Fire Claims Adjuster in Jacksonville: Your Complete 2026 Guide to Fire Damage Recovery

Quick Answer

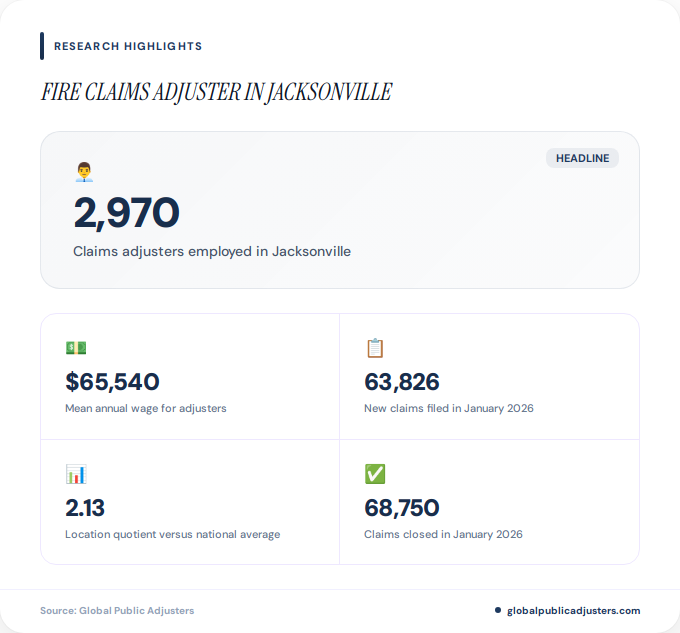

A fire claims adjuster in Jacksonville is a licensed professional who evaluates fire damage to homes and businesses, documents losses, and negotiates insurance settlements. Jacksonville employs approximately 2,970 claims adjusters with a mean annual wage of $65,540, working in an environment with over 63,000 new claims monthly as of January 2026.

When fire strikes your Jacksonville home or business, the aftermath extends far beyond the visible damage. In January 2026 alone,63,826 new claimswere filed in the Jacksonville market, with68,750 claims closedduring the same period. This staggering volume highlights just how active Florida’s insurance claims environment has become, particularly in a coastal city facing increasing climate-driven risks.

Afire claims adjuster in Jacksonvilleserves as your professional advocate during one of life’s most stressful events. These licensed professionals navigate the complex intersection of insurance policy language, structural damage assessment, and fair compensation negotiation. With Jacksonville’s insurance market under significant stress and claims volume at historic highs, understanding the role and value of fire claims adjusters has never been more critical for property owners.

Whether your Riverside historic home suffered smoke damage, your San Marco business experienced a total loss, or your Mandarin property needs comprehensive fire restoration, the right adjuster can mean the difference between a fair settlement and a financial shortfall that lasts for years.

What Is a Fire Claims Adjuster in Jacksonville?

A fire claims adjuster in Jacksonville is alicensed insurance professionalwho specializes in evaluating fire damage to residential and commercial properties. These professionals fall into two primary categories: insurance company adjusters who work for carriers, and public adjusters who work exclusively for policyholders.

Public adjusters represent property owners throughout the entire claims process. They document fire damage, calculate losses (including both structural damage and contents), interpret policy language, and negotiate directly with insurance companies. In Florida’s complex regulatory environment,public adjusters must hold state licensureand meet continuing education requirements to maintain their credentials.

Jacksonville’s2,970 employed claims adjusters, examiners, and investigatorswork in an environment shaped by coastal exposure, hurricane risk, and an insurance market facing significant capacity challenges. The local concentration of claims professionals is notably high, with alocation quotient of 2.13, indicating that this occupation is more than twice as concentrated in Jacksonville compared to the national average.

Fire claims adjusters must understand building codes specific to Jacksonville neighborhoods, from the historic districts of Avondale and Springfield to the newer developments in Nocatee and Ponte Vedra Beach. They evaluate not only visible fire damage but also hidden issues like smoke infiltration in HVAC systems, structural compromise from heat exposure, and water damage from firefighting efforts.

How Do Fire Claims Adjusters Work in Jacksonville?

