Public Adjuster Fees Florida Explained in Orlando: Your Complete 2026 Guide

Quick Answer

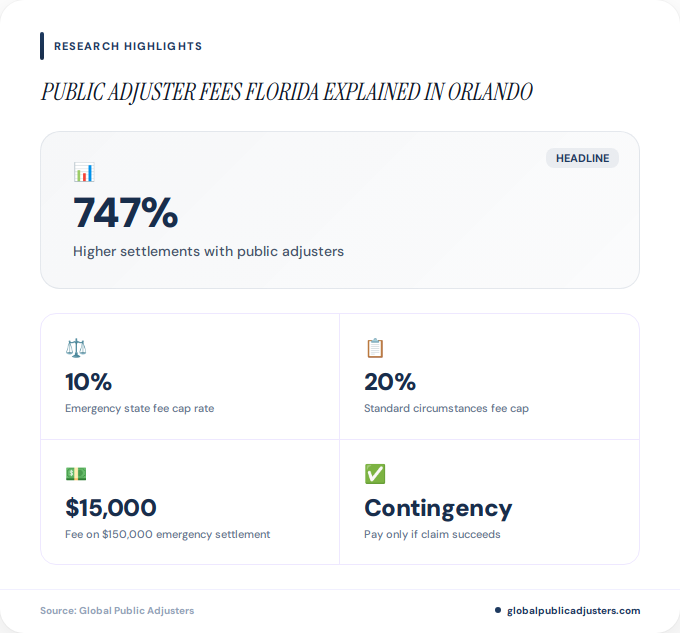

Public adjuster fees in Orlando, Florida are strictly regulated by state law, capped at10% of your claim settlement during a declared state of emergency(for one year) and20% under normal circumstances. These contingency fees mean you pay nothing upfront and only if your claim succeeds, with costs deducted from your final insurance payout.

When your Orlando home sustains damage from a hurricane, water leak, or fire, navigating insurance claims can feel overwhelming. Here’s a statistic that might surprise you:homeowners who hire public adjusters typically receive settlements 747% higher than those who handle claims alone, according to industry data. But what do public adjuster fees in Orlando actually cost, and are they worth the investment?

Understanding public adjuster fees Florida requirements is crucial before signing any contract. Whether you’re dealing with storm damage in Winter Park, water damage in Lake Nona, or fire damage in downtown Orlando, knowing exactly how much you’ll pay and what you’ll receive in return can make the difference between a fair settlement and leaving thousands on the table.

This comprehensive guide breaks down everything Orlando homeowners need to know aboutpublic adjuster fees in Florida, from state-mandated caps to real-world cost examples, so you can make an informed decision about protecting your property interests.

What Are Public Adjuster Fees in Florida?

Public adjuster fees in Florida operate on acontingency basis, meaning you pay nothing upfront and only pay if your claim successfully results in a settlement. This fee structure aligns the adjuster’s incentives with yours: the more they recover, the more they earn.

TheFlorida Department of Financial Services regulates all public adjuster feesunder Chapter 626 of Florida Statutes. These regulations protect Orlando homeowners from excessive charges while ensuring qualified professionals can earn fair compensation for their expertise.

Unlike some states with unregulated fee structures, Florida imposes strict percentage caps that vary based on whether a state of emergency has been declared. This is particularly relevant in Orlando, wherehurricane damage claimsfrequently trigger emergency declarations.

How Are Public Adjuster Fees Calculated in Orlando?

Public adjuster fees in Orlando are calculated as apercentage of your total insurance settlement, not a flat rate. The exact percentage depends on several factors, but Florida law sets clear maximum thresholds.

