When Do I Need a Public Adjuster in Tampa? Your Complete 2026 Guide

Quick Answer

You need a public adjuster in Tampa immediately after property damage from hurricanes, floods, fires, or storms, especially when your claim is denied, undervalued, or delayed beyond reasonable timelines. Public adjusters represent your interests exclusively, inspect hidden damages common in Tampa’s Gulf Coast climate, and negotiate settlements that are typically significantly higher than initial insurance offers, all on a contingency basis.

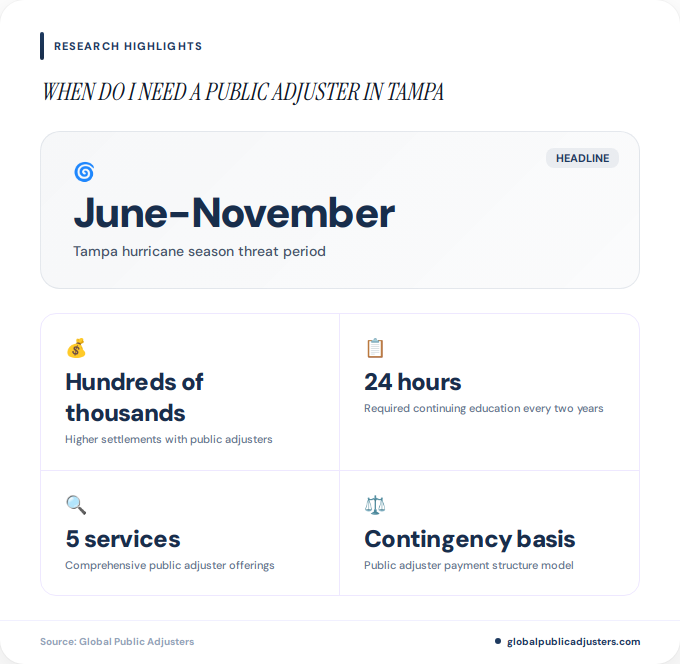

Did you know that Tampa property owners who hire public adjusters receive settlements that can behundreds of thousands of dollars higherthan initial insurance company offers? In Florida’s hurricane-prone Gulf Coast region, where property damage claims are increasingly common, knowing when to hire a public adjuster in Tampa can mean the difference between financial recovery and devastating loss.

Tampa Bay faces unique risks that make property insurance claims particularly complex. Betweenhurricane season threats from June through November, severe thunderstorms, flooding from tropical rainfall, and the constant threat of water damage in this humid coastal climate, Tampa homeowners and business owners file thousands of claims annually. Yet many discover their insurance companies undervalue damages, delay processing, or outright deny legitimate claims.

This comprehensive guide reveals exactly when you need apublic adjuster in Tampa, what warning signs indicate your claim requires professional representation, and how these licensed professionals can protect your financial interests during one of the most stressful times in property ownership.

What Is a Public Adjuster and How Do They Work in Tampa?

Apublic adjuster is a licensed insurance professional who works exclusively for you, not your insurance company. Unlike the adjuster your insurer sends to evaluate your claim, a public adjuster represents your interests throughout the entire claims process, from initial damage assessment through final settlement negotiation.

In Tampa, public adjusters must hold a valid Florida license issued by theFlorida Department of Financial Services. This licensing requires passing a comprehensive examination, submitting to background checks, posting a surety bond, completing apprenticeship requirements, and participating in24 hours of continuing education every two yearsto maintain current knowledge of insurance law and practices.

Public adjusters in Tampa provide comprehensive services that include:

- Conducting thorough property damage inspections, including hidden damages often missed by insurance company adjusters

- Interpreting complex insurance policy language to identify all covered losses and entitlements

- Documenting damages with detailed photographs, measurements, and professional estimates

- Preparing comprehensive claim submissions with supporting evidence

- Negotiating directly with insurance companies to maximize settlement amounts

- Managing all communications and paperwork throughout the claims process

The critical distinction is advocacy. While your insurance company’s adjuster works to minimize payout amounts to protect corporate profits, your public adjuster works to maximize your settlement to ensure full recovery from covered losses. This fundamental difference in motivation explains whypublic adjusters versus insurance adjustersproduce dramatically different claim outcomes for Tampa property owners.

When Should You Hire a Public Adjuster in Tampa?

