Water Damage Adjuster in Florida: Complete 2026 Guide to Claims, Costs, and Coverage

Quick Answer

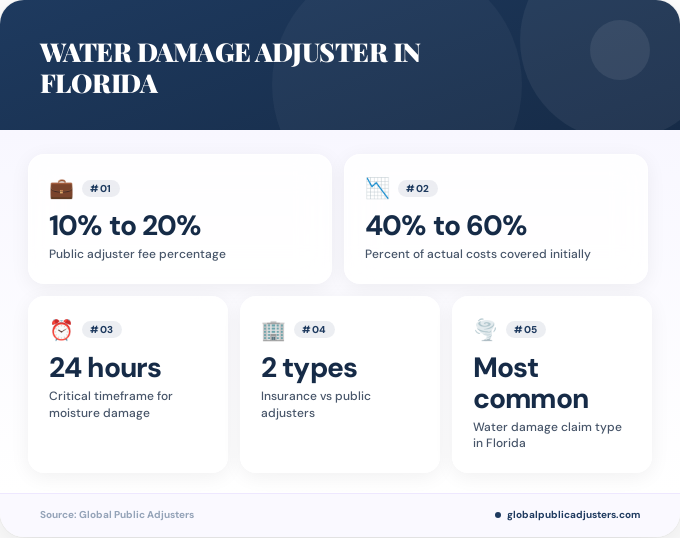

A water damage adjuster in Florida is a licensed professional who evaluates, documents, and negotiates water-loss insurance claims on behalf of policyholders. Public adjusters typically charge10% to 20%of the settlement amount and are most valuable when dealing with complex damage, disputed coverage, or undervalued claims involving hidden moisture or mold.

When a pipe bursts in your Tampa home at 3 a.m., or when Hurricane-force rain floods your Orlando property, you face two urgent crises: stopping the damage and recovering financially. The average Florida homeowner vastly underestimates hidden water damage, often accepting initial insurance settlements that cover only 40% to 60% of actual repair costs. That is where awater damage adjuster in Floridabecomes your most valuable advocate.

Florida’s unique climate, frequent severe weather, and complex property insurance market make water damage one of the most common and contentious claim types. Whether dealing with burst pipes, storm surge, roof leaks, or appliance failures, having a licensed professional on your side can mean the difference between a few thousand dollars and a full recovery that properly restores your home.

This comprehensive guide explains everything you need to know about working with a water damage adjuster in Florida in 2026, including how they work, what they cost, when to hire one, and how to choose the right professional for your specific situation.

What Is a Water Damage Adjuster in Florida?

Awater damage adjuster in Floridais a licensed insurance professional who specializes in evaluating and negotiating claims related to water losses. These adjusters fall into two distinct categories: insurance company adjusters who work for your insurer, and public adjusters who work exclusively for you, the policyholder.

Public adjusters are licensed by the Florida Department of Financial Services and must meet specific educational and ethical requirements. According tothe Public Insurance Claims Consultants of Florida, these professionals serve as your advocate throughout the claims process, ensuring that all damage is properly documented and that you receive the maximum settlement your policy allows.

The distinction is critical: while the insurance company’s adjuster represents the insurer’s financial interests, a public adjuster represents yours. This alignment of interests becomes especially important in Florida’s high-stakes insurance environment, where water damage claims are frequently undervalued or denied due to coverage disputes, causation questions, or overlooked hidden damage.

Why Should You Hire a Water Damage Adjuster in Florida?

Florida homeowners hire water damage adjusters for several compelling reasons. First,insurance companies routinely undervalue water damage claimsby missing hidden moisture intrusion behind walls, under flooring, and within HVAC systems. What appears to be surface damage often extends deep into the structural components of your home.

Second, Florida’s insurance market is notoriously complex. According to theFlorida Office of Insurance Regulation’s January 2026 stability report, the state continues to face unique challenges in property insurance, with water-related losses representing a significant portion of claims disputes.

Third, timing is everything with water damage. Moisture that sits for more than 24 to 48 hours creates ideal conditions for mold growth, which can both complicate your claim and create serious health hazards. A qualified adjuster understands these time-sensitive issues and can expedite the documentation and negotiation process.

How Does a Florida Water Damage Adjuster Work?

The water damage adjuster process in Florida typically follows a systematic approach designed to maximize your claim settlement. Here is howprofessional public adjusting firmshandle water damage cases:

Initial inspection and documentation:The adjuster performs a comprehensive site inspection within 24 to 48 hours of being retained. They use moisture meters, thermal imaging cameras, and other professional equipment to identify all affected areas, including hidden damage that is not visible to the naked eye.

Damage assessment and inventory:Every damaged item is cataloged with photographs, descriptions, and replacement cost estimates. This includes structural components (drywall, flooring, framing), personal property, and systems (electrical, HVAC, plumbing) that may have been compromised.

