Public Adjuster vs Insurance Company in Florida: The Complete 2026 Guide to Maximizing Your Claim Settlement

Quick Answer

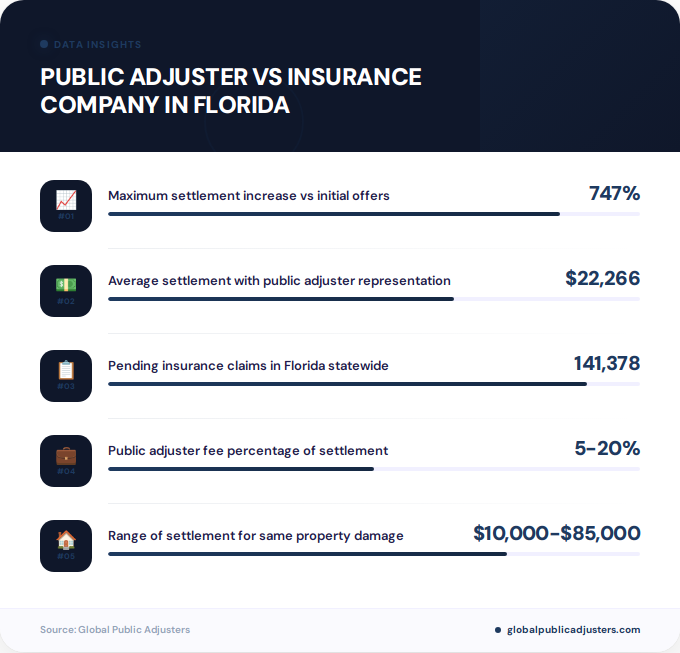

A public adjuster works exclusively for you to maximize your insurance settlement, while an insurance company adjuster represents the insurer’s interests to minimize payouts. In Florida, policyholders using public adjusters receive settlements up to 747% larger than initial offers, with an average increase of 19.4% to $22,266 per claim versus $18,659 without representation.

When hurricane winds tear through Tampa, Miami, or Jacksonville, leaving thousands of Florida homeowners scrambling to file insurance claims, a critical decision emerges: Should you accept the insurance company adjuster’s assessment, or hire your own advocate? The answer could mean the difference between receiving $10,000 and nearly $85,000 for the same damage.

Florida’s volatile property insurance landscape has created unprecedented opportunities and challenges for policyholders navigating the claims process. With141,378 pending claimsstatewide as of January 2026 and massive carrier instability affecting thousands of policies, understanding the distinction between a public adjuster and an insurance company adjuster has never been more crucial.

What Is the Difference Between a Public Adjuster and an Insurance Company Adjuster in Florida?

The fundamental distinction between a public adjuster and an insurance company adjuster in Florida centers on who they represent and whose interests they serve. This difference directly impacts how much money ends up in your pocket after a claim.

Insurance company adjustersare employees or contractors hired by your insurance carrier. Their primary responsibility is to evaluate your claim and determine the minimum payment the insurer is legally obligated to make. They receive salaries or fees from the insurance company, creating an inherent incentive to minimize claim payouts and protect the insurer’s bottom line.

Public adjusterswork exclusively for you, the policyholder. Licensed by the Florida Department of Financial Services, they advocate on your behalf to maximize your settlement. Public adjusters typically charge5-20% of the final settlement amount, aligning their financial incentives directly with yours. The more you recover, the more they earn.

The legal structure reinforces this divide. Insurance company adjusters owe their fiduciary duty to the carrier, whilepublic adjusters in Floridaoperate under strict licensing requirements that mandate loyalty to policyholders. This creates opposing negotiating dynamics in virtually every claim scenario.

How Do Public Adjusters and Insurance Company Adjusters Work?

The claims process reveals stark operational differences between these two types of adjusters. Understanding their methodologies helps explain why settlement outcomes vary so dramatically.

Insurance company adjustersfollow a standardized protocol designed to expedite claims while controlling costs. They conduct damage assessments using proprietary software that often undervalues replacement costs. Their timelines are driven by corporate efficiency metrics rather than thorough investigation. Most receive performance evaluations based partly on how much money they save the company across multiple claims.

