How to Appeal an Insurance Claim Denial in Orlando: Your Complete 2026 Guide

Quick Answer

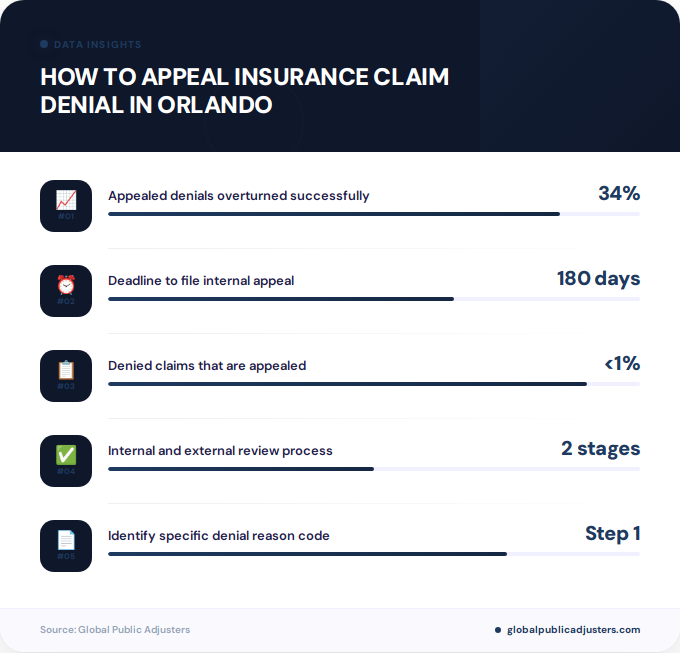

To appeal an insurance claim denial in Orlando, identify the specific denial reason in your notice, gather all supporting medical records and policy documents, file a written internal appeal within 180 days (deadline varies by plan), and if unsuccessful, request an external review through Florida’s insurance oversight or federal processes. Fast action, thorough documentation, and a written argument that directly addresses the insurer’s stated reason yield the best outcomes.

Receiving an insurance claim denial can feel like a devastating blow, especially when you believed your policy covered the treatment, repair, or service in question. Here’s a surprising fact that might give you hope: according toKFF’s 2024 analysis of ACA Marketplace plans, about34% of appealed denials were overturnedor resolved in the consumer’s favor. The catch? Fewer than1% of denied claimswere ever appealed, meaning most people simply accept their denial without question.

If you’re facing a claim denial in Orlando, you have more power than you might think. The appeal process exists precisely to correct insurer mistakes, provide additional context, and ensure you receive the coverage you’ve been paying for. Whether you’re dealing with a health insurance denial in the Dr. Phillips area, a property claim rejection in Winter Park, or any other insurance dispute across the Orlando metro region, understanding how to appeal an insurance claim denial in Orlando can make the difference between accepting a denial and recovering thousands of dollars in coverage.

This comprehensive guide walks you through every step of the Florida appeal process, backed by real data, expert insights, and proven strategies that work in 2026.

Understanding Why Insurance Claims Get Denied

Before you can successfully appeal an insurance claim denial in Orlando, you need to understand exactly why insurers reject claims in the first place. Denial letters typically cite one or more specific reasons, and identifying these reasons is the first critical step in building your appeal.

Common denial reasons include coding errors (especially in health insurance), claims that the treatment or service was “not medically necessary,” services deemed “experimental or investigational,” treatment from out-of-network providers without authorization, missing documentation, or policy exclusions. Property insurance claims in Orlando’s subtropical climate often face denials related to maintenance issues, gradual damage versus sudden loss, or disputes about whether damage occurred during a covered event like a hurricane or tropical storm.

TheAmerican College of Rheumatology emphasizesthat your denial letter is the roadmap for your appeal. Read it carefully, highlight the specific reason codes or language used, and focus your appeal directly on refuting those exact points with evidence and policy language.

What Is the Insurance Appeal Process in Orlando?

For Orlando residents, there is no separate city-level appeal system for insurance denials. Instead, you follow the same Florida state and federal consumer appeal rules that apply throughout the state. The process typically involves two main stages: an internal appeal (reviewed by your insurance company) and, if that fails, an external review (conducted by an independent third party).

Thefederal HealthCare.gov system notesthat consumers have a right to both internal appeal and external review for most health insurance plans, with urgent cases eligible for an accelerated process that can be decided in as little as72 hours.

