How Much Does a Public Adjuster Cost in Jacksonville? Complete 2026 Fee Guide

Quick Answer

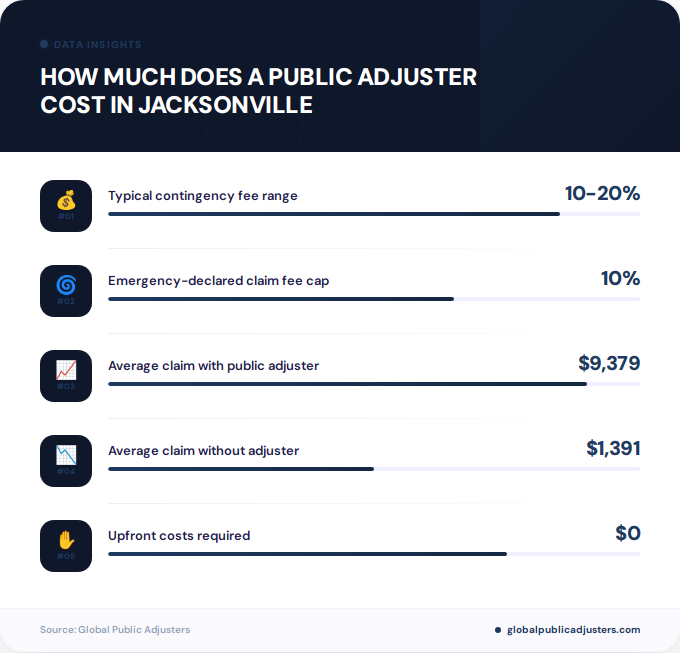

Public adjusters in Jacksonville typically charge a contingency fee of10% to 20% of your final claim settlement, with no upfront costs. For emergency-declared claims like hurricanes, Florida law caps fees at10% for the first yearafter the declaration, then 20% thereafter, meaning your actual cost depends heavily on your settlement amount and claim timing.

If you’re facing property damage from Jacksonville’s notorious hurricane seasons, flooding near the St. Johns River, or storm damage in neighborhoods like Riverside or San Marco, you might be wondering whether hiring a public adjuster is worth the investment. The cost question often stops homeowners in their tracks: will a public adjuster’s fee eat up the extra settlement they promise to secure?

Here’s a surprising fact that puts the investment in perspective: according toindustry data from the Florida Association of Public Insurance Adjusters, policyholders who used public adjusters received$9,379 per claim versus $1,391 without onein non-catastrophe claims, and an even more dramatic$17,187 versus $2,029in catastrophic claims. Understandinghow much a public adjuster costs in Jacksonvillemeans weighing these potential settlement increases against the percentage-based fees that Florida law carefully regulates.

In this comprehensive guide, we’ll break down every aspect of public adjuster pricing in Jacksonville, from standard contingency rates to state-mandated fee caps, helping you make an informed decision about your insurance claim representation.

What Is the Standard Fee Structure for Public Adjusters in Jacksonville?

Unlike attorneys who bill hourly or contractors who quote project prices,public adjusters in Jacksonville operate almost exclusively on a contingency fee basis. This means you pay nothing upfront and only owe fees if and when your insurance claim results in a payment.

The typical contingency percentage in Jacksonville ranges from10% to 20% of your final settlement amount. ManyJacksonville public adjusting firmsadvertise “no fee unless you get paid,” reflecting this performance-based model that aligns the adjuster’s financial interest with maximizing your claim outcome.

This contingency structure offers several advantages for policyholders facing unexpected property damage. You don’t need to come up with cash for professional representation when you’re already dealing with repair expenses and displacement costs. The model also incentivizes adjusters to fight for the highest possible settlement, since their compensation directly correlates with your claim amount.

Why the 10-Point Percentage Spread?

You might wonder why there’s such a wide range between 10% and 20%. Several factors influence where a particular adjuster’s rate falls within this spectrum. Smaller, straightforward claims with clear documentation often command fees at the lower end. Complex commercial claims, disputes requiring extensive documentation and negotiation, or cases involving policy interpretation challenges typically justify higher percentages.

The timing of when you hire an adjuster also matters. If you bring in representation early in the claims process versus after an initial denial or lowball offer, the scope of work differs significantly. Some Jacksonville firms offer tiered pricing based on claim complexity and stage of engagement.

How Do Florida’s Fee Limits Affect Jacksonville Costs?

Florida imposes specific statutory limits on public adjuster fees that directly impact what you’ll pay in Jacksonville. These regulations, enforced by theFlorida Department of Financial Services, exist to protect consumers during vulnerable times, particularly after natural disasters.

