Public Adjuster Florida: Your Complete Guide to Navigating Insurance Claims in the Sunshine State

Quick Answer

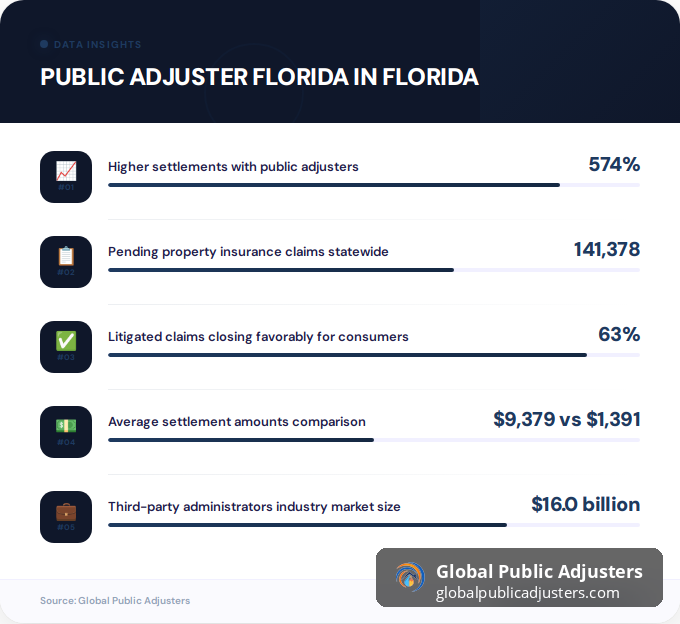

A public adjuster Florida is a licensed professional who works exclusively for policyholders to maximize insurance claim settlements, with data showing adjusters secure settlements averaging574% higher($9,379 vs. $1,391) on non-catastrophe claims compared to unrepresented claimants. In January 2026 alone, Florida recorded141,378 pending property insurance claimsstatewide, creating significant demand for expert claim advocacy across Miami, Tampa, Orlando, and beyond.

When disaster strikes your Florida property, whether from hurricanes battering Miami’s coastline, water damage flooding Tampa homes, or fire destroying Orlando businesses, navigating insurance claims can feel overwhelming. Here’s a startling fact:63% of litigated property claims in Florida close favorably for consumers, but only when they have proper advocacy. This is where a public adjuster Florida becomes invaluable.

With63,826 new property insurance claims opened in January 2026 aloneand a staggering141,378 claims pendingacross the state, Florida’s property insurance landscape remains one of the most complex in the nation. Understanding how public adjusters work and when to hire one can mean the difference between a fair settlement and financial devastation.

What Is a Public Adjuster in Florida?

A public adjuster Florida is a licensed insurance professional who works exclusively for policyholders, not insurance companies. Unlike company adjusters who represent the insurer’s interests, public adjusters advocate solely for property owners to ensure they receive the maximum settlement they’re entitled to under their policy.

These professionals handle every aspect of the claims process, from initial damage assessment and policy review to documentation, negotiation, and final settlement. In Florida’s volatile insurance market, where policy cancellations reached241,710in January 2026 and nonrenewals hit59,610, having an expert who understands policy language and insurer tactics is critical.

The third-party administrators and insurance claims adjusters industry in Florida reached a market size of$16.0 billionin 2026, reflecting the massive demand for professional claims assistance. Public adjusters must complete extensive training, pass state examinations, and maintain continuing education to keep their licenses active through the Florida Department of Financial Services.

Why Hire a Public Adjuster Florida for Your Insurance Claim?

The data speaks volumes about the value public adjusters bring to Florida policyholders. Historical statistics reveal thatnon-catastrophe claims averaged $9,379 with public adjusters versus just $1,391 without, representing a stunning574% differencein settlement amounts.

For hurricane claims, the disparity grows even larger. During the 2005 hurricane season, claims handled by public adjusters averaged$17,187 compared to $2,029for unrepresented policyholders, a747% difference. These figures demonstrate that insurance companies often undervalue claims when policyholders navigate the process alone.

Florida’s unique insurance challenges make professional representation even more critical. The state experiences frequent hurricanes, severe thunderstorms, flooding, and sinkholes, all while maintaining some of the nation’s highest insurance premiums. AJanuary 2026 market reportshows appraisal was invoked1,792 timesin just one month, indicating significant disputes between insurers and policyholders.

How Much Does a Public Adjuster Cost in Florida?

Florida law strictly regulates public adjuster compensation through a tiered fee structure designed to protect consumers. Fornon-emergency claims, public adjusters can charge up to20% of the settlement amount. This percentage-based fee means you pay nothing upfront and only compensate the adjuster if they successfully secure a settlement.

During state-of-emergency situations (such as hurricanes), different caps apply. Public adjusters can charge up to10% of the settlementfor claims filed within the first year of the declared emergency. After one year, the cap increases to20%. These regulations, implemented after 2011 reforms, aim to prevent price gouging while maintaining access to professional representation.

