Roof Damage Claims and Public Adjusters in Florida: Your Complete 2026 Guide

Quick Answer

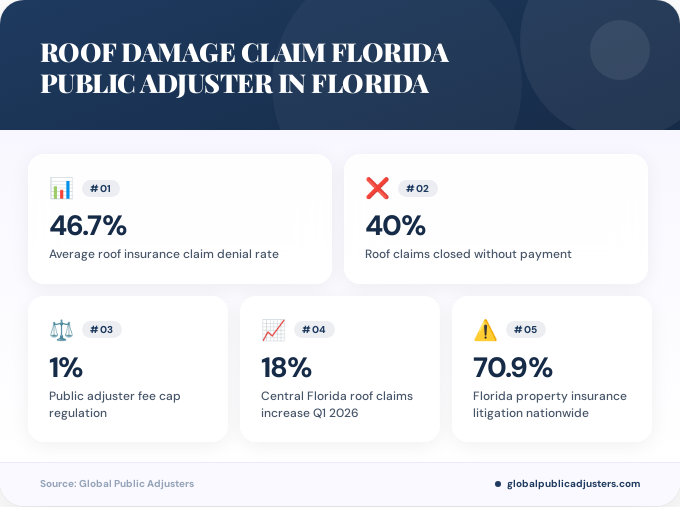

A public adjuster in Florida can help you navigate roof damage insurance claims by representing your interests against the insurer, with fees capped at 1% of the claim under state regulations. Florida homeowners face significant challenges, with over 40% of roof insurance claims closed without payment in 2024 and an average denial rate of 46.7%, making professional representation increasingly valuable for securing fair settlements.

Did you know thatFlorida accounts for roughly 14.9% of all property insurance claims filed nationwide but generates approximately 70.9% of the nation’s property insurance litigation? This staggering statistic reveals the contentious relationship between Florida homeowners and insurance companies, particularly when it comes to roof damage claims.

With Central Florida experiencing an18% increase in roof-related insurance claims in the first quarter of 2026, driven by early-season heat, aging roofs, and spring storm systems affecting Seminole, Orange, and Volusia counties, understanding the role of aroof damage claim Florida public adjusterhas never been more critical.

If you’re facing roof damage and anticipating a battle with your insurance company, this comprehensive guide will equip you with the knowledge you need to maximize your settlement and understand when professional representation becomes essential.

What Is Happening with Roof Insurance Claims in Florida?

The roof insurance claim crisis in Florida has reached unprecedented levels. In 2024, theaverage denial rate surged to approximately 46.7%, with over40% of roof insurance claims closed without payment. For context,76,428 homeowner claims were closed without payment statewide in 2023.

These numbers represent more than statistics. They represent homeowners left with damaged roofs, depleted savings, and mounting frustration with an insurance system designed to protect them.

The situation worsened significantly after Hurricane Milton, when41% of claims closed without payment were categorized as “below deductible.”This classification has become a strategic tool for insurers to deny otherwise valid claims, particularly given Florida’s high hurricane deductibles.

According toindustry experts tracking Florida roof replacement timelines, hurricane deductibles typically range from 2%, 5%, or 10% of home value. On a $400,000 home insured with a 5% hurricane deductible, the homeowner is responsible for the first $20,000 in damage, which can potentially exceed estimated repair costs.

This creates a catch-22 situation where homeowners pay premiums for coverage they can rarely access. Understanding these challenges is the first step toward protecting your investment and securing the compensation you deserve.

What Does a Public Adjuster Do for Roof Damage Claims?

A public adjuster serves as your advocate in the claims process, representing your interests rather than the insurance company’s bottom line. Unlike the insurance company’s adjuster, who works to minimize payouts, aroof damage claim Florida public adjusterworks exclusively for you.

Public adjusters provide comprehensive services including damage assessment, documentation preparation, claims filing, negotiation with insurers, and dispute resolution. They possess in-depth knowledge of Florida insurance law, policy language, and construction costs specific to the region.

