Public Adjuster vs Insurance Agent Difference in Florida: Your Complete 2026 Guide

Quick Answer

In Florida, a public adjuster works exclusively for policyholders to maximize insurance claim settlements (typically earning 5-15% of the payout), while an insurance agent sells policies, handles renewals, and initiates claims but does not negotiate settlements or advocate for the homeowner. Public adjusters assess damages and negotiate with insurers, while agents represent insurance companies and earn commissions on policy sales.

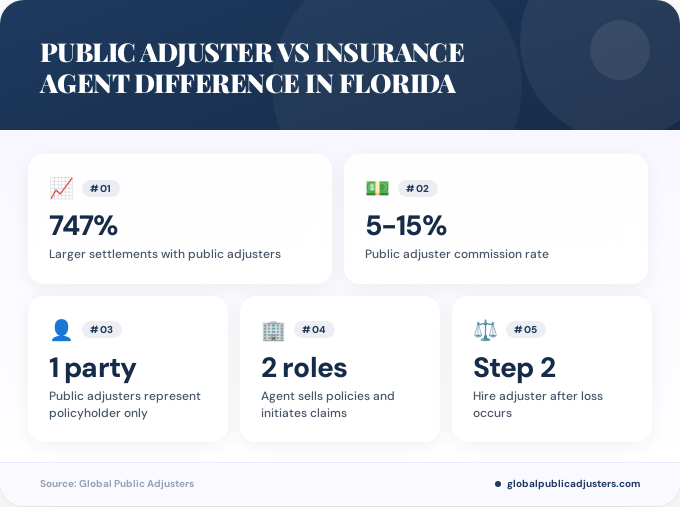

Did you know that Florida policyholders who hire public adjusters secure settlementsup to 747% largerthan initial insurer offers? In a state where hurricanes, tropical storms, and severe weather events regularly devastate properties from Miami to Jacksonville, understanding the public adjuster vs insurance agent difference in Florida can mean the difference between a fair settlement and a financial catastrophe.

With Florida’s unique insurance landscape, frequent post-loss underwriting practices, and complex policy provisions, knowing when to work with an insurance agent versus hiring a public adjuster is crucial for every property owner. This comprehensive guide breaks down the critical distinctions, roles, and strategic considerations for navigating insurance claims in the Sunshine State.

What Is the Primary Difference Between a Public Adjuster and an Insurance Agent in Florida?

The fundamental difference between a public adjuster and an insurance agent in Florida centers on who they represent and when they get involved in your insurance journey.Insurance agents sell insurance policies, help you select coverage, process renewals, and initiate claims, but they do not negotiate settlement amounts or assess damage on your behalf.

Public adjusters are licensed professionals hired by policyholdersafter a loss occurs to evaluate damages, interpret policy language, document claims, and negotiate directly with insurance companies for maximum settlement amounts. As explained byFlorida public adjuster professionals, this distinction is critical because agents work for insurance companies while public adjusters work exclusively for you.

Many Florida homeowners confuse public adjusters with insurance company adjusters (also called staff adjusters or independent adjusters), who are hired by insurers to evaluate claims and minimize payouts. Unlike these company representatives,public adjustershave a fiduciary duty to maximize your settlement.

| Aspect | Public Adjuster | Insurance Agent |

|---|---|---|

| Primary Role | Negotiates claims, assesses damages, maximizes policyholder payout | Sells policies, advises on coverage, assists with policy changes and renewals |

| Who They Represent | Exclusively the policyholder | Insurance company (or multiple via commissions) |

| Claims Involvement | Full: policy review, damage inspection, settlement negotiation | Limited: initiates claim filing, no settlement negotiation |

What Are the Specific Roles and Responsibilities of Each Professional?

Insurance agents in Floridaserve primarily as sales and service professionals. They help you understand coverage options, explain policy terms, recommend appropriate coverage limits, and facilitate policy purchases. Agents can be captive (representing one insurance company) or independent (representing multiple carriers).