Here’s how the calculation typically works: If your Orlando property receives a $150,000 settlement for hurricane damage and your contract specifies a 10% fee (emergency rate), you would pay $15,000 to the public adjuster. If the fee is 20% (standard rate), you would pay $30,000.

| Settlement Amount | 10% Fee (Emergency) | 20% Fee (Standard) |

|---|---|---|

| $50,000 | $5,000 | $10,000 |

| $100,000 | $10,000 | $20,000 |

| $200,000 | $20,000 | $40,000 |

| $300,000 | $30,000 | $60,000 |

Importantly, fees only apply toproceeds collected after the contract date. If your insurance company already paid $25,000 before you hired a public adjuster, and the adjuster secures an additional $75,000, the fee applies only to the $75,000 additional recovery.

Forwater damage claims in Orlando, which often involve complex damage assessments and negotiations, this contingency structure ensures you only pay for results delivered.

What Do Florida Regulations Say About Public Adjuster Fees?

Florida law establishes some of the most consumer-protective public adjuster fee regulations in the United States. These rules apply uniformly across Orlando and the entire state, ensuring consistent protection regardless of which neighborhood you live in.

Thestandard fee cap is 20%of the total claim payment for both residential and commercial properties. This applies to typical claims filed under normal circumstances, such as roof damage from aging, plumbing failures, or isolated storm events not triggering emergency declarations.

However, when the Governor declares a state of emergency (common for hurricanes affecting Orlando), the fee capdrops to 10% for one full yearfrom the declaration date. After that year expires, fees revert to the 20% standard cap. This emergency provision was designed to protect homeowners during their most vulnerable periods.

Additional regulatory safeguards include:

- No fees on pre-contract payments:Adjusters cannot charge for insurance proceeds you received before signing their contract

- Reopened claim limits:For supplemental or reopened claims, fees cannot exceed 20% of the additional payment secured

- Contract rescission rights:Homeowners have specific rights to cancel contracts under certain conditions

- Solicitation restrictions:Adjusters may only contact potential clients Monday through Saturday, 8 a.m. to 8 p.m.

Contracts that exceed statutory fee limits are considered unlawful and unenforceable under Florida law. This means if a public adjuster tries to charge you 25% on a standard claim, that contract violates state regulations.

How Do Emergency Fees Differ From Standard Rates?

Understanding the distinction between emergency and standard fee structures is critical for Orlando homeowners, given the region’s exposure to hurricanes and tropical storms. The difference can mean thousands of dollars in your pocket.

Emergency Fee Structure (10% cap):Applies when the Governor declares a state of emergency affecting your area. This typically occurs for hurricanes, widespread flooding, or other catastrophic events. The 10% cap remains in effect for exactly one year from the emergency declaration date, regardless of when you file your claim during that period.

For example, if Hurricane season brings a major storm to Orlando in August 2026 with an emergency declaration, any claim related to that event filed through August 2027 would qualify for the 10% cap, even if you don’t hire a public adjuster until months later.

Standard Fee Structure (20% cap):Applies to all non-emergency claims, including isolated incidents like kitchen fires, burst pipes, or vandalism. It also applies to emergency-related claims filed more than one year after the declaration expires.

Tropical storm flooding

Declared disasters

Fee: 10% (1 year)

Water leaks

Vandalism

Fee: 20% maximum

Additional damages

Underpayment recovery

Fee: 20% on new amount

This dual structure means timing matters significantly. If you’re considering hiring a public adjuster in Orlando for storm-related damage, acting within the one-year emergency window can save you 10% of your total settlement.

Most reputable Orlando public adjusters will clearly explain which fee structure applies to your specific situation and provide written documentation in your contract. If you’re uncertain whether your claim qualifies for emergency rates, verify the Governor’s declaration dates through official state channels.

Are Public Adjuster Fees Worth It in Orlando?

The value proposition of hiring a public adjuster in Orlando depends on several factors: the complexity of your claim, the extent of damage, your insurance company’s initial offer, and your personal expertise in claims negotiation.

According tothe Florida Association of Public Insurance Adjusters (FAPIA), policyholders who work with public adjusters receive significantly higher settlements than those who negotiate alone. The expertise public adjusters bring in damage assessment, policy interpretation, and negotiation often results in settlements that more than offset their fees.