The optimal time to hire a public adjuster in Tampa is immediately after property damage occurs, ideally before you even file your insurance claim. Early involvement allows your public adjuster to document damages comprehensively from the start, preventing insurance companies from disputing the extent or cause of losses later.

According toFlorida public adjuster industry standards, involving a professional adjuster before filing yields the best outcomes because they can review your policy to identify all covered perils, ensure proper documentation from day one, and establish a strong negotiating position from the initial claim submission.

However, you can hire a public adjuster at any point during the claims process, including after receiving an initial settlement offer you believe is inadequate. Many Tampa property owners successfully engage public adjusters to appeal denied claims or reopen undervalued settlements, though earlier involvement typically produces better results.

Critical Timing Scenarios in Tampa

Specific situations where immediate public adjuster involvement is essential include:

- Immediately after major weather events:Hurricane landfalls, tropical storms, severe thunderstorms with wind or hail damage

- Upon discovering significant property damage:Fire, smoke damage, water intrusion, roof leaks, structural issues

- When facing business interruption:Commercial property damage causing operational shutdown and lost revenue

- After receiving a claim denial:Insurance companies deny legitimate claims regularly, but public adjusters can often reverse these decisions

- When settlement offers seem inadequate:Initial offers frequently undervalue actual repair and replacement costs

- If claims processing stalls:Delays stretching weeks or months without reasonable explanation

Tampa’s position on Florida’s Gulf Coast makes it particularly vulnerable tohurricane damage that requires specialized claim handling. The 2024 hurricane season demonstrated how quickly damages can overwhelm property owners, with thousands of Tampa claims filed within days of major storm events.

Why Tampa’s Climate and Geography Make Public Adjusters Essential

Tampa faces unique environmental challenges that create elevated property damage risks and complex insurance claims. Understanding theseTampa-specific factorsreveals why local property owners benefit disproportionately from public adjuster representation.

Located on Florida’s west coast along Tampa Bay, the city experiences:

- Hurricane vulnerability:Direct exposure to Gulf of Mexico storm systems with 120+ mph wind potential

- Flooding risks:Low elevation areas, storm surge threats, and intense rainfall from tropical systems

- Water intrusion issues:High humidity levels promoting mold growth, roof deterioration from constant moisture exposure

- Aging infrastructure:Many Tampa neighborhoods contain older properties with roofing systems, plumbing, and electrical components prone to failure

These environmental factors createhidden damagesthat insurance company adjusters routinely overlook or undervalue. For example, after hurricane-force winds damage roofing systems, water infiltration often extends beyond visible ceiling stains to include insulation saturation, structural wood decay, and mold colonization within wall cavities. Public adjusters use thermal imaging, moisture meters, and other diagnostic tools to identify these concealed losses that significantly increase legitimate claim values.

Tampa’s Gulf Coast location creates perfect conditions for overlooked claim elements. Insurance adjusters working for companies have quotas and timelines that prevent thorough inspections. Our public adjusters spend the necessary time to uncover every element of covered damage, particularly the hidden water intrusion and mold issues endemic to this climate.

Tampa Neighborhoods with Elevated Claim Complexity

| Neighborhood/Area | Primary Risk Factors | Common Claim Issues |

|---|---|---|

| South Tampa (Bayshore, Hyde Park) | Storm surge, coastal flooding, wind exposure | Flood damage disputes, wind vs. water coverage arguments |

| Westshore/Airport Area | Commercial properties, business interruption | Lost revenue calculations, tenant improvement coverage |

| Seminole Heights | Historic homes, aging infrastructure | Matching ordinance coverage, depreciation disputes |

These geographic considerations makehiring a Tampa public claims adjusterparticularly valuable for property owners in high-risk zones who face complex coverage determinations and potential insurer pushback on legitimate claims.

What Are the Warning Signs You Need a Public Adjuster in Tampa?

Certain red flags during the claims process signal thatprofessional public adjuster representation has become essentialto protect your financial interests. Recognizing these warning signs early allows you to engage expert help before insurers entrench unfavorable positions.

Claim Denial Despite Clear Damage

Insurance companies deny Tampa claims for numerous reasons, some legitimate but many questionable. Common denial justifications include alleged policy exclusions, claims that damage predated coverage, assertions of maintenance neglect, or arguments that losses resulted from uncovered perils.