Historical data from a statewide Florida study conducted between 2008 and 2009 showed thatclaimants with public adjusters averaged $9,379 per non-catastrophe claim, providing compelling evidence of the financial impact professional representation can have. Given inflation and rising construction costs, this differential has likely increased substantially in 2026.

AtGlobal Public Adjusters, we’ve seen countless cases where homeowners initially accepted lowball settlements, only to discover later that professional representation could have doubled or tripled their payout. The key is engaging a public adjuster early in the process, ideally before accepting any settlement offer.

How Long Does a Roof Insurance Claim Take in Florida?

Understanding the claims timeline helps set realistic expectations and identify potential delays that may signal bad faith tactics by insurers. The process typically unfolds across several distinct phases.

Days 1-2: Filing the Claim.You’ll call your insurance company’s claims hotline and provide a basic description of damage. Under Florida Statute 627.70131, insurers must acknowledge receipt within 14 days and begin investigation within 10 days, though in practice, most acknowledge within 24 to 48 hours.

Days 3-21: Adjuster Inspection.The insurance company assigns a field adjuster to inspect damage in person. During normal conditions, scheduling occurs within 7 to 14 days of filing. However,research on roof replacement insurance timelines in Floridashows that after major storms, adjuster availability becomes strained, and wait times can extend to 3 to 6 weeks.

Days 14-45: Claim Approval and Payment.Most claims are resolved in 14 to 45 days from the adjuster inspection. Under Florida law, insurers must either pay or deny claims within 90 days of filing. A common delay occurs when the adjuster’s scope is significantly lower than your contractor’s estimate; the supplement process can add 2 to 6 weeks to the timeline.

| Phase | Timeline | Common Delays |

|---|---|---|

| Filing | 1-2 days | High call volume after storms |

| Inspection | 7-21 days | Adjuster shortages, multiple inspections |

| Resolution | 14-45 days | Scope disputes, supplement requests |

When you work with aFlorida public adjuster, they monitor these timelines closely and escalate matters when insurers fail to meet their statutory obligations. Delays often indicate attempts to wear down claimants, hoping they’ll accept less favorable settlements.

What Are Public Adjuster Fees in Florida?

Florida has implemented strict regulations on public adjuster compensation to protect homeowners from excessive fees while allowing professional representation when disputes arise. Under current Florida law,a public adjuster may not charge more than 1% of the insurance claim.

This regulatory cap creates an important framework for understanding the cost-benefit analysis of hiring a public adjuster. If a public adjuster secures a $50,000 settlement, their maximum fee would be $500. If they negotiate a $200,000 payout, their fee caps at $2,000.

However, pricing structures can vary based on several factors including claim complexity, property size, extent of damage, and whether litigation becomes necessary. Some adjusters work on a contingency basis where you pay nothing unless they secure compensation, while others may require retainer fees for particularly complex cases.

The critical question isn’t whether you can afford to hire a public adjuster, but whether you can afford not to. Given that homeowners with professional representation historically receive settlements averaging significantly higher than those negotiating alone, the 1% fee represents a minimal investment for potentially substantial returns.

For detailed information about fee structures and what you can expect, consult our comprehensive guide onpublic adjuster fees in Florida.

Why Are So Many Roof Claims Being Denied?

Understanding the reasons behind Florida’s alarming denial rate helps you anticipate and counter insurer tactics. Several key factors contribute to the crisis.

High Hurricane Deductibles.As mentioned earlier, 41% of post-Hurricane Milton claims closed without payment were classified as “below deductible.” This strategy effectively denies coverage while technically maintaining policy compliance.

Wear and Tear Exclusions.Insurers frequently argue that roof damage results from normal aging rather than covered events. In Florida’s harsh climate, with intense UV exposure, tropical storms, and humidity, distinguishing between gradual deterioration and sudden damage becomes contentious.Legal experts specializing in roof damage insurance claimsnote that this distinction often requires forensic analysis and expert testimony.

Policy Misinterpretation.Insurance policies contain complex language designed to limit liability. Insurers may cite obscure clauses or apply restrictive interpretations that don’t align with reasonable policyholder expectations.