Public adjustersdeploy a comprehensive advocacy strategy. They document every aspect of damage with detailed photography, hire independent contractors for repair estimates, and review your policy line by line to identify all covered losses. In Florida’s complex insurance environment, this thoroughness frequently uncovers additional damages or coverage provisions that company adjusters overlook or deliberately ignore.

| Aspect | Insurance Company Adjuster | Public Adjuster |

|---|---|---|

| Represents | Insurance Company | Policyholder |

| Compensation | Salary from insurer | 5-20% of settlement |

| Goal | Minimize payout | Maximize settlement |

The negotiation phase further distinguishes their approaches. Company adjusters operate within predetermined settlement ranges approved by supervisors. Public adjusters leverage Florida’salternative dispute resolution mechanisms, including the2,294 mediations and 1,792 appraisalsinvoked statewide in January 2026, to challenge lowball offers aggressively.

Why Does Florida’s Insurance Market Make Public Adjusters Essential?

Florida’s property insurance landscape presents unique challenges that amplify the value proposition of hiring a public adjuster. The state’s market dynamics in 2026 reveal systemic issues that disadvantage unrepresented policyholders.

TheFlorida Office of Insurance Regulation reportsshow concerning instability patterns.Praetorian Insurance led cancellations at 11.19%, meaning one in nine policyholders faced policy termination. The carrier also executed9,865 nonrenewalsin January 2026 alone. This volatility creates pressure on adjusters to resolve claims quickly and cheaply before policies lapse.

The claims industry itself has ballooned into a$16.0 billion marketin Florida as of 2026, ranking seventh in state GDP contribution at 5.2%. This massive financial ecosystem incentivizes cost containment strategies that often work against individual policyholders seeking fair settlements.

Florida’s recent insurance reforms, while stabilizing some market aspects, have also created new complexity.17 new carriers entered the marketsince reforms passed, but these newcomers lack established claims handling track records. Public adjusters provide essential expertise navigating unfamiliar carrier procedures and identifying patterns of underpayment that haven’t yet drawn regulatory scrutiny.

The litigation environment adds another layer. While new and pending litigation dropped40% and 47%respectively by late 2025, historical data reveals that over a decade,71% of $51 billion in insurer payoutswent to attorneys and public adjusters combined, exceeding amounts paid directly to policyholders. This statistic underscores how adversarial the claims process has become in Florida.

What Is the Financial Impact of Hiring a Public Adjuster in Florida?

The financial mathematics of hiring a public adjuster versus accepting an insurance company adjuster’s offer reveals compelling economics for Florida policyholders. Real data demonstrates consistent patterns of substantially increased settlements.

Acomprehensive Bankrate analysisfound policyholders using public adjusters received an average settlement of$22,266 compared to $18,659 without representation, representing a19.4% increase. Applied to Florida’s average claim scenarios, this difference easily covers the public adjuster’s fee while putting thousands more in the policyholder’s pocket.

The premium value emerges in complex claims. The landmark Florida study documenting747% larger settlementsinvolved scenarios where insurance company adjusters initially offered $10,000 for damage that public adjusters successfully argued was worth nearly $85,000. While not every claim sees such dramatic increases, the pattern of significant underpayment by company adjusters appears consistent across claim types.

Your Net Recovery:$18,659

Adjuster Cost:$0

Your Net Recovery:~$19,926

Adjuster Fee (10%):$2,227

Percentage Gain:6.8%

Plus: Better documentation

Even accounting for the public adjuster’s fee (typically 10% for straightforward claims, higher for complex litigation), policyholders net more money. Beyond raw dollars, public adjusters provide documentation that protects against future disputes and ensures repairs meet code requirements, potentially saving tens of thousands in future problems.

The return on investment grows substantially in high-value properties or catastrophic losses. For a $500,000 hurricane claim, a 19.4% increase means an additional$97,000 in settlement. After paying a 10% fee on the total, the homeowner still nets approximately$72,000 morethan accepting the company adjuster’s initial offer.

When Should Florida Homeowners Hire a Public Adjuster?

Timing considerations significantly impact the effectiveness of public adjuster representation in Florida. Certain claim characteristics and carrier behaviors signal when professional advocacy becomes essential.

Complex structural damagerepresents the clearest indicator. Hurricane damage affecting multiple building systems, roof replacement combined with interior water intrusion, or foundation issues require specialized knowledge that most homeowners lack. Public adjusters bring construction expertise and contractor networks to accurately document and value these multifaceted claims.