For property insurance claims in Orlando, the process typically involves submitting additional documentation to your insurer, requesting a re-inspection if damage was undervalued, and potentially filing a complaint with Florida’s Department of Financial Services if the insurer is not cooperating. Many Orlando policyholders working withprofessional claims assistance in Orlandofind that having expert documentation and representation significantly improves their success rate.

How Quickly Must You File an Appeal in Florida?

Time is absolutely critical when learning how to appeal an insurance claim denial in Orlando. Miss your deadline, and you forfeit your right to appeal entirely, no matter how strong your case might be.

For health insurance, most plans allow approximately180 daysfrom the denial notice to file an internal appeal, though this varies by plan type and specific policy language. TheNational Association of Insurance Commissioners consumer guidenotes that urgent-care appeals may need to be decided within72 hours, while non-urgent pre-service appeals are often filed within30 daysin certain plan contexts.

For property insurance claims in Florida, including those in Orlando’s Lake Nona, Baldwin Park, or College Park neighborhoods, the timeline depends on your policy language. However, Florida law generally requires insurers to respond to your appeal or additional documentation within specific timeframes. Acting quickly is always in your best interest.

| Appeal Type | Typical Filing Deadline | Insurer Response Time |

|---|---|---|

| Health Insurance (Non-Urgent) | 30-180 days | 30-60 days |

| Health Insurance (Urgent) | Immediately | 72 hours |

| Property/Casualty | Varies by policy | 30-90 days |

What Documentation Do You Need for a Successful Appeal?

The quality of your documentation often determines whether your appeal succeeds or fails. Insurers uphold66% of denialson appeal, which means weak or incomplete submissions are routinely rejected. The difference between that 66% failure rate and the 34% success rate typically comes down to the strength of your evidence.

For health insurance appeals, gather your complete policy document (not just the summary of benefits), the original denial letter, all medical records related to the service or treatment, itemized bills, test results, imaging studies, a detailed letter of medical necessity from your treating physician, peer-reviewed medical literature supporting the treatment (for experimental treatment denials), and documentation of previous treatments tried and failed (for step-therapy denials).

For property insurance claims common in Orlando’s climate, such as hurricane damage, water damage, or fire claims, collect your policy documents, the original claim denial letter, photos and videos of all damage (timestamped if possible), repair estimates from licensed contractors (multiple estimates strengthen your case), receipts for emergency repairs, weather reports or official records documenting the event, and any inspection reports from the insurer’s adjuster.

The American College of Rheumatology advises patients to begin by carefully reviewing the denial letter and collecting the policy language, medical records, test results, prior treatments, and a letter of medical necessity from the treating clinician. This comprehensive documentation forms the foundation of a winning appeal.

How Does the Internal Appeal Work?

The internal appeal is your first formal opportunity to challenge the denial. This process is handled entirely within your insurance company, typically by a different reviewer or team than the one who made the original denial decision.

Start by contacting your insurer immediately to confirm the appeal process, deadline, and submission requirements. Request the name and direct contact information of the person handling your appeal. Document every conversation with date, time, person’s name, and what was discussed.

Write a clear, professional appeal letter that opens with your policy number, claim number, and a direct statement that you are formally appealing the denial. Reference the specific denial reason from your letter and systematically refute each point with evidence. Attach all supporting documentation in an organized manner, with a cover sheet listing each attachment. For Orlando residents dealing withcomplex property claims, having a public adjuster prepare this documentation can significantly improve the appeal’s strength.

Submit your appeal via certified mail with return receipt requested, and keep copies of everything. For urgent health appeals, you may also submit via fax or online portal, but always follow up to confirm receipt.

When Should You Request an External Review?

If your internal appeal is denied, you have the right to an external review by an independent third party who has no financial relationship with your insurance company. This is a powerful consumer protection that often yields better results than the internal process.

For health insurance, you can typically request an external review after exhausting your internal appeals, or in some urgent cases, simultaneously with your internal appeal. The external reviewer examines your case fresh, with no bias toward the insurer, and their decision is binding in most cases.

Florida residents can alsofile complaints with Florida’s Department of Financial Serviceswhen insurers are not cooperating or acting in bad faith. This regulatory oversight adds another layer of consumer protection, especially important in Orlando where hurricane-related property claims can face unfair denials.

The external review process is typically free or low-cost to consumers. According toProPublica’s investigation of external reviews, consumers who pursue external review see higher overturn rates than those who stop after the internal appeal.

