clearwater region employs7,260 claims adjusters(5.14 per 1,000 jobs), while Miami-Fort Lauderdale-West Palm Beach has6,440 adjusters(2.36 per 1,000 jobs). This concentration reflects both the high claim volumes and the competitive nature of Florida’s insurance market.

How Do Public Adjusters Increase Insurance Payouts?

The effectiveness of public adjusters isn’t just anecdotal. Historical data from Citizens Property Insurance Corporation demonstrates dramatic differences in settlement amounts. According to a comprehensive 2008-2009 study still cited as the industry benchmark, claims involving public adjusters resulted in settlements574% higher for non-catastrophe claimsand747% higher for catastrophe claimscompared to those without professional representation.

Public adjusters achieve these results through several key strategies. First, they conduct thorough damage assessments that identify all covered losses, not just the most obvious damage. Insurance company adjusters often work under time pressure and may miss secondary or hidden damage that adds thousands to the true repair cost.

Second,professional claims handlers in Floridaunderstand policy language and coverage nuances that average policyholders miss. Insurance policies contain complex provisions, exclusions, and conditions that determine what’s covered and how much insurers must pay. Public adjusters interpret these provisions in favor of policyholders rather than insurers.

Third, they prepare comprehensive documentation that insurance companies can’t easily dispute. This includes detailed scope-of-loss reports, professional repair estimates, photographic evidence, and expert opinions when needed. The quality of documentation often determines whether insurers pay policy limits or settle for the minimum.

When Should You Hire an Insurance Claims Public Adjuster in Florida?

Timing matters significantly when considering public adjuster representation. While Florida law allows policyholders to hire public adjusters at any point during the claims process, engaging professional help early typically produces better results.

Consider hiring an insurance claims public adjuster in Florida immediately after experiencing significant property damage such as hurricane destruction, major water damage, fire loss, or commercial property claims.Early engagement ensures proper documentationfrom the start and prevents common mistakes that can jeopardize claims later.

You should especially consider professional representation when your claim involves complex damage assessment, disputes over coverage interpretation, or partial denials from your insurance company. If your insurer’s settlement offer seems inadequate compared to actual repair costs, a public adjuster can review the estimate and identify shortfalls.

Large claims warrant professional help almost universally. When potential settlements exceed $50,000, the public adjuster’s fee (typically 10% to 20% of the settlement) often pays for itself many times over through increased payouts. For claims involvingroof damageorwater damage in Orlando, the complexity of damage assessment makes professional help particularly valuable.

What Are Florida’s Public Adjuster Regulations and Licensing?

Florida maintains strict regulatory oversight of public adjusters to protect consumers. The Department of Financial Services licenses all public adjusters underPart VI of Chapter 626, Florida Statutes, which establishes comprehensive requirements for licensing, professional conduct, and consumer protection.

Only licensed public adjusters can legally represent policyholders in Florida insurance claims for compensation. The licensing process requires applicants to pass a state examination, demonstrate financial responsibility, and maintain continuing education. Exemptions exist only for licensed attorneys handling claims within their legal practice, healthcare providers filing health insurance claims, and licensed health agents assisting with coverage questions.

The regulations include specific consumer protections. Public adjusters must provide written contracts clearly stating their fee structure before beginning work. They cannot accept referral fees from contractors or other parties with financial interests in the claim.Florida’s licensing requirements ensure professional standardsand provide recourse for consumers who experience misconduct.

Recent enforcement actions demonstrate regulators’ commitment to protecting policyholders. In one notable 2022 case following Hurricane Ian, authorities charged a public adjuster withallegedly defrauding homeowners of $703,000through misappropriated claim payments, highlighting the importance of verifying credentials and references.

How Much Does a Public Adjuster Cost in Florida?

Public adjusters in Florida typically charge fees ranging from10% to 20% of the final settlement amount, with specific percentages depending on claim complexity, timing, and circumstances. Florida law caps fees to protect consumers, though the exact structure varies based on whether claims involve catastrophic events.

For non-catastrophe claims, fees generally range from 10% to 15% of the settlement. For claims following declared catastrophes like hurricanes, state law may impose different fee caps, often around 10% for the first year post-disaster and potentially higher percentages as time passes.