If your insurer denies a claim you believe is valid, a public adjuster can review your policy language, examine the denial reasoning, gather additional evidence, and often successfully appeal the decision. Many denials stem from incomplete documentation or misinterpretation of policy terms rather than actual coverage gaps.

Unreasonably Low Settlement Offers

Perhaps the most common warning sign is receiving a settlement offer that clearly falls short of actual repair or replacement costs. Insurance companies regularly lowball initial offers, hoping property owners will accept inadequate compensation rather than fight for proper amounts.

Signs your settlement is too low include:

- Contractor estimates significantly exceeding the insurance payout

- Failure to account for code upgrade requirements in older Tampa properties

- Excessive depreciation deductions reducing replacement cost coverage

- Omission of secondary damages like mold remediation or structural repairs

- No allowance for loss of use or additional living expenses during repairs

A Tampa public adjuster will prepare independent damage assessments with detailed cost estimates that establish the true scope of covered losses, creating leverage for renegotiation.

Processing Delays and Communication Breakdowns

Florida insurance regulations require timely claim processing, yet Tampa property owners frequently experience inexplicable delays stretching months or even years. When your insurance company stops responding to calls, fails to schedule inspections, or provides constantly changing information about claim status, these delays often reflect strategic efforts to pressure you into accepting lower settlements out of desperation.

Public adjusters eliminate these communication problems by becoming your designated representative. Insurance companies must communicate directly with your adjuster, and professionals understand how to escalate stalled claims through proper channels, including regulatory complaints when necessary.

Complex or High-Value Claims

Certain claim types inherently benefit from public adjuster expertise due to valuation complexity:

- Commercial property damage:Business equipment, inventory, tenant improvements, and business interruption calculations

- Large residential losses:Significant damage requiring extensive repairs or full reconstruction

- Multiple simultaneous perils:Combined wind, water, and fire damage requiring careful attribution

- Historic or unique properties:Specialized construction or irreplaceable features requiring expert valuation

For these scenarios, the difference between DIY claim handling and professional representation often amounts totens or hundreds of thousands of dollarsin final settlement values.

How Can a Public Adjuster Maximize Your Tampa Insurance Claim?

Public adjusters employ proven strategies and specialized knowledge to increase claim settlements far beyond what property owners achieve independently. Understanding thesevalue-creation mechanismsexplains why professional representation produces superior outcomes.

Comprehensive Damage Documentation

Insurance companies pay based on documented evidence, not verbal descriptions. Public adjusters create exhaustive damage inventories using professional photography, detailed measurements, material testing, and expert reports that establish undeniable proof of covered losses.

This documentation extends beyond obvious damages to include hidden issues Tampa’s climate creates. Moisture intrusion behind walls, compromised structural integrity from water damage, mold contamination in HVAC systems, and electrical hazards from water exposure all increase legitimate claim values when properly documented and presented.

Policy Language Expertise

Insurance policies contain dense legal language with specific definitions, coverage limits, exclusions, and conditions that determine what insurers must pay. Public adjusters spend their careers interpreting these contracts and understand nuances that maximize covered amounts.

For example, many Tampa homeowners don’t realize their policies include:

- Ordinance or law coverage:Additional amounts to bring repairs up to current building codes

- Loss of use provisions:Hotel costs and living expenses during repairs

- Debris removal allowances:Beyond standard coverage limits for extensive cleanup

- Professional fees:Engineering reports, architectural plans, and other expert costs

Identifying and claiming these additional coverages can substantially increase total settlements. For more details on how different adjuster types interpret policies, review this comparison ofpublic adjusters versus insurance agents in Florida.

Accurate Damage Valuation

Insurance company adjusters frequently undervalue damages using outdated cost databases, inappropriate depreciation schedules, or incomplete scope assessments. Tampa public adjusters prepare independent estimates using current local construction costs, including the premium pricing common in Florida’s tight contractor market, especially after major storm events when demand surges.

This valuation accuracy ensures settlements actually cover complete repairs with quality materials and reputable contractors, rather than leaving property owners with significant out-of-pocket shortfalls.

Skilled Negotiation

Even with perfect documentation and policy interpretation, final settlement amounts often depend on negotiation skills. Public adjusters negotiate claims professionally every day, understanding insurer tactics, typical settlement ranges, and leverage points that create optimal outcomes.

They know when to push for higher amounts, when to accept reasonable offers, and how to escalate disputes through proper channels including appraisal processes, Department of Financial Services complaints, or coordination with attorneys for legal action when necessary.