The most significant fee restriction applies toclaims tied to a Governor-declared state of emergency, common in Jacksonville given Florida’s hurricane exposure. When the Governor declares a state of emergency, public adjuster fees are capped at10% of the claim payment for the first yearfollowing the declaration. After that one-year period expires, fees can increase to the standard20% maximum.

This emergency-related fee cap recognizes that major disasters like Hurricane Irma or tropical storms affecting Jacksonville create widespread claims where homeowners need protection from potentially predatory pricing. The 10% first-year cap ensures affordable access to professional representation during crisis periods.

Additional Florida Contract Requirements

Beyond percentage limits, Florida law mandates several contract provisions that affect your total cost. Public adjusterscannot charge fees on claim payments already receivedbefore you signed their contract. If your insurer issued a partial payment before you hired representation, the adjuster’s fee applies only to additional amounts recovered.

The law also prohibits charging for services not actually performed. Your contract must clearly specify what work the adjuster will complete. Florida grants consumers acancellation right within 10 business daysof contract execution, or for emergency-related claims,30 days after the loss date or 10 days after signing, whichever is longer.

These consumer protections mean that reputable Jacksonville public adjusters operate within a well-defined regulatory framework. Any firm pushing contract terms that exceed these limits should raise immediate red flags. If you’re navigating the claims process independently first, ourguide to filing an insurance claim in Jacksonvilleprovides essential starting information.

| Claim Type | Maximum Fee | Timeline |

|---|---|---|

| Emergency-declared (within 1 year) | 10% | First year after declaration |

| Emergency-declared (after 1 year) | 20% | After one-year period expires |

| Non-emergency claims | 10-20% | Standard negotiated rate |

What Determines Your Final Public Adjuster Cost?

While the percentage range provides a general framework, your specific cost depends on multiple variables unique to your Jacksonville property claim. Understanding these factors helps you anticipate what you’ll actually pay and assess whether different adjusters’ quotes represent fair value.

Claim complexityranks as the primary cost driver. A straightforward roof damage claim with clear wind damage documentation requires less investigative work than a mold claim requiring expert testing, historical moisture analysis, and policy coverage interpretation. Commercial property claims involving business interruption losses or complex inventory assessments typically justify higher fees than residential claims.

Thesettlement amountobviously determines your dollar cost in a percentage-based model. A 15% fee on a $30,000 settlement equals $4,500, while the same percentage on a $200,000 settlement costs $30,000. This reality underscores why understanding the potential settlement increase matters when evaluating whether to hire representation.

Jacksonville-Specific Considerations

Certain Jacksonville-area factors can influence both your claim outcome and adjuster costs. Properties in flood-prone areas near the St. Johns River or Atlantic Beach often involve both homeowners and flood insurance policies, requiring coordination across multiple carriers and potentially more complex fee arrangements.

Hurricane-related claims in Jacksonville typically fall under emergency declaration fee caps, but the timing matters. If you experienced damage months after a hurricane when the emergency declaration period expired, standard 10-20% rates apply. Jacksonville’s coastal location means wind versus water damage disputes frequently arise, sometimes requiring engineering assessments that extend the adjuster’s workload.

Historical properties in neighborhoods like Avondale or Springfield may involve additional documentation requirements or historic preservation considerations that impact the claims process complexity. Similarly, claims for high-value properties in Ponte Vedra Beach or Nocatee communities often involve higher settlement amounts that, while subject to the same percentage, result in larger absolute fee dollars.

Real-World Cost Examples in Jacksonville Claims

Examining concrete cost scenarios helps you understand what you might actually pay for public adjuster services in Jacksonville. These examples reflect the typical percentage ranges applied to various settlement amounts, though your specific cost depends on the factors we’ve discussed.

For amoderate residential claimsettling at $50,000 after hurricane wind damage to your Jacksonville home’s roof and interior, a 10% fee (common under emergency declaration caps) would cost$5,000. At the standard non-emergency rate of 15%, the same settlement would cost$7,500.

Consider asubstantial property damage claimwhere your Mandarin home suffered extensive flooding and structural damage, ultimately settling for $150,000. At the emergency-capped 10% rate, you’d pay$15,000. At a negotiated 15% rate for a complex claim, the fee reaches$22,500. At the maximum 20% rate that might apply to particularly challenging disputes or after emergency periods expire, you’d pay$30,000.

