How to File a Property Damage Claim in Orlando: Complete 2026 Step-by-Step Guide

Quick Answer

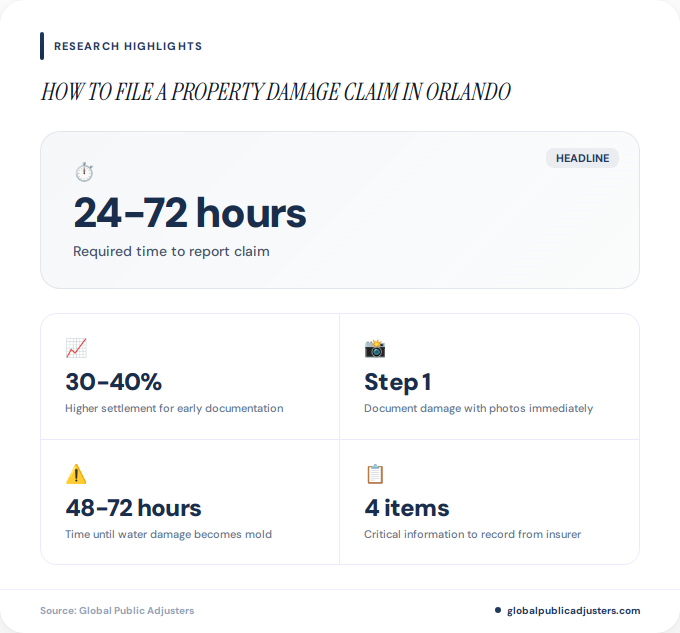

To file a property damage claim in Orlando, immediately report the loss to your insurance company, document all damage with dated photos and videos, preserve the scene until inspection, and gather repair estimates and receipts. The process requires timely notice (typically within 24-72 hours) and thorough evidence collection to maximize your settlement under Florida’s fault-based property damage laws.

When hurricane-force winds tear throughOrlando, or when a sudden pipe burst floods your Lake Nona home, knowing exactly how to file a property damage claim can mean the difference between a fair settlement and a financial disaster. Did you know that according to Florida insurance data, property owners who document their damage within the first24 hoursreceive settlements that are30-40% higherthan those who delay?

Filing a property damage claim in Orlando requires navigating Florida’s unique insurance landscape, understanding tight reporting deadlines, and building bulletproof documentation. Whether you’re dealing with storm damage in Winter Park, water damage in downtown Orlando, or vandalism in Kissimmee, this comprehensive guide walks you through every critical step.

The stakes are high: Florida’s 2023 legislative changes shortened many claim deadlines, and insurance companies in the Orlando market have become increasingly aggressive in claim denials. This guide arms you with the knowledge to protect your rights and maximize your settlement.

What to Do Immediately After Property Damage Occurs in Orlando

The first hours after discovering property damage areabsolutely criticalto the success of your claim. Insurance policies universally require prompt notice, and Florida law favors claimants who act immediately. Here’s what you must do before anything else.

Contact your insurance company immediately, ideally within24 hours. Most policies require notice “as soon as practicable,” and delays can provide grounds for claim denial. Call the claims hotline listed on your policy declarations page, not your agent’s office, and request a claim number. Write down the date, time, representative’s name, and claim number for your records.

Document everything with photographic and video evidencebefore touching anything. Take wide shots showing the entire affected area, then close-ups of specific damage. Include reference points (a ruler, newspaper with date) to establish scale and timing. If you’re dealing withmold damage in Orlando, capture any water intrusion sources and affected materials before contractors begin work.

Preserve the scene until inspection, unless emergency mitigation is required. Florida law generally requires you to prevent further damage (such as tarping a roof or shutting off water), but don’t dispose of damaged items or begin permanent repairs until an adjuster documents the loss. This balance between preservation and mitigation is crucial inproperty damage claims in Orlando.

File police or incident reportswhen damage involves criminal activity (theft, vandalism) or motor vehicle accidents. These official reports carry significant weight with insurers and establish third-party liability. For vandalism cases, Orlando Police Department reports become essential documentation.

How Does Florida Law Affect Your Property Damage Claim?

Understanding Florida’s legal framework is essential when filing a property damage claim in Orlando. The state’s insurance laws, liability standards, and recent legislative changes directly impact your rights and deadlines.