Claim preparation and submission:The adjuster compiles a detailed claim package that includes all documentation, professional estimates from licensed contractors, moisture readings, and a comprehensive scope of loss. This package is submitted to your insurance company with a demand letter outlining the full extent of covered damages.

Negotiation and settlement:Once the insurer responds, your adjuster negotiates on your behalf. This often involves multiple rounds of back-and-forth, supplemental inspections, and expert consultations to resolve disputes over coverage, causation, or repair costs.

According toAsk An Adjuster’s Florida guide, public adjusters typically secure settlements that are 30% to 70% higher than initial insurance company offers, particularly in complex water damage cases involving multiple rooms or structural components.

How Much Does a Water Damage Adjuster Cost in Florida?

Understanding the fee structure is essential when hiring a water damage adjuster in Florida.Most public adjusters work on a contingency fee basis, meaning they only get paid when you receive a settlement. This aligns their interests with yours and removes upfront financial barriers for homeowners facing significant losses.

In 2026, typical public adjuster fees in Florida range from10% to 20%of the final settlement amount. The percentage often depends on several factors:

- Claim complexity:Simple water damage from a single source may command lower fees, while multi-system failures or storm-related intrusion with mold issues typically warrant higher percentages.

- Claim size:Larger settlements often involve lower percentage fees, while smaller claims may require higher percentages to justify the adjuster’s time investment.

- Timing:Some adjusters charge different rates for claims initiated immediately after loss versus reopening previously settled or denied claims.

- Geographic location:Fees may vary between metropolitan areas like Miami, Jacksonville, Tampa, and Orlando versus more rural Florida communities.

For detailed information on public adjuster costs in Florida, see ourcomplete 2026 fee guide for Jacksonville homeowners, which covers the factors that influence pricing across the state.

| Claim Type | Typical Fee Range | Common Scenarios |

|---|---|---|

| Simple water damage | 10% to 15% | Single-room damage, clear causation, no mold |

| Complex water damage | 15% to 20% | Multiple rooms, hidden damage, mold involvement |

| Reopened or denied claims | 20%+ | Previous settlement challenges, litigation potential |

Important warning:Be cautious of any adjuster demanding fees above Florida’s legal limits or requiring upfront payment before services are rendered. These are red flags that may indicate unlicensed or unethical operators.

When Should You Contact a Water Damage Adjuster?

Timing is critical in Florida water damage cases. Industry best practices recommend contacting awater damage adjuster within 24 to 48 hoursof discovering the loss. This rapid response serves multiple purposes:

Prevents additional damage:Quick documentation helps establish the initial scope of loss before secondary damage (like mold) complicates causation questions. Insurance companies often dispute whether damage resulted from the covered event or from delayed mitigation.

Preserves evidence:Water evaporates, materials dry out, and visible signs of intrusion disappear. Professional documentation with moisture meters and thermal imaging captures evidence that will be crucial during negotiations.

Accelerates emergency mitigation:While you should begin emergency water extraction and drying immediately (your policy requires it), having an adjuster document conditions before mitigation protects your claim. Many homeowners start cleanup too quickly and inadvertently destroy evidence of the full damage extent.

You should also consider hiring a public adjuster when:

- The insurance company’s initial settlement offer seems too low

- Your claim has been denied or partially denied

- The damage involves multiple systems or structural components

- Mold is present or suspected

- You lack time or expertise to manage the claims process

- The insurer is delaying or avoiding communication

If you are dealing with a denied claim, our guide onhow to appeal an insurance claim denial in Orlandoprovides detailed strategies that apply throughout Florida.

What Types of Water Damage Are Covered in Florida?

Understanding what your Florida homeowners insurance policy covers is essential before filing a claim. Not all water damage is treated equally, and the source of the water often determines whether you have coverage.

Typically covered water damage:

- Sudden and accidental pipe bursts

- Appliance malfunctions (washing machines, water heaters, dishwashers)

- HVAC system failures and condensation issues

- Roof leaks from storm damage (when the storm is a covered peril)

- Accidental overflow from plumbing fixtures

- Ice dam damage (rare in Florida but can occur in extreme weather)

Typically excluded water damage:

- Flooding from external sources (requires separate flood insurance)

- Groundwater seepage or rising water tables

- Maintenance-related issues or gradual leaks

- Backup of sewers or drains (unless you have optional coverage)

- Storm surge and tidal flooding

According to theFlorida Hurricane Catastrophe Fund 2026 contract language, Florida policies specifically exclude losses from “water damage, flood, surface water, waves, tidal water, overflow, storm surge, or spray” unless explicitly covered by endorsement or separate policy.