What Are Your Actual Chances of Winning an Appeal?

Understanding the real statistics behind insurance appeals helps set realistic expectations and demonstrates why the effort is worthwhile. Based on the most recent data available, the numbers are more encouraging than many Orlando residents realize.

In 2024, KFF analyzed ACA Marketplace plans and found that of the approximately85 million in-network claimsthat were denied, consumers appealed fewer than1%. This staggeringly low appeal rate means that insurers successfully discourage the vast majority of policyholders from exercising their rights.

However, of those who did appeal, about34% saw their denials overturnedor resolved in their favor. This means that roughly one in three people who take the time to properly appeal their denial wins their case. Given that denied claims can involve thousands or even tens of thousands of dollars in coverage, the potential return on the time invested in an appeal is substantial.

The66% uphold ratefor denials reveals an important truth: the quality of your appeal matters far more than simply filing one. A hastily written letter without supporting documentation will likely fail, while a comprehensive, well-documented appeal that directly addresses the insurer’s stated reasons has a much higher success rate.

For property insurance claims in Orlando, success rates vary widely based on the type of claim, the quality of documentation, and whether professional representation is involved. Many policyholders working with experienced public adjusters report significantly higher success rates, particularly for complex claims involving hurricane damage, water intrusion, or fire loss.

Should You Hire Professional Help for Your Appeal?

Many Orlando residents successfully navigate the appeal process on their own, particularly for straightforward denials with clear documentation issues. However, professional assistance can be invaluable for complex claims, high-value denials, or cases involving disputed medical necessity or property damage assessments.

For health insurance appeals, patient advocacy organizations and medical billing advocates specialize in navigating the appeal process. Your treating physician’s office may also have staff experienced in writing letters of medical necessity and gathering supporting documentation.

For property insurance claims, public adjusters are licensed professionals who work exclusively for policyholders, not insurance companies. They understand how to document damage comprehensively, interpret policy language, and build compelling appeals. Thecost of hiring a public adjuster in Orlandovaries based on claim complexity and recovery amount, typically ranging from 10% to 20% of the final settlement, but this investment often results in significantly higher payouts than handling the claim alone.

For legal appeals or cases involving potential bad faith, consulting with an insurance attorney may be appropriate. Florida law provides strong consumer protections, and insurers who wrongfully deny claims may face penalties beyond simply paying the claim. Understandingwhen professional help is neededcan save you time and maximize your recovery.

People Also Ask

Can I appeal an insurance denial more than once in Orlando?

Yes, most insurance policies allow for multiple levels of internal appeal, and if those are exhausted, you can pursue external review through independent third parties. Florida residents also have the option to file complaints with state insurance regulators if insurers are not acting in good faith.

How long does the insurance appeal process take in Florida?

Non-urgent health insurance appeals typically receive a decision within 30 to 60 days, while urgent appeals must be decided within 72 hours. Property insurance appeals vary by complexity but generally receive responses within 30 to 90 days, depending on the insurer and claim type.

What happens if my internal appeal is denied?

If your internal appeal is denied, you have the right to request an external review by an independent third party with no financial ties to your insurer. This external reviewer’s decision is typically binding and provides a fresh evaluation of your case with higher overturn rates than internal appeals.

Do I need a lawyer to appeal an insurance claim denial?

Most insurance appeals do not require a lawyer and can be successfully handled by policyholders with proper documentation. However, for high-value claims, complex medical necessity disputes, or cases involving potential bad faith by the insurer, consulting with an insurance attorney or public adjuster can significantly improve your chances of success.

Can I get emergency treatment while my appeal is pending?

Yes, you should never delay necessary medical treatment while waiting for an appeal decision. Request an expedited or urgent appeal if the denial affects ongoing treatment, and ask your provider about payment plans or financial assistance programs while the appeal is processed.

What if my insurance company doesn’t respond to my appeal?

If your insurer fails to respond within the required timeframe, you can file a complaint with Florida’s Department of Financial Services. Non-response or delayed response may constitute bad faith, which carries penalties for insurers and strengthens your case for external review or legal action.

Frequently Asked Questions

How much does it cost to appeal an insurance claim denial in Orlando?+

Filing an internal appeal with your insurance company is free, as it’s a consumer right included in your policy. External reviews are also typically free or involve only a nominal processing fee. If you hire a public adjuster, fees typically range from 10% to 20% of the recovered amount, while attorney fees vary based on the complexity of your case and whether they work on contingency.