Consider this scenario: Your insurance company offers $80,000 for hurricane damage to your Lake Nona home. You hire a public adjuster at 10% (emergency rate), and through thorough documentation and negotiation, they secure a $180,000 settlement. Your net recovery after the $18,000 fee would be $162,000, compared to the original $80,000 offer. That’s a$82,000 net gainafter fees.

Public adjusters provide particular value in Orlando for:

- Complex damage assessments:Multiple systems affected, hidden damage, or structural issues requiring expert evaluation

- Large claims:High-value properties or extensive damage where settlements exceed $100,000

- Disputed claims:When insurers deny coverage or significantly undervalue damage

- Commercial properties:Business interruption claims, inventory losses, and complex commercial coverage

- Overwhelmed homeowners:Those lacking time, expertise, or emotional capacity to manage the claims process

However, for smaller, straightforward claims (under $10,000) with clear damage and cooperative insurers, the percentage fee might not justify the benefit. In these cases, working directly with your insurance company or seeking guidance fromexperienced public adjustersduring a free consultation might be sufficient.

The key is understanding what you’re paying for. Public adjusters handle documentation, damage inventory, loss estimation, policy review, negotiation, and follow-up. They navigate the technical language of insurance policies and advocate exclusively for your interests, unlikeinsurance company adjusters who represent the carrier.

Are There Hidden Costs Beyond the Percentage?

One of the most important consumer protections in Florida’s public adjuster regulations is the prohibition against hidden fees. Reputable public adjusters in Orlando operate transparently with the contingency percentage as their sole compensation.

What’s Included in the Standard Fee:The percentage fee covers all standard services including initial inspections, damage documentation, estimate preparation, policy analysis, claim filing, insurance company negotiations, and settlement follow-up. No additional charges should apply for these core services.

Potential Additional Costs (Rare):In certain complex situations, you might encounter separate charges for specialized services like engineering reports, environmental testing, or expert witness testimony. However, these must be explicitly outlined in your contract with your written consent before incurring the expense.

According toLouis Law Group’s analysis of Florida public adjuster contracts, legitimate adjusters never charge upfront fees, retainers, or consultation fees. If a public adjuster requests money before settling your claim, this is a major red flag.

You should also be aware that public adjuster fees are separate from attorney fees if you later decide to hire legal representation. Some complex or denied claims benefit from dual representation, but this means paying both the adjuster’s percentage (typically 10-20%) and the attorney’s contingency fee (usually 33-40%). This dual-fee scenario can reduce your net recovery, which is why some homeowners choose to work directly with attorneys on particularly contentious claims.

Always request a detailed, written contract that clearly specifies:

- The exact percentage fee and which rate cap applies (emergency vs. standard)

- What services are included in the base fee

- Any circumstances where additional costs might apply

- Payment terms and when fees are collected

- Your cancellation rights and any associated penalties

Forroof damage claimsor other specialized situations common in Orlando, confirm whether the adjuster works with independent contractors (like roofers or engineers) and who pays for those services.

How Do Public Adjuster Fees Compare to Other Options?

When facing an insurance claim in Orlando, you have several representation options, each with different fee structures and value propositions.

Self-Representation (DIY):Costs nothing but requires significant time investment and insurance expertise. Best for small, straightforward claims where the insurer offers fair initial settlements. Risk: potentially leaving significant money on the table due to lack of negotiation skills or overlooking covered damages.

Public Adjuster (10-20% contingency):No upfront costs, fees only on successful recovery. Adjusters handle the entire claims process from documentation through settlement. Best for medium to large claims, complex damage, or uncooperative insurers. The percentage-based fee structure aligns their incentives with maximizing your settlement.

Attorney Representation (33-40% contingency):Higher percentage fee but includes legal leverage and potential litigation. Necessary for denied claims, bad faith situations, or when insurers refuse reasonable settlements. Attorneys can file lawsuits and represent you in court, powers public adjusters don’t have.