Formajor commercial or high-value residential claimssettling at $250,000 or more, the fee calculations scale proportionally. At 10%, your cost is$25,000. At 15%, it’s$37,500. At the maximum 20%, you’re paying$50,000 or moredepending on the final settlement amount.

According toFlorida insurance law experts, “Public adjusters typically charge contingency fees ranging from 10 to 20 percent of the claim settlement, with emergency-declared claims subject to the 10% first-year cap. Any contract demanding fees exceeding these legal limits represents a major red flag that consumers should immediately address with the Florida Department of Financial Services.”

Comparing Costs to Potential Settlement Increases

The critical question isn’t just what you’ll pay in fees, but whether the adjuster’s representation results in a net benefit after costs. The industry data showing public adjuster clients receiving settlements 4-8 times higher than those who self-represent suggests that in many cases, even after paying the contingency fee, you still come out significantly ahead.

If an insurance company initially offers you $40,000 for storm damage, but a public adjuster secures a $100,000 settlement, you net $90,000 after a 10% fee or $80,000 after a 20% fee. Either outcome substantially exceeds the original $40,000 offer. This math explains why many Jacksonville homeowners view the contingency fee as a worthwhile investment rather than a pure cost.

However, for smaller claims or situations where the initial insurance offer seems reasonable and well-documented, the percentage fee might consume a significant portion of any incremental increase. Running the numbers for your specific situation helps determine whether professional representation makes financial sense. For complex claim denials, our article onappealing insurance claim denialsoffers complementary strategies.

When Is Hiring a Public Adjuster Worth the Cost?

Not every insurance claim requires professional representation, but certain situations strongly justify the cost of hiring a public adjuster in Jacksonville. Recognizing these scenarios helps you make strategic decisions about when to invest in expert advocacy.

Large or complex claimsrepresent the clearest case for representation. If your Jacksonville property suffered damage exceeding $50,000, the potential settlement increase typically outweighs the percentage fee. Claims involving structural damage, multiple systems, or extensive repairs require detailed estimates and documentation that public adjusters specialize in preparing.

When facingclaim denials or disputeswith your insurance carrier, professional representation becomes particularly valuable. Insurance companies employ their own adjusters working to minimize payouts. Having a licensed public adjuster who understands policy language and claims regulations levels the playing field. Fire damage claims especially benefit from expert representation, as detailed in ourfire claims adjuster guide for Jacksonville.

Claim Types That Benefit Most from Professional Representation

Certain damage types inherently involve complexity that justifies adjuster costs.Water damage claimsoften require distinguishing covered perils from excluded flood damage, identifying hidden moisture, and documenting secondary damage like mold. Jacksonville’s humidity and flood exposure make these disputes common.

Hurricane and wind damage claimsfrequently involve large settlement amounts and technical questions about damage causation. Did your roof fail due to covered wind damage or excluded wear and tear? Public adjusters bring meteorological data, engineering expertise, and detailed damage assessments that strengthen your position.

Business interruption claimsinvolve calculating lost income, projecting recovery timelines, and documenting financial impacts. These complex commercial claims almost always justify professional representation given the substantial sums at stake and specialized knowledge required.

Conversely, small claims under $10,000 with clear documentation and reasonable insurance company responses may not warrant the percentage fee. If your carrier promptly accepts liability and offers a settlement that covers your documented repair costs, handling the claim yourself makes financial sense.

How to Choose a Public Adjuster in Jacksonville

Once you’ve decided to hire representation, selecting the right public adjuster requires evaluating factors beyond just their quoted fee percentage. Jacksonville has numerous firms offering public adjusting services, and the cheapest option rarely provides the best value.

Verify licensing and credentialsfirst. Florida requires public adjusters to hold an active license issued by the Department of Financial Services. You can verify any adjuster’s license status through the state’s online database. Look for adjusters with professional designations and continuing education commitments demonstrating ongoing expertise.

Evaluateexperience with your specific claim type. An adjuster who primarily handles residential wind damage might not be your best choice for a complex commercial property business interruption claim. Ask about recent cases similar to yours and request references from Jacksonville clients with comparable situations.

Understanding Contract Terms and Fee Structures

Before signing, carefully review thecontingency fee percentageand what it applies to. Ensure the contract specifies that fees only apply to new money recovered, not payments already received. Confirm whether the percentage applies to the entire settlement including contractor estimates, or only to the insurance payment amounts.

Clarify what services are included in the fee. Does it cover all aspects of your claim, or might additional charges apply for expert consultations, engineering reports, or legal coordination? ReputableJacksonville public adjustersinclude comprehensive services in their contingency fee with no surprise add-ons.