The fire claims adjustment process begins immediately after a fire loss. Professional adjusters follow a systematic approach that balances thoroughness with urgency, recognizing that Jacksonville property owners need both accurate assessments and timely settlements.

Initial Documentation and Assessment:Within hours of engagement, a fire claims adjuster visits the property to document all visible damage. This includes comprehensive photography, detailed written notes, and preliminary damage estimates. In Jacksonville’s humid climate, adjusters also assess potential secondary damage from moisture and mold that can develop rapidly after firefighting water exposure.

Modern adjusters increasingly useadvanced technology including drones and aerial imageryfor damage assessment, particularly when structures are unsafe to enter or when roof damage requires evaluation. This technological shift has transformed how fire damage documentation occurs, providing more comprehensive evidence for claims negotiations.

Damage Inventory and Valuation:Fire adjusters create detailed inventories of damaged and destroyed property. This extends beyond the obvious structural elements to include contents, personal property, improvements, and code upgrade requirements. For Jacksonville businesses, this may encompass equipment, inventory, business interruption losses, and extra expense claims.

The adjuster compares the documented losses against policy coverage, identifying applicable provisions and exclusions. They calculate replacement cost versus actual cash value, depreciation schedules, and code compliance upgrade expenses that often surprise property owners who aren’t familiar with current building standards.

Negotiation and Settlement:Armed with comprehensive documentation, the adjuster presents the claim to the insurance carrier. This typically involves multiple rounds of negotiation, with the adjuster advocating for full and fair compensation under the policy terms. In Jacksonville’s active claims environment, adjusters must navigate carrier workload pressures, adjuster turnover, and varying interpretation of policy language.

Why Should Jacksonville Residents Hire a Fire Claims Adjuster?

Jacksonville property owners face unique challenges when filing fire claims. The combination of complex policies, catastrophe-exposed insurance markets, and the emotional trauma of fire loss creates an environment where professional representation delivers measurable value.

Policy Complexity and Coverage Maximization:Modern insurance policies contain dozens of coverage provisions, endorsements, exclusions, and limitations. Professional adjusters understand how to identify and activate all applicable coverage sections. For fire claims, this may include dwelling coverage, other structures, loss of use, code upgrade provisions, and debris removal, all of which have separate limits and conditions.

Many Jacksonville homeowners discover too late that their insurance company’s adjuster represents the carrier’s interests, not theirs. Apublic adjuster working in Jacksonvilleexclusively represents the policyholder, creating a level playing field during negotiations.

Accurate Damage Assessment:Fire damage extends far beyond visible destruction. Smoke particulates infiltrate porous materials, heat compromises structural integrity, and corrosive byproducts continue damaging electrical and mechanical systems long after flames are extinguished. Professional adjusters understand these hidden losses and ensure they’re documented and claimed.

In Jacksonville’s older neighborhoods like Riverside, San Marco, and Ortega, fire claims often trigger mandatory code upgrades for electrical systems, plumbing, and structural reinforcement. These upgrade costs can add tens of thousands of dollars to a claim, but only if properly identified and documented.

Time and Stress Reduction:Managing a fire claim while dealing with temporary housing, family disruption, and emotional trauma overwhelms most property owners. Professional adjusters handle all claim-related tasks, from documentation through settlement, allowing property owners to focus on their families and lives.

Jacksonville Fire Claims Adjuster Employment and Wage Data

Understanding the local employment landscape for fire claims adjusters provides insight into market dynamics, career opportunities, and the professionalization of claims handling in Jacksonville.

| Metric | Jacksonville | National |

|---|---|---|

| Total Employment | 2,970 | 285,270 |

| Mean Annual Wage | $65,540 | $73,380 |

| Mean Hourly Wage | $31.51 | $35.28 |

| Location Quotient | 2.13 | 1.00 |

| Jobs per 1,000 | 4.11 | 1.93 |

The data from theBureau of Labor Statistics occupational employment surveyreveals several important patterns about Jacksonville’s claims adjuster market. The significantly higher location quotient indicates that insurance claims handling represents a more important part of Jacksonville’s economy compared to most U.S. metro areas.