Hybrid Approach:Some homeowners start with a public adjuster for claim preparation and negotiation, then add attorney representation if the insurer remains unreasonable. This can result in dual fees but may be necessary for maximum recovery on seriously disputed claims.

| Option | Fee Range | Best For |

|---|---|---|

| Self-Filing | $0 (time investment) | Small, clear claims under $10,000 |

| Public Adjuster | 10-20% contingency | Complex claims $25,000-$500,000+ |

| Attorney Only | 33-40% contingency | Denied claims, bad faith situations |

| Adjuster + Attorney | Combined fees vary | Highly disputed large claims |

The difference betweenpublic adjusters and insurance agentsis also crucial to understand. Insurance agents work for insurance companies and don’t charge policyholders directly, but they represent the carrier’s interests, not yours. Public adjusters work exclusively for you and are paid from your settlement.

For Orlando homeowners dealing with hurricane damage, the 10% emergency cap makes public adjusters particularly cost-effective compared to the 33%+ fees attorneys typically charge, while still providing professional representation throughout the claims process.

What Are the 2026 Legislative Changes to Public Adjuster Fees?

Florida’s 2026 legislative session brought important updates to public adjuster regulations, strengthening consumer protections while maintaining the existing fee structure that has served Orlando homeowners well.

Senate Bill 266, effective July 1, 2026, reaffirms the 10% emergency cap and 20% standard cap while adding new contract rescission protections. According to theofficial Senate Bill 266 analysis, the legislation clarifies homeowners’ rights to cancel public adjuster contracts under specific circumstances without penalty.

Key provisions of the 2026 updates include:

- Enhanced disclosure requirements:Public adjusters must provide clearer explanations of fee structures, including examples showing fees under both emergency and standard rates

- Improved contract transparency:Contracts must explicitly state which fee cap applies and under what circumstances fees might change

- Strengthened solicitation rules:Additional restrictions on when and how public adjusters can contact homeowners post-disaster

- Clearer rescission rights:Homeowners have expanded rights to cancel contracts within specific timeframes

House Bill 427 complements these changes by clarifying contract rescission procedures and ensuring homeowners understand their cancellation rights before signing. These bills emerged from post-Hurricane Ian experiences, where some homeowners felt pressured into contracts they didn’t fully understand.

Importantly, the 2026 legislation maintains the fundamental fee structure Orlando residents rely on:10% during emergencies, 20% otherwise. The changes focus on transparency and consumer education rather than altering the underlying economics of public adjuster services.

For Orlando homeowners hiring public adjusters in 2026 and beyond, these updates mean clearer contracts, better understanding of costs before signing, and stronger protections if you need to terminate the relationship. Always ensure your contract complies with current 2026 regulations before signing.

Key Takeaways: Public Adjuster Fees in Orlando, Florida

- Fee caps are strictly regulated:10% during declared emergencies (one year from declaration), 20% for standard claims, with no exceptions allowed under Florida law

- Contingency-only structure:No upfront costs, retainers, or consultation fees; you pay only if your claim succeeds, making professional representation accessible

- Fees apply only to new recovery:Public adjusters can only charge on settlement amounts secured after you sign their contract, not pre-existing payments

- Timing affects cost significantly:Filing hurricane or disaster-related claims within the one-year emergency window cuts fees in half compared to standard rates

- Hidden fees are prohibited:All services should be included in the percentage fee; any additional costs must be explicitly disclosed in writing beforehand

- 2026 regulations strengthen protections:New legislation enhances transparency, disclosure requirements, and contract rescission rights for Orlando homeowners

- Value often exceeds cost:Professional representation typically recovers significantly more than self-negotiation, with the settlement increase often far surpassing the percentage fee

People Also Ask

Can public adjusters charge upfront fees in Florida?

No, Florida law prohibits public adjusters from charging any upfront fees, retainers, or consultation costs. All legitimate public adjusters work on a contingency basis, meaning they are paid only from your successful insurance settlement.

What happens if my claim is denied and I hired a public adjuster?