Insufficient Documentation.Many homeowners lack the expertise to properly document damage, photograph evidence, or present claims in ways that satisfy adjuster requirements. Missing documentation provides insurers with justification for denial.

Scope Disputes.Even when damage is acknowledged, disagreements over the extent of necessary repairs lead to underpayment or denial. An insurance adjuster might approve patching while your contractor insists the entire roof requires replacement.

According toindustry analysis of the public adjuster landscape in Florida, these denial tactics have become increasingly sophisticated as insurers face financial pressures and seek to minimize payouts.

When Should You Hire a Public Adjuster for Roof Damage?

Timing is crucial when engaging a public adjuster. Several scenarios signal that professional representation would benefit your claim substantially.

Immediately After Major Damage.If your roof sustains significant damage from a hurricane, tornado, or severe storm, hiring a public adjuster before filing your claim ensures proper documentation from the start. They’ll photograph damage, secure emergency repairs to prevent further loss, and compile comprehensive evidence.

When Your Claim Is Denied.A denial doesn’t mean the end of your options. Public adjusters excel at appealing denials, identifying policy provisions insurers overlooked, and presenting evidence that contradicts denial justifications.

After Receiving a Lowball Offer.If the insurance company’s settlement seems inadequate compared to contractor estimates, a public adjuster can review the offer, identify undervalued items, and negotiate for appropriate compensation.

When Disputes Arise Over Scope.Disagreements about whether repairs or replacement is necessary, what materials should be used, or how much work is required all benefit from expert intervention.

If Your Claim Exceeds $25,000-$50,000.For significant claims, the complexity and potential for insurer pushback increase substantially. Professional representation becomes particularly valuable as claim amounts rise.

Our article onwhen to hire a public adjuster in Jacksonvilleprovides additional insights into optimal timing and circumstances that warrant professional representation.

How Does the Roof Damage Claim Process Work?

Navigating the claims process requires understanding each stage and the strategies that maximize your settlement. Whether you’re working independently or with a public adjuster, following best practices is essential.

Step 1: Document the Damage.Immediately after discovering roof damage, photograph everything from multiple angles, both close-up and wide shots. Document interior damage including water stains, ceiling damage, and compromised belongings. Video documentation provides additional evidence of the scope and severity.

Step 2: Prevent Further Damage.Florida law requires policyholders to mitigate losses. This means securing tarps, removing standing water, and taking reasonable steps to prevent additional damage. Keep receipts for all emergency measures, as these costs are typically covered.

Step 3: Review Your Policy.Before filing, understand your coverage limits, deductibles, exclusions, and claim filing requirements. Pay particular attention to time limits for filing and any specific procedures your policy mandates.

Step 4: File Promptly.Report the claim to your insurance company as soon as possible. Delays can jeopardize coverage, particularly if subsequent events cause additional damage before you file.

Step 5: Prepare for the Inspection.When the insurance adjuster schedules their inspection, be present and point out all damage. If you’ve hired a public adjuster, they’ll conduct this interaction, ensuring nothing gets overlooked.

Step 6: Get Independent Estimates.Obtain detailed estimates from licensed roofing contractors. These provide leverage when negotiating with insurers and establish baseline costs for repairs or replacement.

Step 7: Review the Settlement Offer.Don’t immediately accept the first offer. Compare it against your contractor estimates, verify all damaged items are included, and ensure depreciation calculations are accurate.

Step 8: Negotiate or Appeal.If the offer is inadequate, present counterarguments supported by documentation, estimates, and policy language. This is where public adjusters demonstrate particular value, as they understand negotiation strategies and insurer psychology.

For comprehensive guidance on navigating this process, review our detailed article onhow to file a public adjuster claim in Orlando.

What Are Regional Considerations Across Florida?

Florida’s diverse climate and geography create regional variations in roof damage patterns and insurance considerations. Understanding your area’s specific challenges helps you prepare more effectively.