Florida operates under a fault-based systemfor property damage, meaning the person or entity that caused the damage (or their insurance carrier) is responsible for repair or replacement costs. This applies whether the damage stems from a car accident, negligence, or contractor error. According toFlorida property damage law resources, establishing clear fault is the foundation of successful third-party claims.

Auto-related property damage requires minimum coverage. Florida law mandates that all vehicle owners carry at least$10,000 in Property Damage Liability (PDL)coverage. If another driver damages your Orlando home, fence, or mailbox, their PDL coverage should pay for repairs. However, if they’re underinsured, your own collision or uninsured motorist property damage coverage may apply.

Statute of limitations deadlines are now shorter. For incidents occurring on or afterMarch 24, 2023, Florida’s tort reform legislation shortened the statute of limitations for most negligence-based property damage claims to2 years, down from the previous 4 years. However, some contract-based claims may still follow different timelines.Legal experts in Orlando property damageemphasize consulting with an attorney to determine which deadline applies to your specific situation.

| Claim Type | Statute of Limitations | Key Considerations |

|---|---|---|

| Negligence-based (post-3/24/23) | 2 years | Most personal injury and property tort claims |

| Contract-based claims | 4-5 years | Depends on written vs. oral contract |

| Insurance policy claims | Varies by policy | Often 1-3 years from date of loss |

What Are the Step-by-Step Filing Requirements?

Filing a property damage claim in Orlando follows a systematic process. Missing even one step can delay your settlement by weeks or provide grounds for denial. Here’s the exact sequence you need to follow.

Step 1: Review Your Insurance Policy

Read your declarations page and policy terms carefullybefore filing. Confirm your coverage limits for dwelling, personal property, loss of use, and specific perils. Check your deductible amount (typically$500 to $5,000+for Orlando homeowners) and note any exclusions. Hurricane deductibles in Central Florida often run2-10% of dwelling coverage, significantly higher than standard deductibles.

Pay special attention to water damage coverage. Standard homeowners policies typically cover sudden internal water damage (burst pipes) but exclude flooding, which requires separate National Flood Insurance Program (NFIP) coverage. Given Orlando’s flood zones, this distinction is crucial.

Step 2: Notify Your Insurer Promptly

Call your insurance company’s claims hotlineas soon as possible after discovering damage. Forresidential damage claims in Orlando, most insurers operate 24/7 hotlines. Provide basic information: your policy number, date/time of loss, type of damage, and preliminary estimate of extent.

Follow up the phone call with written notice if your policy requires it. Send via certified mail with return receipt requested to create a paper trail. Keep copies of all correspondence and note the claim number assigned.

Step 3: Build Your Evidence File

Compile comprehensive documentationbefore the adjuster arrives. Your evidence file should include:

- Photographs and videos showing damage from multiple angles

- Receipts, invoices, or appraisals proving ownership and value of damaged items

- Contractor estimates for repair or replacement

- Police reports (for theft, vandalism, or vehicle-related damage)

- Weather reports or incident reports supporting your timeline

- Correspondence with your insurance company

- Inventory lists with serial numbers for personal property

Forbathroom damage in Orlando homes, include photos of plumbing systems, water damage to adjacent rooms, and any prior inspection reports showing the system was properly maintained.

Step 4: Meet with the Insurance Adjuster

Schedule and prepare for the adjuster’s inspection. The insurance company will assign an adjuster to evaluate your claim, typically within7-14 daysof initial notice (faster for emergency situations). During the inspection, the adjuster will photograph damage, measure affected areas, ask questions, and assess repair costs.

Be present during the inspection but avoid speculation. Stick to verifiable facts: when you discovered the damage, what you observed, what immediate steps you took. Don’t guess about causes or provide opinions about what the insurance should cover. Let your documentation speak for itself.

Step 5: Obtain Independent Estimates

Get your own contractor estimatesindependent of the insurance company’s assessment. Orlando property damage attorneys consistently advise obtaining at leasttwo to threeindependent repair estimates before accepting the insurer’s settlement offer. Professional contractors familiar with Central Florida building codes and material costs can identify damage the adjuster might minimize or overlook.

Repair costs in Orlando vary widely based on scope and quality, typically ranging from$5,000 to $50,000+for moderate damage and$50,000 to $200,000+for extensive hurricane or flood damage. Pricing depends heavily on materials, labor availability, permit requirements, and whether repairs involve structural elements. Request itemized estimates that break down labor, materials, and permitting costs.

