Public Adjuster vs Insurance Company in Florida: Understanding the Critical Differences in 2026

Quick Answer

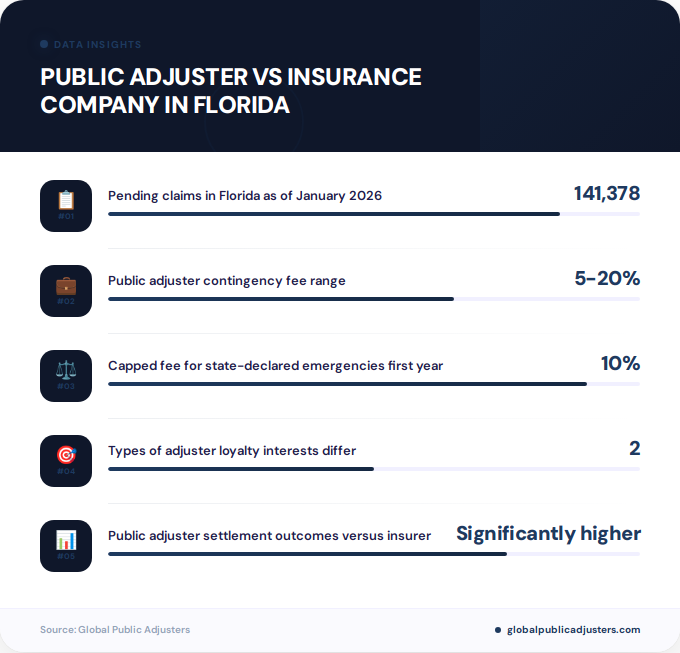

Public adjusters in Florida work exclusively for policyholders to maximize claim settlements, while insurance company adjusters represent the insurer’s financial interests and typically minimize payouts. With141,378 pending claimsstatewide as of January 2026, public adjusters often secure significantly higher settlements through expert negotiation and comprehensive damage documentation.

When disaster strikes your Florida property, understanding the difference between a public adjuster and an insurance company adjuster can mean thousands of dollars in your settlement. With Florida’s property insurance market managing141,378 pending claimsas of January 2026, the choice of representation has never been more critical.

The insurance landscape in Florida remains notoriously challenging for homeowners. From Miami to Tampa, Orlando to Jacksonville, property owners face increasing premiums, carrier instability, and claims denials. This volatile environment creates a fundamental question: whose side is your adjuster really on?

AtGlobal Public Adjusters, we’ve witnessed firsthand how professional representation transforms claim outcomes across the Sunshine State.

What Is the Fundamental Difference Between Public Adjusters and Insurance Company Adjusters?

The core distinction between a public adjuster vs insurance company in Florida centers on loyalty and fiduciary responsibility. Public adjusters work exclusively for policyholders, maintaining afiduciary dutyto maximize settlements within policy limits. They handle every aspect of your claim from initial documentation through final negotiation.

Insurance company adjusters, conversely, represent the insurance carrier’s financial interests. Whether they’re staff adjusters employed directly by companies like Citizens, State Farm FL, or independent contractors, their primary obligation is to the insurer, not the policyholder.

| Aspect | Public Adjuster | Insurance Company Adjuster |

|---|---|---|

| Loyalty | Fiduciary duty to policyholder; maximizes settlement | Duty to insurer; minimizes payouts |

| Payment | Contingency fee (5-20% of settlement) | Salaried or fixed contractor fee |

| Responsibility | Full claim management and policyholder advocacy | Initial assessment and settlement offer |

This distinction becomes particularly critical in Florida’s high-risk property insurance environment, where carriers likeCitizens, State Farm FL, and Slide hold the heaviest claim inventories. Insurance company adjusters work under pressure to close claims quickly and cheaply, while public adjusters invest the time necessary for thorough damage assessment.

How Does Payment Structure Differ Between Public Adjusters and Insurance Company Adjusters in Florida?

Payment models reveal the fundamental alignment of interests in the public adjuster vs insurance company in Florida equation. Public adjusters operate on acontingency fee basis, typically ranging from 5-20% of the final settlement amount. If they don’t secure a recovery for you, they don’t get paid.

Florida law specifically regulates these fees to protect consumers. For claims related to state-declared emergencies,public adjuster fees are capped at 10% for the first year, rising to 20% after one year from the declaration date. This structure ensures public adjusters remain motivated to maximize your settlement throughout the process.

Insurance company adjusters, by contrast, receive salaries or fixed contractor payments regardless of claim outcomes. Many work under quotas or performance metrics that incentivize low settlements and quick closures. This creates an inherent conflict of interest when evaluating property damage across Florida communities from Fort Lauderdale to Tallahassee.

The contingency fee structure aligns the public adjuster’s success directly with the policyholder’s recovery. This creates a powerful incentive to document every aspect of damage and negotiate aggressively, something salaried insurance adjusters have no motivation to do.

Why Does Florida’s Insurance Market Make Public Adjusters Essential in 2026?