Reliance on insurer’s assessment

Basic photo documentation

No policy expertise

Acceptance of initial offers

Average outcome: 40-60% of full value

Independent professional assessment

Detailed forensic documentation

Expert policy interpretation

Skilled settlement negotiation

Average outcome: 80-95% of full value

What Do Public Adjusters Cost in Tampa?

Tampa public adjusters typically work on acontingency fee basis, meaning they receive payment only when you receive your insurance settlement. This no-win, no-fee structure aligns their interests with yours and makes professional representation accessible regardless of your current financial situation.

Public adjuster fees in Tampa generally range from10% to 20% of the total settlement amount, with specific percentages varying based on claim complexity, timing of engagement, and settlement size. Florida law caps public adjuster fees at specific percentages for claims related to states of emergency declared by the Governor.

Several factors influence fee structures:

- Claim size:Larger settlements often justify lower percentage fees

- Complexity level:Straightforward claims versus those requiring extensive investigation, expert reports, or litigation support

- Timing of engagement:Pre-filing involvement versus late-stage appeals or reopened claims

- Type of loss:Residential versus commercial properties, catastrophic events versus individual incidents

It’s important to understand that fee percentages apply to the settlement amount you receive, not the initial offer you would have accepted without representation. If your insurer initially offers $50,000 but a public adjuster negotiates a $150,000 settlement at a 15% fee, you receive $127,500 rather than the original $50,000. Thenet increase of $77,500 far exceeds the $22,500 fee.

For detailed breakdowns of fee structures across Florida, consult this guide topublic adjuster fees in Florida.

Pricing varies based on your specific claim circumstances, property type, and damage scope.Contact our Tampa officefor a complimentary claim review and custom fee proposal tailored to your situation.

Are Public Adjuster Fees Tax Deductible?

In many cases, public adjuster fees qualify as tax-deductible expenses when related to business property claims or investment properties. For personal residences, deductibility depends on specific circumstances and current tax law. Consult your tax professional for guidance applicable to your situation.

How Do You Choose and Hire a Public Adjuster in Tampa?

Selecting the right public adjuster significantly impacts your claim outcome. Tampa property owners should evaluate candidates using specific criteria that identify qualified, ethical professionals.

Verify Florida Licensing

Every public adjuster operating in Tampa must hold a valid Florida license. Verify licensing status through the Florida Department of Financial Services website, which provides real-time license verification, disciplinary history, and continuing education compliance.

Licensed adjusters have passed comprehensive examinations, met experience requirements, posted surety bonds protecting consumers, and maintain current knowledge through mandatory continuing education. Never hire unlicensed individuals regardless of their claims about experience or connections.

Assess Local Tampa Experience

While Florida licensing permits statewide practice, adjusters with extensive Tampa-specific experience offer advantages. They understand local construction costs, know reputable contractors and engineers for expert reports, recognize Tampa-specific damage patterns from Gulf Coast weather events, and have established relationships with local insurance company offices that facilitate negotiations.

Ask potential adjusters about their Tampa claim history, including:

- Years operating in the Tampa Bay area

- Number of Tampa claims handled

- Types of properties and damages they’ve represented locally

- Average settlement increases achieved for Tampa clients

- References from recent Tampa-area clients

Review Professional Affiliations

Membership in professional organizations like theFlorida Association of Public Insurance Adjustersdemonstrates commitment to industry standards, ongoing education, and ethical practices. These organizations provide resources, training, and accountability that benefit consumers.

Understand Contract Terms

Before signing any agreement, carefully review all terms including fee percentages, what services are included, how costs are handled, cancellation provisions, and any exclusions or limitations. Florida law grants you a10 business day right to cancelpublic adjuster contracts after signing, providing protection if you change your mind.

Reputable Tampa public adjusters provide clear, written agreements that explain all terms in plain language. Be wary of adjusters who pressure immediate signing, refuse to explain contract provisions, or make unrealistic promises about guaranteed settlement amounts.

Initial Consultation and Assessment

Most Tampa public adjusters offer free initial consultations and property inspections. Use this opportunity to assess their professionalism, knowledge, and approach. A quality adjuster will:

- Conduct a thorough property inspection, not a cursory walk-through

- Ask detailed questions about the damage event and timeline

- Review your insurance policy to identify coverage

- Provide realistic assessment of claim value and potential challenges

- Explain their process, timeline, and communication practices

- Answer all your questions clearly and completely

Trust your instincts about professionalism and communication style. You’ll work closely with this person throughout your claim, so compatibility and trust matter beyond just credentials.