What is the most common reason insurance claims are denied in Orlando?+

For health insurance, the most common reasons include coding errors, services deemed “not medically necessary,” and out-of-network provider issues. For property insurance in Orlando, common denial reasons include maintenance-related damage, gradual deterioration rather than sudden loss, and disputes about whether damage occurred during a covered event like a hurricane or storm.

Can I still appeal if I missed the initial deadline?+

While most appeals must be filed within the timeframe specified in your denial letter (typically 30 to 180 days), you may still have options. Contact your insurer to explain the delay and request an exception, especially if you can demonstrate good cause for missing the deadline. Some insurers will accept late appeals, particularly for complex claims or extenuating circumstances.

Should I accept a partial settlement or continue my appeal?+

This depends on the gap between the partial offer and your actual damages, the strength of your appeal, and your immediate financial needs. Before accepting any settlement, review it carefully with a public adjuster or attorney to ensure you’re not leaving significant money on the table. Many insurers offer low settlements hoping you won’t appeal.

What documentation strengthens a property insurance appeal in Orlando?+

The strongest property appeals include detailed photo and video documentation of all damage, multiple independent contractor estimates, maintenance records showing proper upkeep, weather data or official reports documenting the covered event, and expert assessments from licensed public adjusters or engineers. Professional documentation often makes the difference between a denied and approved claim.

Will appealing my claim affect my insurance rates or future coverage?+

Appealing a claim denial is your legal right and should not directly result in rate increases or policy cancellation. However, the underlying claim itself may affect your rates depending on the type of claim and your claims history. Never let fear of rate increases prevent you from appealing a wrongful denial.

How do Orlando hurricane claims differ from other property claims?+

Hurricane claims in Orlando often involve complex damage assessments distinguishing wind damage from water damage, which may fall under different policy provisions. These claims require detailed documentation of the storm event, professional assessments, and careful attention to policy language regarding named storms, flood coverage, and covered perils. Many Orlando residents benefit from professional public adjuster assistance for hurricane-related claims.

Key Takeaways

- Act quickly:Most appeal deadlines range from 30 to 180 days from the denial notice, and missing your deadline can forfeit your right to appeal entirely.

- Understand the reason:Your denial letter contains the specific reasons for rejection, and your appeal must directly address each point with evidence and policy language.

- Document thoroughly:The difference between the 66% of appeals that fail and the 34% that succeed typically comes down to the quality and completeness of supporting documentation.

- Use the two-step process:Start with an internal appeal through your insurer, and if that fails, pursue external review by an independent third party for a fresh evaluation of your case.

- Don’t accept defeat:With fewer than 1% of denied claims ever appealed, insurers count on policyholders giving up, but one in three appeals succeeds for those who persist.

- Consider professional help:For complex claims, high-value denials, or property damage disputes common in Orlando’s climate, public adjusters and patient advocates significantly improve success rates.

- Know your rights:Florida law and federal regulations provide strong consumer protections, including mandatory appeal processes, external review rights, and penalties for insurer bad faith.

Understanding how to appeal an insurance claim denial in Orlando empowers you to challenge wrongful rejections and recover the coverage you’ve been paying for. Whether you’re dealing with a health insurance denial in downtown Orlando, a property claim rejection in the surrounding neighborhoods, or any other insurance dispute, the appeal process exists to protect your rights.

The statistics show that appeals work when done properly. With one in three properly documented appeals succeeding, the effort invested in challenging your denial can result in thousands of dollars in recovered coverage. Don’t be part of the 99% who never appeal, especially when professional resources are available to guide you through the process.

Related:How Much Does a Public Adjuster Cost in Jacksonville? Complete 2026 Fee Guide

Related:Water Damage Adjuster in Florida: Complete 2026 Guide to Claims, Costs, and Coverage

Related:Water Damage Claims Adjuster in Orlando: Your Complete 2026 Guide to Expert Claim Representation

If you’re facing a complex property insurance claim denial in Orlando,Global Public Adjustersoffers expert claim representation to maximize your recovery. Our team understands Florida insurance law, Orlando’s unique climate-related challenges, and the documentation required to build winning appeals. Contact us today for a free claim evaluation and discover how professional advocacy can transform your denied claim into a successful settlement.