Central Florida.As noted earlier,Central Florida experienced an 18% surge in roof claims in early 2026, driven by early-season heat, aging infrastructure, and spring storm systems. Counties including Seminole, Orange, and Volusia face particular vulnerability due to rapid development and older housing stock.

South Florida.Miami, Fort Lauderdale, and surrounding areas contend with hurricane exposure, salt air corrosion, and high humidity. These factors accelerate roof deterioration and create frequent disputes over whether damage stems from covered events or environmental wear.

Coastal Areas.Beachfront properties face enhanced wind exposure, saltwater spray, and stricter building codes. Insurance premiums are higher, deductibles more substantial, and coverage restrictions more common.

North Florida.Jacksonville and surrounding areas experience different weather patterns including occasional freezing temperatures and less frequent but still significant tropical storm impacts. The region’s housing stock includes older homes with roofing materials that may not meet current wind resistance standards.

Tampa Bay.This region combines hurricane vulnerability with rapid population growth and varied construction quality. Understanding local building codes and insurance market dynamics is essential for successful claims.

Working with a local public adjuster who understands regional specifics provides significant advantages. They’re familiar with area contractors, typical damage patterns, local building codes, and regional insurer behaviors.

What Regulations Affect Roof Claims in Florida?

Florida’s regulatory environment for property insurance and roofing claims continues evolving in response to market pressures and consumer protection needs. Recent changes significantly impact how claims are handled.

TheFlorida Statute 627.70131establishes timelines for insurer responses, requiring acknowledgment within 14 days and investigation commencement within 10 days. Insurers must pay or deny claims within 90 days of filing, though extensions are possible with documented justification.

Recent regulatory changes have loosened some roof coverage standards. According to theFlorida Realtors Association reporting on new roof coverage rules, modifications to previous strict requirements may affect how insurers evaluate roof condition and coverage eligibility.

TheFlorida Building Codesets standards for roof construction, wind resistance, and materials. Claims often hinge on whether existing roofs met code at installation and whether repairs must bring the roof to current code compliance.

Matching Laws.Florida has specific regulations regarding roof material matching when partial repairs occur. UnderstandingFlorida’s roof matching laws for insurance claimshelps ensure you receive appropriate compensation for aesthetically consistent repairs.

Public Adjuster Licensing.Florida requires public adjusters to be licensed through the Department of Financial Services. When hiring a public adjuster, verify their credentials and license status. Our guide onpublic adjuster license requirements in Floridaexplains what qualifications professionals must meet.

Assignment of Benefits (AOB) Reforms.Florida has enacted restrictions on AOB agreements between contractors and homeowners to reduce abuse. Understanding current AOB rules prevents complications with your claim.

Key Takeaways

- Florida’s roof insurance claim denial rate reached 46.7% in 2024, with over 40% of claims closed without payment, making professional representation increasingly valuable.

- Public adjusters in Florida can charge a maximum of 1% of the claim amountunder state regulations, creating affordable access to professional advocacy that historically increases settlement amounts significantly.

- Hurricane deductibles ranging from 2% to 10% of home valueeffectively deny many otherwise valid claims by exceeding actual damage costs, particularly when insurers classify claims as “below deductible.”

- The typical claim timeline spans 14 to 90 days, with filing occurring in days 1-2, inspection in days 3-21, and resolution in days 14-45, though major storms can extend these periods substantially.

- Central Florida experienced an 18% surge in roof claims in early 2026, driven by aging infrastructure, early-season heat, and spring storm systems affecting Orange, Seminole, and Volusia counties.

- Hiring a public adjuster early in the process, ideally before accepting any settlement offer, maximizes your chances of securing fair compensation and avoiding common insurer tactics.

- Proper documentation, prompt filing, and understanding your policyare essential whether you work independently or with a public adjuster to navigate Florida’s complex insurance landscape.

People Also Ask

How much does a public adjuster cost in Florida for roof damage?

Public adjusters in Florida can charge a maximum of 1% of the insurance claim amount under state regulations. This means if your settlement is $100,000, the maximum fee would be $1,000, creating an affordable option for professional representation that typically increases settlement amounts substantially beyond the fee cost.