What Makes Public Adjusters Different from Insurance Company Adjusters?

Understanding the fundamental differences betweenpublic adjusters and insurance company adjustersclarifies why property owners benefit from independent representation.

Employment and Loyalty

The critical distinction is employment relationship. Insurance company adjusters work for your insurer, receiving salaries or fees from the company that must pay your claim. Their job performance is evaluated based on how effectively they minimize claim payments and protect company profits.

Public adjusters work exclusively for you, earning fees only from your settlement. Their success depends on maximizing your recovery, creating perfect alignment between their financial interests and yours.

Scope of Representation

Insurance company adjusters assess damages from their employer’s perspective, looking for reasons to limit coverage, apply exclusions, or reduce valuations. They follow company guidelines that prioritize cost containment over comprehensive damage recognition.

Public adjusters investigate damages from your perspective, identifying every element of covered loss, documenting all related expenses, and interpreting policy language to maximize legitimate entitlements. They work to overcome insurance company resistance rather than create it.

Expertise and Resources

While both types of adjusters possess technical knowledge, public adjusters typically maintain broader networks of specialized experts including structural engineers, mold remediation specialists, content restoration professionals, and forensic accountants who provide evidence supporting claim values.

Insurance company adjusters have access to company resources but operate under time constraints and cost limitations that prevent thorough investigations. Tampa property owners frequently report company adjusters spending 30-45 minutes inspecting significant damages, while public adjusters conduct multi-hour forensic assessments with follow-up testing and expert consultations.

Availability and Communication

Company adjusters juggle dozens or hundreds of claims simultaneously, making direct communication difficult. Tampa property owners often struggle to reach assigned adjusters, receive returned calls, or get clear answers about claim status.

Public adjusters handling your claim provide direct access, regular updates, and responsive communication. You can contact them with questions, concerns, or new information, receiving prompt attention rather than voicemail runaround.

For more detailed analysis of these distinctions, explore this comprehensive comparison ofwhen you need a public adjuster.

What Types of Claims Benefit Most from Public Adjusters in Tampa?

While public adjusters can assist with virtually any property insurance claim, certaindamage types and scenarioscreate particularly strong cases for professional representation.

Hurricane and Wind Damage Claims

Tampa’s Gulf Coast location creates constant hurricane exposure. These catastrophic events generate the most complex and valuable property damage claims, with multiple damage types requiring careful attribution to covered perils.

Hurricane claims often involve disputes about whether damage resulted from covered wind or excluded flooding, proper valuation of roof systems and structural components, and coordination of emergency repairs with permanent restoration. Public adjusters experienced in hurricane claims understand these technical issues and documentation requirements that determine settlement outcomes.

Tampa experienced significant hurricane activity in recent years, with thousands of claims filed after major storms. Insurance companies deploy catastrophe teams with quotas and time pressures that prioritize quick settlements over accurate valuations, creating opportunity for sophisticated property owners to gain substantial advantages through public adjuster representation.

Water Damage and Flood Claims

Water damage represents one of the most common and contentious claim types in Tampa. Sources include roof leaks, plumbing failures, air conditioning condensation, storm water intrusion, and foundation seepage. Each source carries different coverage implications that insurance companies exploit to deny or minimize legitimate claims.

Public adjusters specializing in water damage understand the forensic investigation required to establish damage sources, timelines, and coverage applicability. They coordinate with water mitigation specialists, mold remediation experts, and structural engineers to document all related damages including secondary effects like mold growth and structural deterioration.

For comprehensive guidance on these claim types, review this resource aboutwater damage public adjuster services in Florida.

Roof Damage Claims

Florida’s intense sun exposure, severe weather, and salt air create harsh conditions that deteriorate roofing systems rapidly. Tampa property owners file thousands of roof damage claims annually, yet insurance companies frequently dispute whether damage resulted from covered storm events or excluded wear and tear.

Roof claims require expert analysis of damage patterns, material conditions, and causation evidence. Public adjusters work with roofing contractors and engineers to establish storm-related damage, document proper replacement costs including code upgrade requirements, and overcome insurer arguments about age-related deterioration versus acute damage events.