Step 6: Review the Settlement Offer

Carefully evaluate the insurer’s initial offerbefore accepting. Most first offers from insurance companies come in20-50% lowerthan full replacement value, according to industry data. Compare the offer against your independent estimates, policy limits, and actual damages.

If the offer seems inadequate, you have the right to negotiate. Provide additional documentation, highlight items the adjuster may have missed, and reference your policy’s coverage terms. Written counter-offers with supporting evidence carry more weight than phone conversations.

What Documentation Do You Need for a Successful Claim?

The strength of your property damage claim in Orlando rests almost entirely on your documentation. Insurance companies make decisions based on verifiable evidence, not verbal descriptions or memory. Insufficient documentation is the leading cause of claim denials and low settlements.

Photographic and video evidenceshould be comprehensive and systematic. Take photos from multiple angles: wide shots showing entire rooms or structures, medium shots of damaged areas, and close-ups of specific items. Include reference points (a newspaper with date, a measuring tape, recognizable landmarks) to establish scale and timing. Video walk-throughs narrated with your observations create powerful evidence, especially for widespread damage.

Proof of ownership and valueseparates successful claims from denied ones. For personal property, gather receipts, credit card statements, appraisals, product manuals, warranty cards, and prior insurance declarations. If you lack receipts for damaged items, provide model numbers, purchase dates, and retail prices from comparable new items. For high-value items (jewelry, art, electronics over $2,500), professional appraisals significantly strengthen your claim.

Repair estimates from licensed contractorsprovide crucial third-party validation. Choose contractors licensed in Florida (verify through the Department of Business and Professional Regulation) and familiar with Orlando building codes. Request written estimates on company letterhead that itemize materials, labor, disposal costs, and permit fees. Multiple estimates demonstrate due diligence and reveal when an insurance adjuster’s assessment is unreasonably low.

| Document Type | Why It Matters | How to Obtain |

|---|---|---|

| Dated Photos/Videos | Establishes extent and timing of damage | Smartphone with timestamp, digital camera |

| Police Reports | Creates official record for theft/vandalism | Orlando Police Department online portal |

| Receipts/Appraisals | Proves ownership and actual cash value | Original purchase records, credit statements |

| Contractor Estimates | Validates repair costs vs. adjuster figures | Licensed local contractors (2-3 quotes) |

| Weather Reports | Corroborates storm/wind damage claims | National Weather Service historical data |

Maintenance and repair recordsdemonstrate that you properly maintained your property, which can defeat insurer arguments that damage resulted from neglect. Keep receipts for roof repairs, HVAC servicing, plumbing work, and pest control. For Orlando properties, annual roof inspections and hurricane preparation records are particularly valuable given the region’s exposure to tropical storms.

Communication logswith your insurance company create accountability. Document every phone call (date, time, representative name, summary of conversation), save all emails, and keep copies of letters sent and received. If a claim representative makes promises or commitments, confirm them in writing via email or certified letter.

What Types of Property Damage Claims Are Most Common in Orlando?

Orlando’s unique climate, geography, and development patterns create distinct property damage patterns. Understanding the specific challenges of your damage type helps you build a stronger claim and anticipate insurer responses.

Hurricane and Wind Damage

Tropical storms and hurricanes pose the greatest threatto Central Florida properties. According toOrlando hurricane damage attorneys, major storms cause billions in property damage across the region every few years. Common damage includes torn roofing, broken windows, structural impacts from fallen trees, and water intrusion from wind-driven rain.

Hurricane claims require specific documentation: pre-storm photos showing property condition, weather reports confirming wind speeds, and clear differentiation between wind damage (typically covered) and flood damage (requires separate coverage). Insurance companies often dispute causation, claiming water damage came from flooding rather than wind-driven rain through compromised roofing.

Water and Flood Damage

Water damage ranks as Orlando’s most frequent property claim. Sources include burst pipes, appliance failures, roof leaks, and sewage backups. Standard homeowners policies cover sudden internal water damage but exclude gradual leaks, maintenance-related issues, and ground flooding. Separate flood insurance through NFIP or private carriers covers rising water from storms, rivers, or overwhelming drainage systems.

The key distinction: water damage from above (covered) versus below (often not covered). Document the water source clearly, photograph the damage progression, and begin mitigation immediately to prevent mold, which develops in Orlando’s humid climate within 48-72 hours.

Fire and Smoke Damage

Fire losses are typically well-coveredunder standard policies, including dwelling repair, personal property replacement, additional living expenses, and debris removal. However, smoke and soot damage often extends far beyond the visible burn area, requiring professional cleaning and odor remediation.