Ask about theirtrack record and average settlement increases. While past results don’t guarantee future outcomes, adjusters who consistently secure settlements significantly exceeding initial offers demonstrate valuable negotiation skills. Request specifics: What percentage of claims do they take to completion? What’s their average claim duration?

Review thecancellation and termination provisionscarefully. Florida law grants you specific cancellation rights, but understanding the process and any potential pro-rated fees if you terminate the relationship matters. Ensure you’re comfortable with the commitment before signing.

Hidden Costs and Contract Red Flags to Avoid

While legitimate public adjusters in Jacksonville operate transparently within Florida’s regulatory framework, awareness of potential hidden costs and contract red flags protects you from problematic arrangements.

Upfront fees or advance paymentsshould immediately raise concerns. Florida law permits public adjusters to charge advance fees for non-residential claims only, and only when approved by the Department of Financial Services. Any residential claim adjuster demanding money before settlement likely violates state regulations.

Watch forvague or unlimited fee structures. Your contract should clearly state the exact percentage and specify how it’s calculated. Phrases like “reasonable fees” or “customary charges” without specific percentages create opportunities for disputes. Theinvestment analysis of public adjuster costsemphasizes the importance of transparent fee agreements.

Fee Stacking and Referral Arrangements

Some problematic arrangements involvecontractors and public adjusters working togetherwhere the contractor refers you to an adjuster, then both take percentages of your settlement. While not inherently illegal, these relationships can inflate costs and create conflicts of interest. Your adjuster should work solely for you, not coordinate with contractors to maximize their combined fees.

Beware offees charged on amounts you negotiate directly. If you reach agreement with your insurance company on part of your claim without the adjuster’s involvement, you shouldn’t owe fees on those amounts. Your contract should clarify that fees apply only to settlements the adjuster actually assists in securing.

Unusual contract termslike extended exclusive representation periods, automatic renewals, or provisions transferring your rights to negotiate with the insurer should trigger careful review. Standard contracts grant the adjuster authority to negotiate on your behalf but preserve your ultimate control over settlement decisions.

If you’re considering becoming a public adjuster yourself, understanding these fee structures and regulations from the professional side proves essential. Our comprehensive guide onFlorida public adjuster licensingcovers the requirements in detail.

People Also Ask

Do I pay a public adjuster upfront in Jacksonville?

No, legitimate public adjusters in Jacksonville work on contingency, meaning you pay nothing upfront for residential claims. They collect their percentage fee only after your insurance claim settles and you receive payment. Any adjuster demanding advance payment for residential property claims likely violates Florida regulations.

Can public adjusters charge more than 10% in Florida?

Yes, but it depends on timing. For Governor-declared emergencies like hurricanes, fees are capped at 10% for the first year after the declaration, then can increase to 20% thereafter. For non-emergency claims, public adjusters typically charge between 10% and 20% based on claim complexity and scope of work.

What happens if my claim is denied after hiring a public adjuster?

With contingency-based fees, if your claim results in zero payment, you owe nothing to the public adjuster. They only collect fees when you receive settlement money. This performance-based structure means the adjuster’s financial interest aligns completely with maximizing your claim recovery.

Are public adjuster fees tax deductible in Florida?

Generally, fees paid to public adjusters for personal residential property claims are not tax deductible under current IRS rules. However, business property claims and commercial property adjusting fees may qualify as business expenses. Consult a tax professional for your specific situation.

Can I negotiate a public adjuster’s fee percentage?

Yes, public adjuster fees are negotiable within Florida’s legal limits. While most Jacksonville firms have standard rates, factors like claim size, complexity, and whether you’re bringing them in early versus after a denial may influence the percentage. Always discuss fees before signing a contract and ensure the rate reflects your situation fairly.

How long does a public adjuster contract last in Jacksonville?

Public adjuster contracts typically remain in effect until your claim reaches final settlement or the contract is properly terminated. Florida law provides specific cancellation rights: 10 business days after signing for standard contracts, or 30 days after the loss (or 10 days after signing, whichever is longer) for emergency-related claims. Always review termination provisions before signing.

Frequently Asked Questions

What is the average public adjuster fee in Jacksonville for hurricane claims?+

Hurricane claims filed within one year of a Governor-declared state of emergency are subject to Florida’s 10% fee cap, which represents the standard cost for Jacksonville hurricane claims during that period. After the one-year emergency period expires, fees can increase to the typical 10-20% range, though 15% represents a common middle-ground rate for complex storm claims.