Jacksonville’smean annual wage of $65,540sits below the national average, reflecting regional cost-of-living differences and market dynamics. However, experienced fire claims adjusters, particularly those working on catastrophe assignments or in specialized public adjusting roles, often earn substantially more than these averages.

National wage distribution data shows the career progression potential. While entry-level positions start around$46,040 annually (10th percentile), experienced professionals can reach$85,250 to $102,630+ (75th to 90th percentile), demonstrating significant income growth for those who develop specialized expertise in complex claims like fire losses.

What Industry Trends Are Affecting Fire Claims Adjusters in 2026?

The fire claims adjustment profession is experiencing rapid transformation driven by technology adoption, climate change impacts, and evolving customer expectations. Jacksonville adjusters must adapt to these changes while maintaining the core skills that make claims handling effective.

Automation and Artificial Intelligence:Insurance carriers are deployingAI systems for claims triage, document review, and fraud detection. While these systems improve efficiency for routine claims, complex fire losses still require experienced human judgment. The technology augments adjuster capabilities rather than replacing them, particularly for large or complicated claims where policy interpretation and negotiation skills remain essential.

Machine learning algorithms can now scan thousands of repair estimates, identify pricing anomalies, and flag potentially inflated claims. Fire claims adjusters must understand these systems and provide documentation that satisfies both automated screening and human review.

Remote and Digital Workflows:The shift toward remote adjusting accelerated dramatically over recent years. Virtual inspections, digital documentation platforms, and centralized claim processing have become standard practice. Jacksonville adjusters increasingly work from home offices while using advanced software to manage claim workflows, communicate with clients, and collaborate with contractors and engineers.

However, serious fire losses still demand in-person inspection. The smell of smoke, the feel of damaged materials, and the spatial understanding that comes from walking through a structure cannot be fully replicated through video calls and photographs. The most effective adjusters blend digital efficiency with traditional hands-on assessment skills.

Climate-Driven Loss Complexity:Jacksonville’s coastal location places properties at risk from multiple perils that often overlap. A structure weakened by hurricane winds may be more susceptible to electrical fires. Flooding can compromise fire suppression systems. These overlapping perils create complicated causation questions that affect coverage and settlement amounts.

Fire claims adjusters must understand how different policy sections interact when multiple perils contribute to a loss. This requires not only technical expertise but also persuasive communication skills to present complex causation arguments to insurance carriers.

Job Outlook and Workforce Changes:According toinsurance industry workforce analysis, claims adjuster positions face pressure from automation and workflow changes. The World Economic Forum’s Future of Jobs Report 2025 ranks claims adjusters among occupations expected to see declining employment through 2030.

However, this projection reflects the consolidation of routine claims processing rather than the elimination of professional adjustment services. Specialized adjusters who handle complex losses, maintain deep technical knowledge, and deliver superior customer experiences will continue to find strong demand. Fire claims, with their inherent complexity and high stakes, represent one of the specializations most resistant to automation.

How to Choose the Right Fire Claims Adjuster in Jacksonville

Selecting a fire claims adjuster represents one of the most consequential decisions property owners make after a fire loss. The right professional can increase your settlement by tens or even hundreds of thousands of dollars while reducing stress during an already difficult time.

Licensing and Credentials:Florida requires public adjusters to hold state licensure, complete continuing education, and maintain professional standards. Verify that any adjuster you consider holds a currentFlorida public adjuster licensethrough the Department of Financial Services website. This basic credential ensures the adjuster has met minimum competency requirements and is subject to regulatory oversight.

Beyond basic licensing, look for adjusters with specialized training in fire loss evaluation, structural assessment, and contents restoration. Professional designations and ongoing education in areas like building codes, construction methods, and insurance policy interpretation indicate a commitment to expertise.

Local Jacksonville Experience:Fire claims adjustment requires knowledge of local building practices, contractor availability, permit processes, and replacement cost patterns. An adjuster familiar with Jacksonville’s neighborhoods understands that restoration costs in Ponte Vedra Beach differ from those in Northside, and that historic district regulations in Riverside create unique compliance requirements.