For fire claims, preserve the scene until fire marshal and insurance investigations conclude. Obtain copies of the official fire report, photograph all damaged areas before cleanup, and inventory all affected possessions room by room. Working withexperienced public adjustershelps ensure hidden smoke damage doesn’t get overlooked in the settlement.

Vehicle-Related Property Damage

Car crashes into homes, fences, and mailboxesare surprisingly common in Orlando’s dense residential neighborhoods. These claims involve the at-fault driver’s auto liability insurance rather than your homeowners policy. Florida’s$10,000 minimum PDL requirementoften proves insufficient for major structural damage, requiring you to pursue the driver personally or tap your own collision coverage.

Document the scene immediately, call Orlando police to create an official accident report, photograph vehicle and property damage, and exchange insurance information with the driver. File claims with both the at-fault driver’s insurer and your own carrier to preserve all options.

Vandalism and Theft

Malicious damage and burglaryare covered under standard homeowners policies, subject to your deductible. File a police report immediately (essential for claim approval), document all missing or damaged items with photos and receipts, and change locks or secure entry points to prevent additional losses.

Insurance companies scrutinize these claims carefully for signs of fraud or staged losses. Complete honesty and thorough documentation are critical. If you discover the loss occurred while the property was vacant for more than 60 days, coverage may be limited or excluded entirely under vacancy clauses.

How Should You Work with Insurance Adjusters?

Your interaction with the insurance adjuster significantly influences your claim outcome. Understanding the adjuster’s role, motivations, and limitations helps you communicate effectively and protect your interests.

Remember that adjusters work for the insurance company, not for you. Their job is to settle claims fairly but also to minimize the insurer’s payout. Company adjusters receive performance evaluations based on settlement amounts, creating inherent pressure to lowball offers. Independent adjusters (hired by the insurer on a per-claim basis) may be slightly more objective but still represent the carrier’s interests.

Provide facts without speculationduring the inspection and interviews. Answer questions directly but don’t volunteer information beyond what’s asked. Never guess about causes, costs, or contributing factors. If you don’t know something, say so. Recorded statements require particular care: request to review your policy before giving one, and consider consulting witha professional advocatebeforehand.

Document all interactionswith the adjuster. Take notes during phone calls, save emails, and confirm verbal agreements in writing. If the adjuster suggests certain repairs or provides guidance, ask for it in writing. Memories fade and disputes about “who said what” almost always favor the insurance company in later disputes.

Be present during inspectionswhenever possible. Walk through the property with the adjuster, point out all damaged areas, and ensure nothing gets overlooked. Bring your own documentation file and photos to supplement the adjuster’s observations. Adjusters often work quickly, and items missed during the initial inspection can be difficult to add later.

Don’t accept the first offer immediately. Initial settlement offers rarely represent the maximum amount the insurer will pay. Review the offer against your independent estimates, policy limits, and actual losses. If gaps exist, prepare a detailed written response explaining why the offer is insufficient, supported by contractor estimates, receipts, and policy language.

What Common Mistakes Should You Avoid?

Even well-intentioned property owners make critical errors that jeopardize their claims. These mistakes can result in claim denials, reduced settlements, or policy cancellations.

Delaying notice to your insurerranks as the most common and costly mistake. Policies require “prompt” or “immediate” notice, and weeks of delay provide grounds for denial. Even if you’re unsure whether damage exceeds your deductible or is covered, report it anyway. You can always withdraw a claim, but you can’t retroactively cure late notice.

Beginning permanent repairs before inspectioneliminates the adjuster’s ability to verify your loss. Emergency mitigation (tarping, water extraction, securing openings) is required to prevent further damage, but replacing materials, repainting, or reconstructing before inspection gives the insurer ammunition to deny or reduce your claim. Photograph everything thoroughly before any work begins.

Accepting inadequate settlements out of frustrationhappens when claim delays stretch for months. Orlando property damage attorneys report that exhausted claimants often accept lowball offers just to “get it over with,” leaving thousands of dollars on the table. If the settlement doesn’t cover your documented losses, negotiate or seek professional assistance rather than accepting less than you’re owed.

Failing to read your policy carefullyleads to wrong assumptions about coverage. Many Orlando homeowners don’t realize their standard policies exclude flood damage, require higher hurricane deductibles, or limit coverage for certain high-value items. Read your policy before you need to file a claim, and ask your agent to explain confusing provisions.