Lowball initial offerswarrant immediate consultation. If your insurance company adjuster’s settlement seems drastically lower than contractor estimates or your research suggests, a public adjuster can reassess the damage and negotiate upward. The 747% settlement increases documented in Florida studies typically involve scenarios where company adjusters dramatically undervalued claims.

Claim denials or delaysrepresent another critical trigger point. Florida regulations require timely claim handling, but carriers frequently use delay tactics hoping policyholders will accept inadequate settlements or abandon claims. Public adjusters escalate stalled claims through formal dispute resolution channels.

Carrier-specific patterns should inform your decision. TheFlorida Insurance Stability Unitdata showsCitizens Property Insurance carried 6,936 open lawsuitsin January 2026, with 44% of litigated claims closing favorably for consumers. State Farm Florida showed even better outcomes at84% favorable resolutions across 3,416 suits.

These statistics suggest systemic underpayment patterns at specific carriers. If you hold coverage with carriers showing high litigation rates and favorable consumer outcomes, hiring a public adjuster proactively often prevents the need for eventual litigation while securing comparable settlement increases.

Which Florida Insurance Carriers Show the Highest Denial Patterns?

Understanding carrier-specific behavior patterns helps Florida homeowners anticipate challenges and determine when public adjuster representation becomes strategically necessary. January 2026 data reveals significant disparities in how carriers handle claims.

Citizens Property Insurancedominates the problematic carrier landscape with6,936 open lawsuits, the highest in Florida. However, its44% favorable outcome ratefor consumers in litigation suggests the carrier frequently underpays claims that are successfully challenged. This pattern makes public adjuster representation particularly valuable for Citizens policyholders.

Praetorian Insurancepresents unique risks beyond claim handling. The carrier’s11.19% cancellation rateand9,865 nonrenewalsin January 2026 create urgency for policyholders to file and resolve claims before policy termination. Public adjusters can accelerate claim processing and ensure documentation protects your interests if the carrier exits the market.

Several carriers demonstrate exceptional consumer favorability rates that warrant attention.Security First Insuranceshows a remarkable95% favorable outcome ratein litigated claims, the highest in Florida.TypTap Insurance at 89%andSlide Insurance at 88%similarly favor consumers in disputes.

These high favorability rates suggest these carriers routinely make initial lowball offers but settle significantly higher when challenged. Public adjusters familiar with these patterns can leverage the carriers’ litigation avoidance strategies to negotiate better settlements without reaching the courtroom.

The alternative dispute resolution statistics provide additional insight. With2,294 mediations and 1,792 appraisalsinvoked statewide in January 2026, Florida’s formal dispute channels see heavy use.Appraisal processes excel for valuation disputes, with63% of all litigated claimsultimately closing favorably for consumers when properly documented and advocated.

Public adjusters strategically employ these mechanisms against carriers known for undervaluation, turning Florida’s regulatory framework into leverage for higher settlements without the time and expense of full litigation.

Key Takeaways

- Public adjusters work for you exclusively, while insurance company adjusters represent the carrier’s interests to minimize payouts. This fundamental difference drives settlement outcomes in Florida’s adversarial claims environment.

- Florida policyholders using public adjusters receive settlements up to 747% largerthan initial insurance company offers, with average increases of 19.4% translating to $3,607 more per claim even after adjuster fees.

- Florida’s insurance market shows significant instabilitywith 141,378 pending claims, 11.19% cancellation rates at some carriers, and $16.0 billion in claims administration activity creating systematic incentives for underpayment.

- Specific carriers demonstrate patterns of underpayment, including Citizens (6,936 open lawsuits, 44% favorable consumer outcomes), State Farm Florida (3,416 suits, 84% favorable), and Security First (95% favorable rate when challenged).

- Alternative dispute resolution mechanisms provide leverage, with 2,294 mediations and 1,792 appraisals invoked in January 2026, and 63% of litigated claims closing favorably for consumers who properly document and advocate.

- Timing matters significantly, particularly for complex structural damage, lowball offers, claim denials, and policies with unstable carriers executing high nonrenewal rates.

- The financial mathematics favor hiring public adjustersfor most substantial claims, as settlement increases consistently exceed the 5-20% fee structure, netting thousands more for policyholders.

People Also Ask

How much does a public adjuster cost in Florida?

Public adjusters in Florida typically charge between 5-20% of the final settlement amount, with most charging around 10% for standard claims. Complex claims requiring litigation or extensive negotiation may command higher percentages, but the fee structure ensures the adjuster only earns when you receive payment.