When a loss occurs, your agent can help you initiate the claims process by notifying the insurance company and providing basic guidance. However, their involvement typically ends there. They do not assess the extent of damages, calculate replacement costs, or negotiate settlement amounts on your behalf.

Public adjusters in Floridaprovide comprehensive claim management services after a loss. Their responsibilities include conducting thorough damage assessments, documenting all losses with photographs and detailed inventories, reviewing policy language to identify covered damages, preparing detailed claim estimates, and negotiating with insurance company adjusters to secure fair settlements.

According toinsurance claims experts, public adjusters excel at identifying hidden damages that company adjusters often overlook, such as structural issues behind walls, mold growth after water damage, or code upgrade requirements following hurricanes in areas like Tampa, Fort Lauderdale, and Orlando.

Who Do Public Adjusters and Insurance Agents Actually Work For?

This question reveals the most critical distinction in the public adjuster vs insurance agent difference in Florida.Insurance agents work for insurance companies, earning commissions on policies they sell and renew. Even independent agents who represent multiple carriers are compensated by insurers, not policyholders.

This creates an inherent conflict of interest when claims arise. While agents may genuinely want to help their clients, their business relationship is fundamentally with the insurance company. They cannot negotiate against the company that pays their commissions.

Public adjusters work exclusively for policyholders, with no ties to insurance companies. As noted byFlorida claims professionals, this independence allows them to aggressively advocate for maximum settlements without conflicting loyalties. Their compensation comes directly from the policyholder, typically as a percentage of the settlement amount.

This alignment of incentives means public adjusters are motivated to secure the highest possible settlement. The more they recover for you, the more they earn, creating a partnership focused on maximizing your claim value.

When Should Florida Homeowners Hire a Public Adjuster vs Working With Their Agent?

Work with your insurance agentwhen you are shopping for new coverage, reviewing policy options, updating coverage limits, adding endorsements, or asking general policy questions. Agents are valuable resources for understanding what types of coverage you need before a loss occurs, particularly given Florida’s unique risks like hurricane deductibles and flood insurance requirements.

Your agent should also be your first contact to initiate a claim, as this starts the official process and creates a record with your insurance company. However, this is where many Florida homeowners make a costly mistake by assuming their agent will handle the rest.

Hire a public adjusterimmediately after any significant loss, particularly for hurricane damage, wind damage, water damage, fire damage, or theft involving substantial property damage. According to industry data, claims involving losses exceeding $10,000 to $25,000 typically benefit significantly from public adjuster representation.

Public adjusters are especially critical in Florida for hurricane claims involving Citizens Property Insurance Corporation, Universal Property & Casualty Insurance, and other carriers known for aggressive claim denial tactics and post-loss underwriting practices. If your claim is denied, undervalued, or delayed, a public adjuster can reassess the situation and fight for proper compensation.

How Does Compensation Differ Between Public Adjusters and Insurance Agents?

Insurance agentsearn their income through commissions on policy sales and renewals, typically ranging from 5% to 20% of the premium amount depending on the policy type and carrier. These commissions are built into your premium cost and paid by the insurance company, so you do not write a separate check to your agent.

Agents may also receive bonuses, contingent commissions based on overall book performance, and renewal commissions for policies that continue year after year. This structure incentivizes agents to sell policies and maintain customer relationships but does not reward them for claim advocacy.

Public adjusters in Floridawork on a contingency fee basis, typically charging between5% and 15% of the final settlement amount. The exact percentage depends on the claim complexity, size, and whether legal action becomes necessary. Florida law regulates these fees, with different caps applying based on timing and circumstances.

This contingency structure means you pay nothing upfront, and the public adjuster only earns compensation if they successfully recover settlement funds. For example, if a public adjuster charges 10% and secures a $150,000 settlement on your hurricane damage claim, their fee would be $15,000, leaving you with $135,000.

Given that policyholders using public adjusters secure settlementsaveraging 19.4% higherthan unassisted claims (and up to 747% higher in many cases), the net recovery after fees typically far exceeds what homeowners would receive handling claims alone or relying solely on agent assistance.