Pricing varies based on your specific claim circumstances, including damage extent, policy complexity, and settlement amount. Larger settlements may justify lower percentage fees, while complex claims requiring extensive documentation and negotiation may warrant higher percentages.Understanding fee structures helps policyholders make informed decisionsabout whether professional representation makes financial sense.

Premium firms emphasize value over cost. While the fee percentage matters, the total net recovery matters more. A 15% fee on a $200,000 settlement nets the policyholder $170,000, far exceeding what most property owners could secure independently. The key is finding experienced professionals who deliver results that justify their compensation through superior documentation, negotiation skills, and industry knowledge.

Most reputable public adjusters work on contingency, meaning they only get paid when you receive a settlement. This aligns their interests with yours and eliminates upfront costs. However, always review contracts carefully to understand what services are included, how fees are calculated, and what happens if you’re dissatisfied with results.

How Have 2022-2026 Reforms Changed Florida Insurance Claims?

Florida’s property insurance market underwent dramatic transformation between 2022 and 2026 through comprehensive litigation and regulatory reforms. These changes fundamentally altered the claims landscape and created a more stable environment for both insurers and policyholders.

The most significant reforms targeted excessive litigation that had plagued Florida’s market for years. At its peak in 2023, Florida accounted for72% of all homeowners insurance litigation nationwidedespite representing only10% of claims. Reforms limiting attorney fees and restricting assignment of benefits dramatically reduced lawsuit filings.

The market response demonstrated the reforms’ effectiveness. According toFlorida Realtors’ 2026 market analysis, the state has seen185+ residential rate filingsproposing decreases or no increases,18 new property insurersentering the market, and Citizens Property Insurance policies falling50% since 2024. Average rate cuts of8.7%are expected as competition increases.

Claims Share:10% nationwide

Market Status:High instability

New Insurers:18 companies

Citizens Reduction:50% decline

Physical Damage:49.5% decrease

Rate Decreases:42 insurers

These reforms don’t eliminate the need for public adjusters. In fact, professional representation may become more valuable as insurers gain leverage in a less litigious environment.Understanding the difference between public and company adjustershelps policyholders navigate this evolving landscape effectively.

Regional Differences Across Florida Markets

Florida’s property insurance market varies significantly across regions, driven by hurricane exposure, property values, and local market dynamics. Understanding these regional differences helps policyholders make informed decisions about insurance claims and public adjuster representation.

South Florida, encompassing Miami-Fort Lauderdale-West Palm Beach, faces the highest hurricane risk and consequently the most complex claims environment. The region employs6,440 claims adjusters, reflecting the volume and complexity of property claims. High property values in coastal areas like Miami Beach, Coral Gables, and Boca Raton create larger claims that often benefit from professional representation.

Central Florida, particularly the Orlando metropolitan area, deals with a mix of hurricane exposure and water damage from Florida’s heavy rainfall. The region’s rapid growth and diverse property types from theme park resorts to suburban developments create varied claims scenarios.Orlando insurance claimsoften involve complex coverage questions related to vacation rentals and commercial properties.

The Tampa Bay region, with7,260 claims adjusters(the highest concentration per capita statewide), demonstrates both the claim volume and competitive market for adjuster services. The area’s vulnerability to both Gulf hurricanes and inland flooding creates consistent demand for claims expertise.Tampa’s public adjusters handle diverse property typesfrom historic bungalows in Hyde Park to modern condominiums along the waterfront.

Northeast Florida, including Jacksonville, experiences different risk profiles with more wind and rain damage than storm surge.Jacksonville policyholders hire public adjustersfor claims involving older residential properties, commercial buildings, and specialized risks like river flooding.

Key Takeaways

- Public adjusters significantly increase settlements:Historical data shows 574% to 747% higher payouts compared to unrepresented claims, with fees typically between 10% and 20% of the final settlement.

- Florida’s market remains highly active:With 63,826 new claims in January 2026 alone and 141,378 pending claims statewide, professional claims advocacy remains essential for many property owners.

- Licensing and regulation protect consumers:Florida’s Department of Financial Services regulates all public adjusters under Chapter 626, requiring licensing, examinations, and professional standards enforcement.