Disposing of damaged property prematurelydestroys evidence the insurer may need to verify your claim. Keep damaged items until the adjuster has inspected them and authorized disposal. For large items or health hazards (mold, sewage), photograph extensively and get written permission before removal.

Providing inconsistent informationraises red flags. Ensure your account of when damage occurred, how it happened, and what you lost remains consistent across all communications. Innocent mistakes can appear fraudulent when different versions emerge in photos, police reports, and adjuster interviews.

When Should You Hire a Public Adjuster or Attorney?

Not every property damage claim requires professional representation, but certain situations strongly favor hiring specialized help. Understanding when the cost of professional assistance pays for itself can maximize your net settlement.

Consider hiring a public adjuster whendamage is extensive (claims exceeding$10,000 to $15,000), the insurer denies or significantly undervalues your claim, you lack time or expertise to document and negotiate effectively, or the claim involves complex issues like mold, structural damage, or business interruption. Public adjusters work exclusively for policyholders, documenting losses, preparing estimates, and negotiating settlements. They typically charge10-20% of the final settlement, but experienced adjusters often increase settlements by30-50% or more, resulting in higher net recovery even after fees.

When evaluatingpublic adjuster costs in Orlando, remember that fees are usually contingent (no recovery, no fee) and are deducted from the settlement rather than paid upfront. The cost-benefit analysis typically favors hiring a public adjuster for claims over $15,000 to $20,000 or when the insurer offers substantially less than your independent estimates.

Hire an attorney whenthe insurance company denies your claim outright, acts in bad faith (unreasonable delays, lowball offers without explanation, failure to investigate), the dispute involves significant money (over$25,000 to $50,000), or third-party liability is disputed. Property damage attorneys handle claim litigation, bad faith lawsuits, and recovery from at-fault parties. Most work on contingency (typically33-40% of recovery), meaning no upfront costs.

According toOrlando property damage legal experts, attorney representation becomes essential when your claim exceeds policy limits and you need to pursue the at-fault party personally, or when the insurer’s conduct suggests bad faith. Under Florida law, bad faith claims can result in damages beyond the policy limits plus attorney fees.

For smaller claims under $5,000 to $10,000, self-representation usually makes financial sense. Follow the documentation and negotiation steps outlined in this guide, obtain multiple contractor estimates, and be persistent in your communications. Reserve professional assistance for situations where the complexity or disputed amount justifies the cost.

Remember thattiming matters when hiring a public adjuster in Florida. While you can engage one at any point before settlement, earlier involvement allows better documentation and evidence preservation. Many adjusters offer free claim reviews to help you determine whether professional representation would benefit your specific situation.

Key Takeaways

- Report property damage to your Orlando insurer within 24 hoursto comply with policy requirements and preserve your coverage rights. Delayed notice is the leading cause of claim denials.

- Document damage comprehensively with dated photos, videos, receipts, and contractor estimatesbefore beginning any permanent repairs. Your evidence file determines your settlement amount.

- Florida’s 2023 tort reform shortened the statute of limitations to 2 yearsfor most negligence-based property damage claims occurring after March 24, 2023, making prompt action even more critical.

- Obtain independent repair estimates from at least two licensed Orlando contractorsbefore accepting the insurance adjuster’s assessment. First offers typically come in 20-50% below full value.

- Understand your policy’s coverage, deductibles, and exclusionsbefore filing. Orlando’s hurricane deductibles often run 2-10% of dwelling coverage, and flood damage requires separate insurance.

- Preserve damaged property until the adjuster inspects it, but take immediate mitigation steps (tarping, water extraction) to prevent additional loss. Photograph everything before and after emergency repairs.

- Consider hiring a public adjuster for claims exceeding $15,000 to $20,000or when the insurer’s offer seems unreasonably low. Professional representation often increases net recovery despite fees.

People Also Ask

How long do I have to file a property damage claim in Orlando?

Most insurance policies require you to report property damage “as soon as practicable,” typically within 24-72 hours of discovery. The statute of limitations for negligence-based claims is now 2 years in Florida (as of March 2023), while contract-based claims may have longer periods. Check your specific policy for exact deadlines.

What is the average property damage claim payout in Orlando?

Property damage settlements in Orlando vary widely based on the type and extent of damage, ranging from $5,000 to $50,000+ for moderate damage and $50,000 to $200,000+ for extensive losses. Hurricane and flood claims average significantly higher than minor water or vandalism losses. Your actual payout depends on your coverage limits, deductible, and documentation quality.