Can I switch from an insurance adjuster to a public adjuster mid-claim?

Yes, Florida homeowners can hire a public adjuster at any point during the claims process, even after receiving an initial settlement offer from the insurance company adjuster. Many policyholders hire public adjusters specifically after receiving lowball offers, and the 747% settlement increases documented in Florida often result from these mid-process interventions.

Do public adjusters handle all types of insurance claims in Florida?

Florida public adjusters handle property insurance claims including hurricane damage, fire, water damage, theft, and other covered perils affecting residential and commercial properties. They do not handle auto insurance, health insurance, or life insurance claims, focusing exclusively on property and casualty matters where structural damage assessment expertise adds value.

How long does it take a public adjuster to settle a claim in Florida?

Settlement timelines vary based on claim complexity, but Florida public adjusters typically resolve straightforward claims within 30-90 days, while complex cases involving litigation or appraisal may take 6-12 months. The thoroughness that extends timelines often produces dramatically higher settlements, with the 19.4% average increase representing thousands of additional dollars worth the wait.

Will hiring a public adjuster hurt my relationship with my insurance company?

Your relationship with your insurance carrier is purely contractual, and Florida law explicitly protects your right to hire a public adjuster without penalty. Carriers cannot retaliate, cancel policies, or deny future claims because you hired professional representation. The 141,378 pending claims statewide demonstrate that claim disputes are standard business in Florida’s insurance market.

What credentials should I look for in a Florida public adjuster?

Verify the public adjuster holds an active Florida license through the Department of Financial Services, carries professional liability insurance, and demonstrates experience with your specific claim type. References from recent clients, familiarity with alternative dispute resolution mechanisms like the 2,294 mediations and 1,792 appraisals conducted in January 2026, and knowledge of carrier-specific patterns indicate quality representation.

Frequently Asked Questions

What is the main advantage of hiring a public adjuster over using the insurance company adjuster in Florida?+

The primary advantage is significantly higher settlements, with Florida studies showing policyholders receive up to 747% more than initial offers when represented by public adjusters. Beyond dollars, public adjusters provide comprehensive damage documentation, contractor oversight, and policy expertise that protects your long-term interests in ways company adjusters deliberately avoid.

Does hiring a public adjuster guarantee a higher settlement in Florida?+

While no outcome is guaranteed, data shows consistent settlement increases averaging 19.4% higher when using public adjusters. The fee structure, where adjusters earn 5-20% of settlements, aligns their incentives with maximizing your payout. Most reputable public adjusters offer free claim reviews and only proceed if they believe they can increase your settlement beyond their fee.

Can I negotiate the public adjuster fee percentage in Florida?+

Yes, public adjuster fees are negotiable within Florida’s regulatory framework. Straightforward claims with clear damage documentation may warrant lower percentages (5-10%), while complex cases requiring extensive investigation, expert testimony, or litigation justifiably command higher fees (15-20%). Always get the fee structure in writing before signing a representation agreement.

What happens if my insurance company refuses to pay even with a public adjuster?+

Public adjusters escalate disputes through Florida’s alternative dispute resolution mechanisms, including the 2,294 mediations and 1,792 appraisals invoked in January 2026. If these fail, they work with attorneys to pursue litigation, leveraging data showing 63% of litigated claims close favorably for consumers. The comprehensive documentation they provide from the start strengthens your legal position.

How do I verify a public adjuster is licensed in Florida?+

Check the Florida Department of Financial Services website, which maintains a searchable database of all licensed public adjusters. Verify the license is active, check for any disciplinary actions, and confirm the adjuster carries required professional liability insurance. Legitimate adjusters readily provide their license number and welcome verification.

Should I hire a public adjuster for small claims in Florida?+

For claims under $5,000, the economics often favor handling it yourself or accepting the insurance company adjuster’s offer, as the public adjuster fee may consume most of any settlement increase. However, for claims above $10,000, especially involving structural damage or carrier patterns of underpayment, public adjuster representation typically delivers substantial net benefits.

What documentation should I gather before meeting with a public adjuster?+

Collect your insurance policy, photos of all damage, contractor estimates, correspondence with the insurance company, and any initial settlement offers. Public adjusters review these materials during free consultations to assess whether they can increase your settlement beyond their fee, saving everyone time if the existing offer is already maximized.