What Florida-Specific Factors Make This Difference Critical?

Florida’s insurance market presents unique challenges that make understanding the public adjuster vs insurance agent difference in Florida absolutely essential for property owners. The state experiences more hurricanes, tropical storms, and severe weather events than any other U.S. state, creating a high-volume, high-stakes claims environment.

Post-loss underwritingis a particularly problematic practice in Florida, where insurers like Citizens Insurance and others conduct credit checks, property inspections, and policy reviews after a claim is filed, looking for reasons to deny coverage or cancel policies. Public adjusters help policyholders navigate these tactics and protect their rights.

Florida’s complex insurance regulatory environment includes special provisions for hurricane deductibles, windstorm coverage exclusions, sinkhole coverage requirements, and flood insurance coordination. Agents can explain these provisions when selling policies, but public adjusters know how to apply them when fighting for maximum claim settlements.

Areas like Miami-Dade County, Broward County, Palm Beach County, Hillsborough County (Tampa), and coastal communities throughout Florida face elevated insurance rates and coverage restrictions. When major losses occur in these high-risk areas, having a public adjuster who understands local building codes, repair costs, and policy nuances becomes invaluable.

How Do Settlement Outcomes Compare With and Without a Public Adjuster in Florida?

The statistical evidence overwhelmingly demonstrates the value of public adjuster representation in Florida insurance claims. According to 2026 industry data,policyholders using public adjusters secure settlements up to 747% larger than initial insurer offers, with an average increase of 19.4% over unassisted claims.

These dramatic improvements result from several factors. Public adjusters conduct more thorough damage assessments, identifying hidden damages that company adjusters miss or deliberately undervalue. They understand policy language nuances and coverage triggers that maximize claim values under complex Florida insurance contracts.

| Claim Type | Without Public Adjuster | With Public Adjuster |

|---|---|---|

| Hurricane Damage | $45,000 to $75,000 typical initial offer | $85,000 to $225,000 negotiated settlement |

| Water Damage | $12,000 to $28,000 typical initial offer | $25,000 to $65,000 negotiated settlement |

| Fire Damage | $35,000 to $95,000 typical initial offer | $75,000 to $250,000+ negotiated settlement |

Public adjusters also prevent common mistakes that reduce claim values, such as accepting quick settlement offers before all damages are discovered, missing filing deadlines, or failing to document losses properly. As detailed byFlorida insurance claim experts, these professional advocates understand the intricate provisions within Florida insurance policies that companies exploit to minimize payouts.

Perhaps most importantly, public adjusters handle the extensive documentation, communication, and negotiation processes that overwhelm most homeowners, particularly when they are simultaneously dealing with property repairs, temporary housing, and recovery stress following major losses.

Key Takeaways

- Insurance agents sell policies and initiate claims but do not negotiate settlements, while public adjusters advocate exclusively for policyholders to maximize claim payouts.

- Public adjusters in Florida typically charge 5% to 15% of the settlementon a contingency basis, meaning no upfront costs and payment only upon successful recovery.

- Florida policyholders using public adjusters receive settlements averaging 19.4% higherthan unassisted claims, with increases up to 747% in many cases.

- Hire a public adjuster for significant lossesexceeding $10,000 to $25,000, hurricane damage, denied claims, or disputes with insurers like Citizens Insurance.

- Florida’s unique insurance challenges, including post-loss underwriting, hurricane deductibles, and aggressive claim denial tactics, make public adjuster expertise particularly valuable.

- Agents work for insurance companies and earn commissions on sales, creating inherent conflicts when claims arise, while public adjusters work solely for you.

- Time is critical in Florida insurance claims, particularly following hurricanes and tropical storms when claim volumes surge and insurers face financial pressure to minimize payouts.

People Also Ask

Can an insurance agent also be a public adjuster in Florida?

No, Florida law prohibits individuals from serving simultaneously as both an insurance agent and a public adjuster due to inherent conflicts of interest. Agents represent insurers while public adjusters represent policyholders, creating incompatible duties that would compromise both roles.