The difference between proper roof claim handling and inadequate representation often determines whether you receive a small repair allowance or full replacement cost for your entire roofing system. For detailed information, consult this guide toroof damage claims and public adjusters in Florida.

Fire and Smoke Damage Claims

Fire damage creates devastating losses requiring comprehensive restoration including structural repairs, content replacement, smoke odor remediation, and often complete rebuilding. These high-value claims involve complex valuations of building components, personal property, additional living expenses during reconstruction, and code upgrade requirements.

Public adjusters coordinate with fire investigators, restoration contractors, content specialists, and building professionals to document all dimensions of fire losses. They ensure proper accounting for smoke damage beyond obviously burned areas, including HVAC contamination, electrical system damage, and odor absorption in porous materials throughout affected structures.

Business Interruption Claims

Commercial property owners facing operational shutdowns from covered damage can claim lost income, continuing expenses, and extra costs to minimize loss periods. These business interruption claims require sophisticated financial analysis including revenue projections, expense categorization, and mitigation efforts documentation.

Public adjusters working with accountants and business valuation experts prepare comprehensive business interruption claims that capture all legitimate losses. Insurance companies aggressively dispute these claims using conservative projections and restrictive interpretations, making professional representation particularly valuable.

People Also Ask

Can I hire a public adjuster after my claim is denied?

Yes, you can hire a Tampa public adjuster after claim denial to appeal the decision. Public adjusters frequently reverse denials by providing additional documentation, expert reports, and policy interpretation that overcome initial rejection reasons. Many successful claims start as denials before professional intervention.

How long does the claims process take with a public adjuster in Tampa?

Tampa insurance claims with public adjuster representation typically resolve within 60 to 180 days, depending on damage complexity and insurer cooperation. Simple claims may settle in weeks, while complex disputes involving appraisal or litigation can extend longer. Public adjusters actually accelerate most claims by providing complete documentation upfront.

Will hiring a public adjuster make my insurance company angry?

Insurance companies cannot legally retaliate against policyholders for hiring public adjusters, and professional representation is your contractual right. While insurers prefer unrepresented claimants they can lowball, they must negotiate fairly with licensed public adjusters. Any retaliation constitutes bad faith and creates additional legal liability for insurers.

Do I need a lawyer or a public adjuster for my Tampa insurance claim?

Most Tampa property damage claims benefit from public adjusters who handle damage assessment and settlement negotiation without litigation. Attorneys become necessary when insurers act in bad faith, deny claims improperly, or settlement negotiations fail. Many cases succeed with public adjusters alone, though complex disputes may require both professionals working together.

What should I do immediately after property damage in Tampa?

After Tampa property damage, first ensure safety and prevent further damage through emergency repairs like tarping or water extraction. Document everything with photos and videos before cleanup. Notify your insurance company promptly but avoid detailed recorded statements before consulting a public adjuster. Contact a licensed Tampa public adjuster for free inspection and policy review before filing your formal claim.

Are public adjusters regulated in Florida?

Yes, Florida strictly regulates public adjusters through the Department of Financial Services, requiring comprehensive licensing examinations, background checks, surety bonds, apprenticeships, and 24 hours of continuing education every two years. Florida also caps fees for emergency-declared claims and grants consumers 10 business day cancellation rights. Always verify license status before hiring any public adjuster in Tampa.

Frequently Asked Questions

How much does a public adjuster cost in Tampa?+

Tampa public adjusters typically charge 10% to 20% of your final settlement on a contingency basis, with exact percentages depending on claim complexity, timing, and size. Florida law caps fees for governor-declared emergency claims. You pay nothing unless you receive a settlement, and fees come from the increased amount the adjuster negotiates beyond what you would have received independently.

When is the best time to hire a public adjuster in Tampa?+

The optimal time to hire a public adjuster in Tampa is immediately after property damage occurs, ideally before filing your insurance claim. Early involvement allows comprehensive damage documentation from the start and prevents insurance companies from establishing low initial valuations. However, you can successfully engage public adjusters at any point, including after receiving inadequate settlement offers or claim denials.

What types of property damage do Tampa public adjusters handle?+

Tampa public adjusters handle all types of property damage including hurricane and wind damage, water damage and flooding, roof damage, fire and smoke damage, mold contamination, theft and vandalism, and business interruption losses. They represent both residential and commercial property owners for any covered peril under standard insurance policies or specialized coverage.