This is where a knowledgeable water damage adjuster becomes invaluable. They understand the nuances of coverage language and can often find pathways to coverage that the average policyholder would miss. For example, while flood damage from storm surge is excluded, wind-driven rain entering through a storm-damaged roof may be covered.

What Makes Florida Water Damage Claims Different?

Florida’s unique geography, climate, and insurance market create specific challenges for water damage claims that do not exist in most other states.

Hurricane and tropical storm exposure:Florida experiences more hurricane and tropical storm impacts than any other state. When these systems bring both wind and rain, determining causation becomes critical. Was the water intrusion caused by wind-driven rain through a storm-damaged opening (potentially covered) or by flooding (typically excluded)?

High humidity and rapid mold growth:Florida’s year-round humidity means that water damage leads to mold growth much faster than in drier climates. Mold can begin developing within 24 to 48 hours, and coverage for mold remediation is often limited or excluded unless it directly results from a covered loss.

Assignment of benefits disputes:Florida has unique laws regarding assignment of benefits (AOB), where policyholders assign their insurance benefits to contractors. While recent reforms have limited AOB abuses, the practice has created a contentious environment where insurers are often suspicious of claims involving third-party contractors.

Property insurance crisis:Florida’s property insurance market has experienced significant instability, with multiple carrier insolvencies and policy non-renewals. This has pushed many homeowners to Citizens Property Insurance Corporation, the state-backed insurer of last resort, which has different claims handling procedures than private carriers.

Understanding these Florida-specific issues is why working with a local water damage adjuster who specializes in the state’s unique insurance environment is so important. National adjusters or out-of-state professionals often lack the specific knowledge needed to navigate Florida’s complex regulatory and coverage landscape.

Public Adjuster vs. Insurance Company Adjuster: Understanding the Difference

One of the most common sources of confusion in water damage claims is understanding the difference between the adjuster your insurance company sends and a public adjuster you hire independently.

| Factor | Insurance Company Adjuster | Public Adjuster |

|---|---|---|

| Who they work for | The insurance company | You, the policyholder |

| Financial incentive | Minimize claim payouts | Maximize your settlement |

| Cost to you | None (paid by insurer) | 10% to 20% of settlement |

| Inspection approach | Focus on visible damage | Search for all damage, including hidden |

The insurance company adjuster is not your enemy, but their job is to protect the insurer’s interests. They are evaluated and compensated based on how efficiently they close claims and how well they control costs. A public adjuster, by contrast, earns more when you receive a larger settlement, creating a direct alignment of financial interests.

According toLouis Law Group’s 2026 analysis of Florida property claims, policyholders represented by public adjusters receive significantly higher settlements on average, particularly in complex water damage cases involving structural issues or mold.

Important limitation:Public adjusters cannot provide legal advice, file lawsuits, or handle bad-faith litigation. If your dispute escalates to requiring legal action, you will need to consult with an attorney who specializes in insurance law. Many public adjusters work closely with property insurance attorneys and can provide appropriate referrals when legal intervention becomes necessary.

What Are Warning Signs When Choosing an Adjuster?

Not all water damage adjusters in Florida are equally qualified or ethical. Watch for these warning signs that should prompt you to look elsewhere:

Unlicensed operators:Always verify that your adjuster holds a current Florida public adjuster license through the Department of Financial Services. Unlicensed adjusters cannot legally represent you and may expose you to legal and financial risks.

Excessive or unusual fees:Be wary of adjusters demanding fees above 20% for standard claims, requiring large upfront payments, or asking for fees regardless of outcome. Legitimate public adjusters work on contingency and charge within industry-standard ranges.

Pressure tactics:Reputable adjusters do not use high-pressure sales tactics, show up uninvited after disasters, or demand you sign contracts immediately. You should have time to review contracts, check references, and make informed decisions.

Promises of specific outcomes:No adjuster can guarantee a specific settlement amount. Anyone who promises exact dollar figures before reviewing your policy and inspecting the damage is either dishonest or inexperienced.

Lack of local presence:Storm chasers who travel from other states after disasters often lack knowledge of Florida-specific insurance regulations, policy forms, and claims practices. Choose adjusters with established Florida offices and long-term local presence.

For more information on properly documenting and filing your claim, review ourcomplete step-by-step guide to filing property damage claims in Orlando, which covers best practices throughout the state.

Key Takeaways

- Water damage adjusters in Floridaspecialize in evaluating and negotiating water-loss claims, with public adjusters working exclusively for policyholders and insurance company adjusters representing insurers.

- Public adjusters typically charge10% to 20%of the final settlement on a contingency basis, meaning you pay nothing unless you receive a settlement.

- Contact a water damage adjuster within24 to 48 hoursof discovering damage to document conditions before secondary issues like mold complicate your claim.