Ask prospective adjusters about their experience with Jacksonville properties similar to yours. A firm with deep local roots, such asGlobal Public Adjusters, brings relationships with local contractors, engineers, and restoration specialists that can accelerate your recovery.

Communication and Responsiveness:Fire victims need clear, regular communication about claim status, settlement progress, and next steps. During initial consultations, assess how well the adjuster explains the process, answers your questions, and sets realistic expectations. Adjusters who provide direct contact information and commit to specific response timeframes typically deliver superior service throughout the claim.

Track Record and References:Request references from recent fire claim clients with similar property types and loss scales. Ask about settlement outcomes, communication quality, and overall satisfaction. Established firms should readily provide references and may maintain online reviews or testimonials demonstrating their track record.

What Does a Fire Claims Adjuster Cost in Jacksonville?

Understanding the cost structure for public adjuster services helps property owners make informed decisions about representation.Public adjuster feestypically follow a percentage-based model, with the adjuster receiving a portion of the settlement increase they achieve.

Typical Fee Structures:In Jacksonville, public adjuster fees generally range from5% to 20% of the claim settlement, depending on several factors including claim size, complexity, and whether the claim is for an open loss or a reopened settlement. Larger commercial claims often command lower percentage fees, while smaller residential claims may be at the higher end of the range.

The fee percentage reflects the adjuster’s risk and investment. They conduct extensive documentation, hire experts when needed, and invest substantial time negotiating with carriers, all typically without upfront payment. The contingency structure aligns the adjuster’s interests with maximizing your settlement.

Value Versus Cost:Property owners should evaluate adjuster fees in the context of settlement increases. If a fire claim initially valued at $150,000 by your insurance carrier settles for $275,000 with professional representation, a 10% adjuster fee of $27,500 still leaves you with a net gain of $97,500 compared to accepting the original offer.

Research consistently shows that professionally represented claimants receive significantly higher settlements than those who self-represent, often more than covering the adjuster fee. The true cost isn’t the adjuster’s percentage but rather the money left on the table by not having expert representation.

Fee Transparency and Agreements:Reputable adjusters provide clear written fee agreements before beginning work. These contracts specify the percentage, how it’s calculated, what services are included, and how disputes are resolved. Florida law regulates public adjuster contracts, requiring specific disclosures and providing property owners with cancellation rights.

Be wary of adjusters who request upfront fees, as Florida regulations prohibit this practice for public adjusters. The contingency fee structure protects property owners by ensuring adjusters only get paid when they deliver results.

Key Takeaways

- Jacksonville employs 2,970 claims professionalswith a location quotient more than double the national average, reflecting the area’s high claims volume and insurance industry presence.

- Fire claims adjusters earn a mean annual wage of $65,540 in Jacksonville, with experienced specialists and those handling complex losses earning substantially more than this average.

- January 2026 saw 63,826 new claims filedin the Jacksonville market, demonstrating the extremely active claims environment local property owners navigate.

- Professional fire claims adjusters use advanced technologyincluding drones, digital documentation systems, and comprehensive damage assessment tools while maintaining essential hands-on evaluation skills.

- Public adjusters work exclusively for property owners, not insurance companies, creating balanced representation during claim negotiations and maximizing settlement outcomes.

- Adjuster fees typically range from 5% to 20% of the settlementon a contingency basis, with the investment generally more than offset by increased claim payments compared to self-representation.

- Local Jacksonville expertise matters significantlybecause of unique building codes, neighborhood characteristics, contractor markets, and regional construction cost patterns that affect accurate claim valuation.

People Also Ask

What does a fire claims adjuster do?

A fire claims adjuster evaluates fire damage to properties, documents all losses including structural damage and contents, calculates the value of the claim, and negotiates with insurance companies to secure fair settlements. They interpret policy language and ensure all applicable coverage provisions are identified and claimed.

How much do fire claims adjusters make in Jacksonville?

Fire claims adjusters in Jacksonville earn a mean annual wage of $65,540 according to Bureau of Labor Statistics data, with entry-level positions starting around $46,000 and experienced specialists earning $85,000 to $102,000 or more. Public adjusters working on a contingency fee basis may earn substantially more when handling large commercial claims.