Do I need both an insurance agent and a public adjuster?

Yes, they serve different purposes at different times. Your insurance agent helps you purchase appropriate coverage and initiates claims when losses occur, while a public adjuster handles the damage assessment, documentation, and settlement negotiation after a claim is filed to maximize your recovery.

Will hiring a public adjuster upset my insurance company?

Insurance companies may prefer dealing directly with policyholders, but hiring a public adjuster is your legal right and cannot be held against you. Professional public adjusters maintain working relationships with all major carriers and negotiate claims professionally without damaging your coverage or insurability.

What is the difference between a public adjuster and a company adjuster?

Company adjusters (also called staff or independent adjusters) work for insurance companies to evaluate claims and protect the insurer’s financial interests by minimizing payouts. Public adjusters work exclusively for policyholders to maximize settlements, creating directly opposing roles in the claims process.

When should I contact a public adjuster after a loss in Florida?

Contact a public adjuster immediately after experiencing significant property damage, ideally within 24 to 48 hours. Early involvement allows them to document damages before evidence disappears, prevent settlement mistakes, and establish proper claim values from the beginning of the process.

Are public adjuster fees worth it in Florida?

Absolutely, with statistics showing settlement increases averaging 19.4% and often reaching 747% higher than initial offers, the net recovery after public adjuster fees typically far exceeds what homeowners receive handling claims independently. For significant claims, the expertise and advocacy easily justify the contingency fee.

Frequently Asked Questions

How much does a public adjuster cost in Florida?+

Public adjusters in Florida typically charge between 5% and 15% of the final settlement amount on a contingency basis. The exact percentage depends on claim complexity, size, timing, and whether litigation becomes necessary. Florida law regulates these fees to protect consumers, and you pay nothing unless the adjuster successfully recovers settlement funds on your behalf.

Can I switch to a public adjuster after my claim has already started?+

Yes, you can hire a public adjuster at any point during the claims process, even after initial damage assessments or settlement offers. Many Florida homeowners engage public adjusters after receiving unsatisfactory initial offers or experiencing claim denials. Earlier involvement typically produces better results, but experienced adjusters can still add substantial value to ongoing claims.

What credentials should I look for in a Florida public adjuster?+

Verify that any public adjuster holds a valid Florida public adjuster license through the Florida Department of Financial Services. Look for experience with your specific loss type (hurricane, water, fire), local market knowledge, professional certifications, positive client reviews, and transparent fee agreements. Reputable adjusters provide references and clearly explain their process and costs.

Will my insurance agent help me if I hire a public adjuster?+

Your insurance agent can still answer policy questions and facilitate communication with the insurance company, but once you hire a public adjuster, most direct claim negotiations and documentation will be handled by the adjuster. This division of labor works well, with agents providing policy information and public adjusters managing claim strategy and settlement negotiations.

How long does the claims process take with a public adjuster in Florida?+

The timeline varies significantly based on claim complexity, damage extent, and insurer responsiveness. Simple claims may resolve within 30 to 90 days, while complex hurricane damage claims can take 6 to 12 months or longer. Public adjusters typically expedite the process by ensuring complete documentation and aggressive follow-up, though they prioritize maximum settlement over speed.

What types of property damage claims do public adjusters handle in Florida?+

Florida public adjusters handle virtually all property damage types, including hurricane and windstorm damage, water damage from plumbing failures or storms, fire and smoke damage, theft and vandalism, sinkhole damage, tornado damage, and business interruption claims. They represent both residential and commercial property owners across all claim types and sizes.

Can a public adjuster help if my Florida insurance claim was denied?+

Yes, public adjusters frequently help overturn claim denials by re-evaluating damages, identifying coverage that insurers overlooked, providing additional documentation, and leveraging their expertise in Florida insurance law. They can also coordinate with attorneys if legal action becomes necessary, though many denials are successfully reversed through professional adjustment alone.