Do public adjusters charge differently for residential versus commercial claims?+

While both residential and commercial claims typically use the 10-20% contingency model, commercial claims often fall at the higher end of this range due to increased complexity, business interruption calculations, and higher settlement amounts. Commercial claims also allow advance fees in certain circumstances under Florida law, unlike residential claims which must be purely contingency-based.

Will I save money by not hiring a public adjuster in Jacksonville?+

Not necessarily. While you avoid paying the adjuster fee, research shows public adjuster clients receive settlements 4-8 times higher than self-represented claimants. For a $100,000 settlement with a 10% fee, you net $90,000, far exceeding the typical $20,000-$30,000 self-negotiated settlements. The key is whether the settlement increase exceeds the percentage fee for your specific claim.

When do I actually pay the public adjuster’s fee?+

You pay the public adjuster after your insurance company issues the claim settlement payment. Most adjusters request their fee once you receive and deposit the insurance check. The payment is calculated as the contracted percentage of your final settlement amount, and reputable adjusters provide a clear invoice showing how the fee was calculated.

Can I hire a public adjuster after my insurance company already made an offer?+

Yes, you can hire a public adjuster at any stage of the claims process, even after receiving an initial offer. However, Florida law prevents adjusters from charging fees on payments already received before you signed their contract. The adjuster’s fee applies only to additional amounts they help recover above what was already paid.

What should be included in a public adjuster contract in Jacksonville?+

A proper Florida public adjuster contract must include the exact fee percentage, scope of services, your cancellation rights, language stating fees apply only to new recoveries, and clear termination provisions. It should specify what’s included in the fee versus any additional charges, though most legitimate adjusters include all standard claim services in their contingency percentage with no hidden costs.

Are there situations where public adjuster fees might be refunded?+

If you exercise your legal right to cancel the contract within Florida’s specified timeframe (10 business days for standard contracts, or up to 30 days for emergency-related claims), any fees paid would be refunded. Additionally, if an adjuster charged fees for services not performed or for payments received before contract execution in violation of Florida law, those fees should be refunded and the violation reported to the Department of Financial Services.

Making an Informed Decision About Public Adjuster Costs

Understandinghow much a public adjuster costs in Jacksonvillerequires looking beyond simple percentage numbers to evaluate the complete value proposition. With contingency fees typically ranging from 10% to 20%, and Florida’s emergency fee caps providing consumer protection during disasters, the cost structure is transparent and regulated.

The real question isn’t whether you’ll pay a percentage fee, but whether that fee represents a worthwhile investment given your claim’s potential settlement increase. For large, complex, or disputed claims in Jacksonville, professional representation often delivers net benefits that substantially exceed costs. Smaller straightforward claims with reasonable insurance responses may not justify the percentage fee.

Key factors in your decision include your claim’s size and complexity, your comfort level negotiating with insurance adjusters, the insurance company’s initial response, and whether your situation involves emergency-declared events triggering Florida’s fee caps. For property owners in Jacksonville facing significant damage from hurricanes, flooding, fire, or other covered perils, a public adjuster’s expertise in documentation, policy interpretation, and negotiation frequently proves invaluable.

Need Help with Your Jacksonville Insurance Claim?

At Global Public Adjusters, we provide transparent contingency-based representation that maximizes your insurance settlement while complying with all Florida fee regulations. Our Jacksonville team offers free claim reviews to help you understand your options with no obligation.

Related:Water Damage Adjuster in Florida: Complete 2026 Guide to Claims, Costs, and Coverage

Related:Water Damage Claims Adjuster in Orlando: Your Complete 2026 Guide to Expert Claim Representation

Related:How Do Public Adjusters Get Paid in Florida: Complete 2026 Fee Structure Guide

Key Takeaways

- Public adjusters in Jacksonville charge 10-20% contingency feeswith no upfront costs, meaning you pay only if your claim settles successfully

- Florida caps emergency-declared claim fees at 10% for the first yearafter a Governor’s disaster declaration, then 20% thereafter, protecting consumers during hurricanes and major storms

- Your actual cost depends on settlement amount and claim complexity, ranging from a few thousand dollars on moderate claims to $50,000+ on major property losses

- Research shows public adjuster clients receive 4-8 times higher settlementsthan self-represented claimants, often resulting in net benefits even after fees

- Florida law prohibits fees on pre-existing paymentsand grants 10-30 day cancellation rights depending on claim type

- Large, complex, or disputed claims benefit most from representation, while small straightforward claims may not justify the percentage fee

- Always verify licensing and review contract terms carefully, watching for red flags like upfront fees, vague percentages, or terms exceeding legal limits