When should I hire a fire claims adjuster in Jacksonville?

You should hire a fire claims adjuster immediately after a fire loss, ideally before giving a recorded statement to your insurance company or accepting any settlement offer. Early engagement allows the adjuster to document damage while evidence is fresh and prevents you from making statements that might limit your claim later.

What’s the difference between an insurance adjuster and a public adjuster?

An insurance adjuster works for the insurance company and represents the carrier’s interests in minimizing claim payments. A public adjuster works exclusively for the property owner and is paid to maximize the claim settlement, creating balanced representation during negotiations.

Do I need a fire claims adjuster for small fire damage?

Even seemingly small fires often cause hidden damage including smoke infiltration, heat compromise of structural elements, and corrosive byproducts affecting electrical and mechanical systems. A professional adjuster can identify these hidden losses that property owners typically miss, often increasing settlements by amounts that far exceed adjuster fees even on smaller claims.

How long does the fire claims process take in Jacksonville?

Fire claim timelines vary significantly based on damage extent, policy complexity, and insurance carrier responsiveness. Simple claims may resolve in 30 to 60 days, while complex commercial losses or disputed claims can take six months or longer. Professional adjusters often accelerate the process through efficient documentation and carrier relationships.

Frequently Asked Questions

Can I hire a fire claims adjuster after already filing my claim?+

Yes, you can hire a public adjuster at any point during the claims process, even after filing. However,earlier engagement provides better resultsbecause adjusters can document damage more thoroughly and prevent you from making statements or accepting offers that might limit your recovery. Even if you’ve already received a settlement offer, an adjuster can review it and potentially negotiate a better outcome.

Will hiring a fire claims adjuster delay my settlement?+

Professional adjusters typically accelerate the claims process rather than delay it. Their expertise in documentation, policy interpretation, and carrier communication streamlines negotiations. While thorough documentation takes time upfront, it prevents the back-and-forth revisions and disputes that often delay self-represented claims. The modest additional time investment usually results in significantly higher settlements that more than justify the wait.

Does my insurance company pay the public adjuster’s fee?+

No, the property owner pays the public adjuster from the settlement proceeds, not the insurance company. The fee is typically a percentage of the total settlement, deducted when the insurance company issues payment. This contingency structure aligns the adjuster’s interests with maximizing your settlement, as their compensation directly depends on the claim outcome.

What documentation should I gather before meeting with a fire claims adjuster?+

Gather your insurance policy documents, any previous appraisals or home inspections, receipts for valuable items, photographs of your property before the fire, and any communication you’ve already had with your insurance company. However, professional adjusters will guide you through the documentation process, so don’t delay hiring an adjuster if you can’t locate all documents immediately. They can often obtain policy information directly from carriers.

Are fire claims adjusters regulated in Florida?+

Yes, Florida heavily regulates public adjusters through the Department of Financial Services.Public adjusting firms in Floridamust hold state licenses, maintain continuing education, carry professional liability insurance, and follow strict standards for contracts, advertising, and client representation. This regulatory framework protects consumers and ensures professional competency.

Can a fire claims adjuster help with business interruption claims?+

Yes, experienced fire claims adjusters handle business interruption claims in addition to property damage. They work with forensic accountants to document lost income, calculate continuing expenses, and present comprehensive business interruption claims to carriers. These claims are particularly complex and benefit significantly from professional representation, often resulting in substantially higher settlements than business owners achieve on their own.

What happens if I disagree with my fire claims adjuster’s approach?+

Related:How to File an Insurance Claim in Florida: Jacksonville Homeowners and Auto Policy Holders Guide

Related:How to File a Property Damage Claim in Orlando: Complete 2026 Step-by-Step Guide

Reputable adjusters maintain open communication and explain their strategy throughout the process. If disagreements arise, discuss your concerns directly with the adjuster or their supervisor. Florida law provides property owners with cancellation rights under public adjuster contracts, typically allowing termination with written notice. However, most disputes can be resolved through discussion, and switching adjusters mid-claim can sometimes delay resolution and reduce settlement outcomes.