- Early engagement produces better results:Hiring a public adjuster immediately after significant property damage ensures proper documentation and prevents mistakes that can jeopardize claims later.

- Recent reforms have stabilized the market:Litigation reforms have reduced lawsuits, attracted new insurers, and resulted in rate decreases, but professional representation remains valuable in this evolving environment.

- Regional variations affect claims outcomes:Different areas of Florida face unique risks and market conditions, from South Florida’s hurricane exposure to Central Florida’s water damage challenges.

- Professional representation pays for itself:On larger or complex claims, the increased settlement typically exceeds the public adjuster’s fee many times over, making it a net financial benefit.

People Also Ask

Is hiring a public adjuster worth it in Florida?

Yes, particularly for larger or complex claims. Historical data shows public adjusters secure settlements 574% to 747% higher than unrepresented claims, typically making their 10-20% fee worthwhile when it results in substantially larger total payouts to policyholders.

What is the difference between a public adjuster and an insurance adjuster?

Public adjusters work exclusively for policyholders to maximize settlements, while insurance company adjusters represent the insurer’s interests to minimize payouts. This fundamental difference in who they represent creates opposite incentives and typically results in dramatically different settlement outcomes.

How much does a public adjuster charge in Florida?

Florida public adjusters typically charge between 10% and 20% of the final settlement amount, with exact percentages depending on claim complexity, timing relative to catastrophic events, and settlement size. Most work on contingency, meaning no upfront costs and payment only when you receive settlement funds.

Can I hire a public adjuster after my claim is denied?

Yes, Florida law allows policyholders to hire public adjusters at any stage of the claims process, including after partial or full denials. Many public adjusters specialize in appealing denied claims by identifying coverage that insurers overlooked or misinterpreted.

How long does it take to settle a claim with a public adjuster?

While claims with public adjusters typically take longer to settle (due to more thorough documentation and negotiation), the substantially higher payouts usually justify the additional time. Settlement timelines vary from several weeks to several months depending on claim complexity and insurer responsiveness.

Do I need a lawyer or a public adjuster for my Florida insurance claim?

Most claims benefit more from public adjusters than attorneys initially, as adjusters handle documentation and negotiation without litigation costs. Attorneys become necessary when claims require lawsuits, but starting with a public adjuster often resolves disputes without legal action while keeping costs lower.

Frequently Asked Questions

What types of claims do public adjusters handle in Florida?+

Florida public adjusters handle all types of property insurance claims including hurricane damage, wind and hail damage, water damage from leaks or flooding, fire and smoke damage, theft and vandalism, mold remediation, and business interruption claims. They work with both residential and commercial property claims of all sizes.

How do I verify a public adjuster’s license in Florida?+

You can verify any public adjuster’s license through the Florida Department of Financial Services website, which maintains a searchable database of all licensed adjusters. Always confirm licensing before signing a contract, and check for any disciplinary actions or complaints filed against the adjuster.

Can my insurance company require me not to hire a public adjuster?+

No, Florida law gives policyholders the absolute right to hire public adjusters to represent their interests. Insurance companies cannot prohibit or penalize you for obtaining professional representation, and any policy language suggesting otherwise is unenforceable.

What should I look for when choosing a public adjuster in Florida?+

Look for Florida licensure, specific experience with your type of claim, verifiable references from past clients, clear fee structures in writing, and professional associations like membership in the Florida Association of Public Insurance Adjusters. Avoid adjusters who pressure quick decisions or promise specific settlement amounts.

Will hiring a public adjuster increase my insurance rates?+

No, hiring a public adjuster does not directly affect your insurance rates. Rate increases are based on claims filed, not on whether you use professional representation. The larger settlement a public adjuster secures doesn’t increase rates beyond what the claim itself would have triggered.

Can I fire my public adjuster if I’m not satisfied?+

Yes, you can terminate your public adjuster contract at any time, though the contract will specify what fees are owed for work already completed. Review termination provisions carefully before signing, and ensure you understand your rights and obligations if the relationship doesn’t work out.

Do public adjusters work with contractors?+

Reputable public adjusters may recommend qualified contractors but should never receive referral fees or kickbacks, which Florida law prohibits. They should provide multiple contractor options and allow you to choose freely, ensuring their loyalty remains exclusively to your interests as the policyholder.