Florida’s property insurance market remains in unprecedented turmoil, making professional representation more valuable than ever. The state faces severe carrier instability, with Praetorian Insurance leading cancellations at a staggering11.19% rate, meaning one in nine policyholders received cancellation notices in January 2026 alone.

The numbers tell a compelling story about the need for public adjusters when dealing with insurance company adjusters in Florida:

- 141,378 pending claimsstatewide as of January 2026, concentrated among high-volume carriers

- 9,865 policy nonrenewalsby Praetorian in January 2026, creating rushed claim closures

- $16.0 billion market sizefor Florida’s third-party administrators and claims adjusters in 2026

- Alternative dispute resolution dominating with2,294 mediation casesand1,792 appraisal casesin January 2026

These market conditions create pressure on insurance company adjusters to minimize payouts.New litigation decreased 40% and pending litigation fell 47%as carriers shifted to alternative dispute resolution, often disadvantaging unrepresented policyholders.

WithFlorida’s claims adjustment industry valued at $16.0 billion, the resources available to insurance companies far exceed what individual homeowners can marshal without professional representation.

What Role Does Each Adjuster Type Play in the Claims Process?

Understanding the practical differences in daily responsibilities illuminates the public adjuster vs insurance company in Florida debate. Public adjusters provide comprehensive claim management from start to finish, including damage assessment, policy interpretation, documentation, contractor coordination, and all communications with the insurance carrier.

They conduct detailed inspections using specialized equipment, photograph and catalog damage extensively, prepare room-by-room estimates, and negotiate directly with insurance company adjusters on your behalf. Public adjusters also handle all required paperwork, meet deadlines, and escalate to appraisal or mediation when necessary.

Insurance company adjusters typically conduct a single initial inspection, prepare a settlement offer based on their assessment, and handle communications primarily through the insurer’s systems. Their focus centers on closing claims efficiently rather than maximizing policyholder recovery.

In practice, insurance company adjusters often miss hidden damage, undervalue repair costs, apply improper depreciation, or deny coverage for items that should be included. Public adjusters identify these discrepancies and advocate for proper compensation.

How Do Settlement Outcomes Compare Between Public Adjusters and Insurance Company Adjusters?

The financial impact of choosing between a public adjuster vs insurance company in Florida becomes clear when examining settlement data. Studies of Florida hurricane claims reveal that public adjusters secured average payments of$22,266following the 2004 hurricane season, representing a19.4% increasecompared to claims handled without professional representation.

This settlement advantage exists across all claim types in Florida, from water damage in coastal properties to hurricane damage throughout the state. Public adjusters leverage several advantages to achieve higher settlements:

- Comprehensive damage documentation that insurance company adjusters often overlook

- Expert knowledge of policy language and coverage interpretations

- Established relationships with contractors for accurate repair estimates

- Experience with alternative dispute resolution processes like appraisal and mediation

- Understanding of depreciation schedules and replacement cost value calculations

The1,792 appraisal casesfiled in January 2026 demonstrate how public adjusters successfully challenge insurance company undervaluations through Florida’s dispute resolution mechanisms. Appraisal proves particularly effective against carriers with high denial rates.

When you consider thatpublic adjusters often secure settlements significantly higher than initial insurance company offers, their contingency fees represent excellent value for policyholders across Tampa, Miami, and throughout Florida.

When Should Florida Homeowners Hire a Public Adjuster?

The decision between accepting an insurance company adjuster’s assessment or hiring a public adjuster depends on several factors specific to Florida property claims. Consider professional representation when your claim involves significant damage exceeding $10,000, complex policy interpretation questions, or damage to multiple property areas.

Public adjusters prove particularly valuable when dealing with carriers experiencing financial stress or high nonrenewal rates, when initial settlement offers seem inadequate, or when the insurance company denies coverage for items you believe should be included. If your property sustained damage from hurricanes, flooding, or other disasters common across Florida’s diverse climate zones, professional representation often pays for itself many times over.

Time constraints also favor hiring a public adjuster early in the claims process. With insurance companies pushing claims through alternative dispute resolution and focusing on rapid closures, having someone who understands the full scope of your policy rights becomes essential.

Florida homeowners should be especially vigilant when their carrier appears on the high-cancellation lists, as these companies often accelerate claim closures to reduce exposure before policy terminations. Public adjusters can ensure your claim receives proper attention even amid carrier instability.

Key Takeaways

- Fundamental loyalty difference:Public adjusters maintain fiduciary duty to policyholders and maximize settlements, while insurance company adjusters represent insurers and minimize payouts across Florida claims.

- Payment structure alignment:Public adjusters work on contingency (5-20% of settlement, capped at 10% initially for emergency-declared claims), ensuring their success depends on yours, unlike salaried insurance adjusters.

- Market conditions favor representation:With 141,378 pending claims statewide and major carriers like Praetorian canceling 11.19% of policies, professional advocacy is increasingly essential in Florida’s volatile insurance market.