Does homeowners insurance cover water damage in Orlando?

Standard Orlando homeowners policies cover sudden internal water damage (burst pipes, appliance failures) but exclude flooding from external sources, gradual leaks, and maintenance-related issues. Flood damage requires separate NFIP or private flood insurance. The distinction between covered and excluded water damage is the most disputed issue in Orlando property claims.

Can I do my own repairs before the insurance adjuster arrives?

You should perform emergency mitigation (tarping, water extraction, securing openings) to prevent further damage, but avoid permanent repairs or disposal of damaged property until after the adjuster’s inspection. Document everything with photos and videos before any work begins. Premature repairs can result in claim denials or reduced settlements.

What should I do if my Orlando property damage claim is denied?

Request a written explanation of the denial citing specific policy language, then review your policy carefully to determine if the denial is justified. Gather additional documentation, obtain independent expert opinions, and submit a formal appeal in writing. For significant claims, consult with a public adjuster or property damage attorney to evaluate your options for dispute resolution or litigation.

How much does a public adjuster cost in Orlando?

Orlando public adjusters typically charge 10-20% of the final settlement amount on a contingency basis, meaning no recovery equals no fee. The percentage often decreases for larger claims. While this represents a significant cost, experienced public adjusters frequently increase settlements by 30-50% or more, resulting in higher net recovery even after their fee is deducted.

Frequently Asked Questions

What documentation do I need to file a property damage claim in Orlando?+

You need dated photos and videos of all damage, proof of ownership (receipts, appraisals, serial numbers), contractor repair estimates, police reports (for theft or vandalism), weather reports (for storm damage), your insurance policy and declarations page, and a detailed inventory of damaged items. Keep copies of all correspondence with your insurer and document every phone conversation.

How long does it take to settle a property damage claim in Orlando?+

Simple claims with clear liability and documentation can settle within 2-4 weeks. Complex claims involving structural damage, disputes about coverage, or multiple parties often take 2-6 months or longer. Hurricane-related mass claims can extend the timeline due to adjuster shortages and contractor backlogs. Florida law requires insurers to acknowledge claims within 14 days and either accept or deny within 90 days.

Will filing a property damage claim increase my Orlando insurance rates?+

Filing a claim can potentially increase your rates or affect renewability, particularly if you file multiple claims within a 3-5 year period. However, not all claims affect rates equally; weather-related losses may have less impact than claims suggesting negligence. The rate increase risk should be weighed against out-of-pocket repair costs, especially for claims only slightly exceeding your deductible.

What is actual cash value versus replacement cost in Orlando claims?+

Actual Cash Value (ACV) pays for replacement cost minus depreciation based on the item’s age and condition, while Replacement Cost Value (RCV) pays the full cost to replace with new comparable items without deducting depreciation. Most Orlando insurers initially pay ACV, then reimburse the depreciation amount (recoverable depreciation) after you complete repairs and submit receipts. RCV coverage costs more but provides significantly better protection.

Can I choose my own contractor for repairs in Orlando?+

Yes, you have the right to hire any licensed contractor you choose for repairs. Insurance companies may suggest preferred contractors or direct repair programs, but you are not required to use them. Obtain multiple estimates, verify Florida licensing, check references, and ensure contractors are familiar with Orlando building codes and permit requirements before making your selection.

What is Florida’s Property Damage Liability minimum requirement?+

Florida requires all vehicle owners to carry at least $10,000 in Property Damage Liability (PDL) coverage, which pays for damage your vehicle causes to another person’s property. This minimum often proves insufficient for major accidents involving Orlando homes, fences, or expensive vehicles, making higher PDL limits (typically $50,000 to $100,000+) a prudent choice for adequate protection.

Should I give a recorded statement to the insurance adjuster?+

Related:How to Appeal an Insurance Claim Denial in Orlando: Your Complete 2026 Guide

Related:How Much Does a Public Adjuster Cost in Jacksonville? Complete 2026 Fee Guide

Related:Water Damage Adjuster in Florida: Complete 2026 Guide to Claims, Costs, and Coverage

Your policy may require you to cooperate with reasonable investigations, which can include recorded statements. Before giving one, review your policy carefully, organize your facts and documentation, and consider consulting with a public adjuster or attorney. Answer questions directly and truthfully but don’t speculate or volunteer information beyond what’s asked. You have the right to request additional time to prepare or have representation present.