Can a public adjuster help if my insurance claim was already settled?+

In some cases, Tampa public adjusters can reopen settled claims if you discover additional damages not included in the original settlement, if fraud or misrepresentation occurred, or if the settlement agreement contains specific provisions allowing supplemental claims. Time limits apply, so consult a public adjuster promptly if you believe your settled claim was inadequate.

How do I verify a public adjuster’s license in Tampa?+

Verify Tampa public adjuster licenses through the Florida Department of Financial Services website, which provides real-time license status, disciplinary history, continuing education compliance, and contact information. Never hire unlicensed adjusters regardless of their experience claims. Licensed professionals meet strict education, examination, bonding, and ethical requirements that protect consumers.

What is the difference between a public adjuster and an insurance adjuster?+

The fundamental difference is employment and loyalty. Insurance company adjusters work for your insurer, receiving payment from the company that must pay your claim, and their job is to minimize settlement amounts. Public adjusters work exclusively for you, earning fees from your settlement, and their success depends on maximizing your recovery. This creates opposite incentives that produce dramatically different claim outcomes.

Will my insurance rates increase if I hire a public adjuster in Tampa?+

Insurance rates may increase after any significant claim regardless of whether you use a public adjuster, based on your claim history and insurer underwriting practices. Hiring professional representation does not independently cause rate increases. The financial benefit of receiving proper settlement amounts through public adjuster representation typically far exceeds any potential premium adjustments over time.

Key Takeaways

- Hire a public adjuster in Tampa immediately after property damagefrom hurricanes, floods, fires, water intrusion, or any significant loss, especially before filing your insurance claim for optimal results.

- Warning signs requiring public adjuster help include claim denials, unreasonably low settlement offers, processing delays, and complex high-value damagescommon in Tampa’s Gulf Coast climate with hidden water and mold issues.

- Public adjusters work exclusively for you on contingency fees(typically 10-20% of settlements), creating aligned financial interests and risk-free representation that consistently produces settlements hundreds of thousands of dollars higher than initial offers.

- Tampa’s unique hurricane exposure, flooding risks, and aging infrastructurecreate property damage patterns requiring specialized knowledge that local public adjusters provide through comprehensive damage documentation, policy expertise, and skilled negotiation.

- Verify Florida licensing, assess Tampa-specific experience, and review contract terms carefullywhen selecting a public adjuster, taking advantage of free consultations and the 10-day cancellation period Florida law provides.

- Public adjusters differ fundamentally from insurance company adjustersthrough opposite employment relationships, advocacy positions, and incentive structures that make independent representation essential for protecting your financial interests.

- Hurricane damage, water intrusion, roof damage, fire losses, and business interruption claimsbenefit most from Tampa public adjuster expertise due to valuation complexity, coverage disputes, and the substantial financial stakes involved.

Protect Your Tampa Property Investment with Expert Representation

When property damage strikes your Tampa home or business, the insurance claim that follows represents one of your most important financial decisions. The difference between inadequate DIY claim handling and professional public adjuster representation often amounts totens or hundreds of thousands of dollarsin settlement value.

Tampa’s unique Gulf Coast risks create property damage scenarios where insurance companies routinely undervalue legitimate claims, deny covered losses, or delay processing to pressure inadequate settlements. Public adjusters level this playing field by providing the expertise, resources, and advocacy that protect your interests throughout the claims process.

Don’t navigate complex insurance claims alone when professional help is available on a risk-free contingency basis. Whether you face hurricane damage, water intrusion, roof deterioration, fire losses, or any other covered peril, experienced Tampa public adjusters can maximize your recovery while minimizing your stress and time investment.

Explore our comprehensive public adjuster servicesdesigned specifically for Tampa property owners, orcontact us todayfor a free claim evaluation and policy review. Our licensed professionals are ready to inspect your property, identify all covered damages, and negotiate the maximum settlement you deserve.

Similar towhen you should hire a public adjuster in Jacksonville, Tampa property owners benefit from early professional involvement that establishes strong negotiating positions from the start. The sooner you engage expert representation, the better your ultimate claim outcome.

Visitour about pageto learn more about our team’s experience, credentials, and commitment to maximizing Tampa property insurance claims through ethical, aggressive advocacy on behalf of our clients.