- Significant settlement differences:Public adjusters historically secure average settlements 19.4% higher than unrepresented claims, with documented average payments of $22,266 in major Florida disaster claims.

- Comprehensive vs. limited service:Public adjusters provide full claim management including documentation, negotiation, and dispute resolution, while insurance company adjusters typically conduct single inspections and initial offers.

- Alternative dispute resolution expertise:With 2,294 mediation and 1,792 appraisal cases in January 2026, public adjusters navigate Florida’s complex ADR landscape effectively against carrier undervaluations.

- Critical timing considerations:Hiring public adjusters early in the claims process ensures comprehensive damage documentation before carriers push for quick closures or policy terminations.

People Also Ask

Is it worth hiring a public adjuster in Florida?

Hiring a public adjuster in Florida is typically worth it for claims exceeding $10,000, as they historically secure settlements 19.4% higher than unrepresented claims. With 141,378 pending claims statewide and significant carrier instability, professional representation often recovers far more than the contingency fee costs.

What is the difference between a public adjuster and an insurance adjuster?

Public adjusters work exclusively for policyholders with fiduciary duty to maximize settlements, while insurance adjusters represent the carrier’s interests and focus on minimizing payouts. Public adjusters handle comprehensive claim management on contingency, whereas insurance adjusters receive salaries regardless of settlement amounts.

How much does a public adjuster charge in Florida?

Florida public adjusters typically charge 5-20% of the final settlement on a contingency basis. For state-declared emergencies, fees are capped at 10% during the first year, rising to 20% after one year from the declaration date, with no recovery meaning no fee.

Can insurance companies deny claims if you use a public adjuster?

Insurance companies cannot legally deny claims solely because you hired a public adjuster. In fact, professional representation often prevents wrongful denials by ensuring comprehensive documentation and proper policy interpretation throughout the Florida claims process.

When should I hire a public adjuster for my Florida insurance claim?

Hire a public adjuster immediately after significant damage occurs, ideally before filing your claim or within days of the incident. Early engagement ensures comprehensive damage documentation and prevents accepting inadequate initial settlement offers from insurance company adjusters.

Do public adjusters work with all insurance companies in Florida?

Yes, public adjusters work with all insurance carriers operating in Florida, including Citizens, State Farm FL, Slide, and all private insurers. They maintain professional relationships and understand carrier-specific procedures, which proves particularly valuable with the 141,378 pending claims across multiple carriers.

Frequently Asked Questions

What are the biggest mistakes Florida homeowners make when dealing with insurance adjusters?+

The most common mistakes include accepting the first settlement offer without negotiation, signing releases before understanding full damage scope, and failing to document damage comprehensively before repairs begin. Many homeowners also miss critical policy deadlines or underestimate damage severity, particularly with water intrusion or structural issues common in Florida’s climate.

Can I switch from an insurance company adjuster to a public adjuster mid-claim in Florida?+

Yes, Florida homeowners can hire a public adjuster at any point during the claims process, even after receiving an initial settlement offer from the insurance company adjuster. Many policyholders engage public adjusters after realizing their initial settlement inadequately covers damages, and public adjusters can reopen negotiations or pursue appraisal to secure proper compensation.

How long does the claims process take with a public adjuster versus an insurance company adjuster in Florida?+

While insurance company adjusters often push for quick closures within 30-60 days, public adjusters typically invest 60-180 days for thorough documentation and negotiation, resulting in substantially higher settlements. With 2,294 mediation and 1,792 appraisal cases in January 2026, alternative dispute resolution may extend timelines but significantly increases recovery amounts for Florida policyholders.

What credentials should I look for when hiring a public adjuster in Florida?+

Verify Florida Department of Financial Services licensing, look for experience with your specific damage type (hurricane, water, fire), and confirm expertise with your insurance carrier. Request references from recent Florida claims, verify professional liability insurance coverage, and ensure they understand current state regulations including the 10% emergency fee cap.

Will hiring a public adjuster affect my insurance rates or future coverage in Florida?+

No, hiring a public adjuster cannot legally affect your insurance rates or future coverage eligibility in Florida. Insurance companies cannot discriminate against policyholders who choose professional representation, and with carriers like Praetorian already canceling 11.19% of policies due to market conditions, advocacy protects your interests without additional risk.

What types of property damage claims benefit most from public adjusters in Florida?+

Hurricane damage, water intrusion, mold remediation, fire and smoke damage, and roof failures benefit most from public adjuster representation in Florida. Complex claims involving multiple damage types, structural issues, or business interruption require the comprehensive documentation and policy expertise that public adjusters provide, especially given Florida’s unique coastal weather patterns and construction challenges.

How do public adjusters handle claims with carriers experiencing financial difficulties in Florida?+

Public adjusters expedite claims with financially stressed carriers, prioritize critical damage documentation, and escalate to Florida’s guaranty fund when necessary. With carriers like Praetorian issuing 9,865 nonrenewals in January 2026, public adjusters ensure claims close properly before policy terminations and protect policyholders’ rights throughout carrier transitions or insolvencies.