- Florida’s unique climate, hurricane exposure, and insurance market create specific challenges that require specialized local knowledge and expertise.

- Public adjusters typically secure settlements30% to 70% higherthan initial insurance offers, particularly in complex cases involving hidden damage or mold.

- Always verify that your adjuster holds a current Florida public adjuster license and avoid anyone using high-pressure tactics or making specific settlement guarantees.

- Coverage for water damage depends heavily on the source of the water, with sudden and accidental losses generally covered while flooding typically requires separate flood insurance.

People Also Ask

Do I need a public adjuster for water damage in Florida?

You should consider a public adjuster when the loss is large, involves hidden damage, includes mold, spans multiple rooms, or when the insurance company’s initial offer seems inadequate. Public adjusters are especially valuable in Florida’s complex insurance environment where water damage claims are frequently undervalued.

Can a public adjuster negotiate with my insurance company?

Yes, public adjusters are licensed professionals authorized to negotiate insurance claims on your behalf. They handle all communication with your insurer, present evidence of your losses, and work to secure the maximum settlement your policy allows. However, they cannot file lawsuits or provide legal advice.

How long does a water damage claim take in Florida?

Simple water damage claims may settle within 30 to 60 days, while complex claims involving structural damage, mold, or coverage disputes can take three to six months or longer. Florida law requires insurers to acknowledge claims within 14 days and make settlement decisions within 90 days in most cases.

What is the difference between flood damage and water damage in Florida?

Standard homeowners policies cover sudden and accidental water damage from internal sources like burst pipes or appliance failures. Flood damage from external sources like storm surge, rising water, or groundwater seepage requires separate flood insurance through the National Flood Insurance Program or private carriers.

Will hiring a public adjuster delay my water damage claim?

No, experienced public adjusters typically accelerate the claims process by submitting complete, well-documented packages that reduce back-and-forth with insurers. While comprehensive documentation takes time upfront, it usually results in faster final settlements and fewer disputes than incomplete self-filed claims.

Are public adjuster fees tax deductible in Florida?

Public adjuster fees may be tax deductible as a casualty loss expense in some circumstances, but tax laws change frequently and vary by situation. Consult with a qualified tax professional who understands Florida property loss deductions to determine what applies to your specific case.

Frequently Asked Questions

What should I do immediately after discovering water damage?+

First, stop the water source if possible and safe to do so. Then contact your insurance company to report the claim, document the damage with photos and videos, and begin emergency mitigation to prevent additional damage. Contact a public adjuster within 24 to 48 hours to ensure proper documentation before conditions change.

Can I switch to a public adjuster after starting a claim myself?+

Yes, you can hire a public adjuster at any point during the claims process, even if you have already filed the claim yourself. Many homeowners hire public adjusters after receiving unsatisfactory initial settlement offers. However, earlier involvement typically produces better results because evidence and conditions are better preserved.

Does my insurance company have to accept my public adjuster’s estimate?+

No, the insurance company is not required to accept your public adjuster’s estimate. The final settlement is reached through negotiation between your adjuster and the insurer’s adjuster, often involving independent inspections, contractor bids, and expert opinions. The goal is to reach agreement on what the policy covers and the cost to repair.

What if my water damage claim is denied?+

If your claim is denied, you have the right to appeal the decision. A public adjuster can help build a stronger case with additional documentation and expert opinions. If the denial appears to be in bad faith or based on incorrect policy interpretation, you may need to consult with an insurance attorney who can pursue legal remedies.

How do I verify a public adjuster’s license in Florida?+

You can verify any Florida public adjuster’s license through the Department of Financial Services online license search tool. This will show their license status, any disciplinary actions, and when their license was issued. Always verify licensing before signing a contract or allowing anyone to represent you in an insurance claim.

Can a public adjuster help with mold damage from water intrusion?+

Yes, public adjusters commonly handle claims that include mold damage resulting from covered water losses. They can document the connection between the water intrusion and subsequent mold growth, coordinate mold testing and remediation estimates, and negotiate for mold coverage within your policy limits. Many Florida policies have specific sublimits for mold remediation.

Should I accept my insurance company’s recommended contractors?+

Related:Water Damage Claims Adjuster in Orlando: Your Complete 2026 Guide to Expert Claim Representation

Related:How Do Public Adjusters Get Paid in Florida: Complete 2026 Fee Structure Guide

Related:How Does a Public Adjuster Get Paid in Florida: Complete 2026 Fee Structure Guide

You have the right to choose your own contractors for repairs and are not required to use the insurer’s preferred vendors. Many policyholders prefer independent contractors who work for them rather than having ongoing relationships with insurance companies. Your public adjuster can help coordinate contractor estimates and ensure repairs are properly documented and completed.