If your claim is completely denied with no payment from the insurance company, you owe the public adjuster nothing. The contingency fee structure means adjusters only get paid when you receive a settlement, protecting you from financial loss on unsuccessful claims.

How long does the 10% emergency fee cap last in Orlando?

The 10% emergency fee cap remains in effect for exactly one year from the date the Governor declares a state of emergency. After that year expires, fees for new contracts revert to the standard 20% cap, even if the claim relates to the same disaster event.

Can I negotiate a lower fee with my public adjuster?

Yes, the 10% and 20% figures are maximum caps, not minimum requirements. Some public adjusters may negotiate lower percentages for particularly large claims or straightforward cases, though most maintain standard rates to ensure quality service.

Do I need a public adjuster if my insurance company seems cooperative?

Even with cooperative insurers, public adjusters often identify additional covered damages and secure higher settlements than policyholders negotiating alone. However, for small, straightforward claims with fair initial offers, professional representation may not be necessary.

Are public adjuster fees tax deductible in Florida?

Public adjuster fees may be tax deductible as a casualty loss expense in certain circumstances, but tax laws change frequently and vary by situation. Consult a tax professional to determine if your specific public adjuster fees qualify for deductions on your federal or state returns.

Frequently Asked Questions

What is the maximum a public adjuster can charge in Orlando, Florida?+

The maximum fee is 10% of your settlement during a declared state of emergency (for one year after declaration) and 20% for all other claims. These are legal caps established by Florida Statutes Chapter 626, and any contract exceeding these limits is unlawful and unenforceable.

When do I pay my public adjuster in Orlando?+

You pay your public adjuster only after receiving your insurance settlement check. The fee is typically deducted from your total payout before you receive the net proceeds, though payment timing should be clearly outlined in your contract.

Can I cancel my public adjuster contract in Florida?+

Yes, Florida law provides specific rescission rights allowing you to cancel public adjuster contracts under certain conditions. The 2026 legislative updates (SB 266 and HB 427) strengthened these cancellation protections, though specific terms vary by contract and timing.

How do public adjuster fees work on supplemental claims?+

For reopened or supplemental claims where you’re seeking additional payment on a previously settled claim, public adjusters can charge up to 20% of the new payment amount only. They cannot charge fees on the original settlement you already received.

What’s included in a public adjuster’s standard fee?+

The contingency percentage covers all standard services including damage inspection, documentation, loss inventory, estimate preparation, policy review, claim filing, negotiation with your insurance company, and settlement follow-up. Specialized services like engineering reports may incur separate charges if explicitly agreed upon in writing.

Should I hire a public adjuster or attorney for my Orlando insurance claim?+

Public adjusters (10-20% fees) are ideal for claim preparation and negotiation when insurers are engaged but offering inadequate settlements. Attorneys (33-40% fees) become necessary for denied claims, bad faith situations, or when litigation is required. Some complex cases benefit from both professionals working together.

How can I verify my public adjuster is licensed in Florida?+

All public adjusters must be licensed by the Florida Department of Financial Services. You can verify licenses, check complaint histories, and confirm credentials through the department’s online license search system before signing any contract.

Ready to Maximize Your Insurance Settlement in Orlando?

Understanding public adjuster fees is just the first step. If you’re facing an insurance claim in Orlando, whether from hurricane damage, water intrusion, fire loss, or any other covered event, professional representation can make a substantial difference in your final recovery.

The contingency fee structure means you risk nothing by getting expert assessment of your claim. With fees capped at 10-20% and only charged on successful settlements, hiring a qualified public adjuster aligns professional expertise with your financial interests.

Don’t leave money on the table or struggle through the complex claims process alone.Contact Global Public Adjusters todayfor a free consultation and learn exactly how much your claim could be worth with professional representation. Our team serves all of Orlando and surrounding communities, bringing decades of experience to every claim we handle.

Remember: insurance companies have teams of adjusters protecting their interests. Shouldn’t you have an expert protecting yours?