How long do I have to file a roof damage claim in Florida?

Most Florida homeowner insurance policies require claims to be filed within one to three years of the damage occurring, though specific timeframes vary by policy. It’s critical to report damage as soon as possible, as delays can jeopardize coverage and allow insurers to argue that subsequent events, rather than the original incident, caused the damage.

What percentage of roof damage is needed for insurance claim approval in Florida?

There’s no specific percentage threshold, as approval depends on whether damage results from a covered peril rather than normal wear and tear. Insurers evaluate the cause of damage, extent of deterioration, and whether repairs adequately address the problem or full replacement is necessary based on safety, code compliance, and material matching requirements.

Can I hire my own contractor if the insurance company sends one?

Yes, you have the right to hire your own contractor for estimates and repairs. In fact, obtaining independent contractor estimates provides leverage when negotiating with insurers and establishes baseline costs that may reveal inadequacies in the insurance company’s assessment or settlement offer.

What is the difference between a public adjuster and an insurance adjuster?

An insurance adjuster works for the insurance company and represents their interests in minimizing payouts, while a public adjuster works exclusively for you and represents your interests in maximizing your settlement. This fundamental difference in allegiance creates dramatically different outcomes in claim negotiations and final settlement amounts.

Will hiring a public adjuster delay my roof claim?

While involving a public adjuster may extend the initial negotiation period slightly, they often accelerate overall resolution by preventing the back-and-forth disputes that occur when homeowners accept inadequate offers and later discover they need to renegotiate. Professional adjusters expedite documentation, reduce insurer objections, and minimize unnecessary delays.

Frequently Asked Questions

What should I do immediately after discovering roof damage in Florida?+

Document the damage with photographs and videos from multiple angles, secure tarps or temporary repairs to prevent further damage, and contact your insurance company to report the claim within 24-48 hours. Keep receipts for all emergency measures, as these costs are typically covered under your policy’s loss mitigation provisions.

How do I know if my roof damage is covered by insurance in Florida?+

Coverage depends on whether damage resulted from a covered peril such as wind, hail, or falling objects rather than normal wear and tear or neglect. Review your policy’s declarations page, exclusions section, and covered perils list, or consult with a public adjuster who can evaluate your specific situation against policy language and Florida insurance regulations.

What is a hurricane deductible and how does it affect my roof claim?+

A hurricane deductible is typically 2%, 5%, or 10% of your home’s insured value and applies when damage occurs during officially declared hurricane events. On a $400,000 home with a 5% hurricane deductible, you’re responsible for the first $20,000 in repairs, which can effectively deny coverage if estimated damage falls below this threshold.

Can I appeal a denied roof insurance claim in Florida?+

Yes, you have multiple options including requesting a formal review by the insurance company, filing a complaint with the Florida Department of Financial Services, hiring a public adjuster to reassess and renegotiate, or pursuing litigation if necessary. Many initially denied claims are successfully overturned with proper documentation and professional representation.

What documentation do I need for a successful roof damage claim?+

Essential documentation includes photographs and videos of damage, contractor estimates for repairs or replacement, maintenance records showing proper upkeep, receipts for emergency repairs, weather reports confirming the damaging event, and correspondence with your insurance company. Comprehensive documentation significantly strengthens your negotiating position.

How much does roof replacement cost in Florida and will insurance cover it?+

Roof replacement costs in Florida vary widely from $8,000 to $50,000 or more depending on size, materials, complexity, and regional labor rates. Insurance covers replacement when damage from a covered peril necessitates it, though insurers often dispute whether full replacement is required or repairs are sufficient, making documentation and professional assessment critical.

Should I sign an Assignment of Benefits agreement with my roofing contractor?+

Exercise caution with Assignment of Benefits (AOB) agreements, as Florida has enacted restrictions due to past abuses. While AOB can simplify the process by allowing contractors to deal directly with insurers, it also transfers control of your claim and can lead to inflated costs or disputes. Consult with a public adjuster or attorney before signing any AOB agreement.