The average public adjuster salary in Florida stood at$48,531 annually(or $23.33 per hour) as of March 2026, though experienced adjusters handling high-value commercial claims or complex hurricane damage often earn significantly more through their commission-based structure.

| Claim Type | Maximum Fee | Timeline |

|---|---|---|

| Non-Emergency Claims | 20% | Any time |

| Emergency Claims (First Year) | 10% | Within 1 year of emergency declaration |

| Emergency Claims (After First Year) | 20% | After 1 year of emergency declaration |

Florida Insurance Market Statistics 2026: What You Need to Know

The Florida property insurance market in 2026 presents both challenges and opportunities for policyholders. According tocomprehensive market analysis, January 2026 saw302,082 new policies writtenagainst241,710 cancellations, creating a net positive but revealing a concerning1.98% monthly churn rate.

Certain carriers show particularly high cancellation rates. Praetorian Insurance topped the list with an11.19% cancellation rateand9,865 policies nonrenewed, suggesting significant dissatisfaction or financial instability. For homeowners working withGlobal Public Adjusters, monitoring carrier stability becomes crucial when filing claims.

Citizens Property Insurance, Florida’s insurer of last resort, reduced its policy count to under400,000(the lowest in 14 years) following market reforms. This reduction reflects efforts to stabilize the market but also means fewer options for high-risk properties in coastal areas like Miami Beach, Naples, and the Florida Keys.

Closed Claims:68,750

Pending Claims:141,378

Appraisals Invoked:1,792

Cancellations:241,710

Nonrenewals:59,610

Monthly Churn:1.98%

Industry Size:$16.0 billion

Avg PA Salary:$48,531

Without PA:$1,391

Difference:574%

When Should You Hire a Public Adjuster Florida?

Timing matters significantly when engaging a public adjuster. The ideal moment is immediately after discovering property damage but before filing your insurance claim. Early involvement allows the adjuster to document damage comprehensively, prevent further deterioration, and establish the full scope of loss before the insurance company’s adjuster arrives.

Consider hiring a public adjuster Florida if your claim involves significant damage (typically over $10,000), complex coverage questions, or if you’ve already received a lowball settlement offer. Properties in Florida’s hurricane-prone regions like Fort Myers, Jacksonville, and the Panhandle particularly benefit from expert representation given the frequency of catastrophic weather events.

You should also engage a public adjuster if your insurer denies your claim, delays payment beyond reasonable timeframes, or if you lack the time, expertise, or emotional capacity to navigate the claims process. Business owners facing commercial property damage often find public adjusters essential for maintaining operations while pursuing complex claims. The approach is similar to how businesses mightchoose specialized professionalsfor other critical business functions.

How Are Public Adjusters Licensed and Regulated in Florida?

Florida maintains some of the nation’s strictest licensing requirements for public adjusters, overseen by the Florida Department of Financial Services. Prospective adjusters must complete pre-licensing education, pass a comprehensive state examination, submit to background checks, and maintain errors and omissions insurance.

The state’s rigorous oversight results in relatively low complaint rates compared to the volume of claims handled. According toindustry analysis, Florida’s licensing standards exceed those of many other states, reflecting ethical standards that protect consumers while allowing adjusters to effectively advocate for policyholders.

Licensed public adjusters must complete continuing education requirements to maintain their credentials, ensuring they stay current on policy changes, building codes, damage assessment techniques, and legal developments. The Department of Financial Services publishes a searchable database where consumers can verify an adjuster’s license status, check for disciplinary actions, and confirm their standing.

How to Choose the Right Public Adjuster in Florida

Selecting the right public adjuster requires careful vetting. Start by verifying their Florida license through the Department of Financial Services website. Check their experience with your specific type of damage (hurricane, flood, fire, sinkhole) and property type (residential, commercial, condominium).

Request references from recent clients with similar claims and ask about their communication style, responsiveness, and settlement results. Reputable adjusters will provide detailed written contracts that comply with Florida’s disclosure requirements, including their license number, firm name, loss description, and compensation percentage in clearly readable font.

Beware of adjusters who solicit immediately after disasters (this may violate regulations), promise specific settlement amounts (outcomes depend on policy terms and damage), or pressure you to sign contracts without thorough review. The best public adjusters take time to explain the process, answer questions, and demonstrate deep knowledge of Florida’s insurance landscape, much like howlocal professionalsin other fields prioritize transparency and expertise.

What Are the Latest Florida Public Adjuster Regulations?

Florida enacted significant regulatory changes in 2026 that impact both public adjusters and consumers.Senate Bill 266, effective July 1, 2026, mandates detailed contract disclosures including firm name, license number, loss description, and compensation percentage displayed in18-point font. Public adjusters must also provide written loss estimates to clients.

The Department of Financial Services gained authority to discipline adjusters who violate these disclosure requirements, ensuring transparency in consumer contracts. These provisions aim to prevent confusion and ensure policyholders fully understand their agreements before signing.

Senate Bill 427, also effective July 1, 2026, provides special protections for vulnerable adults. The legislation allows vulnerable adults to cancel public adjuster contracts at any time without penalty and authorizes the Department of Financial Services to impose fines up to$5,000 per actfor adjusters who improperly solicit this protected population.

These legislative changes reflect Florida’s commitment to balancing consumer protection with access to professional claims advocacy. According toinsurance industry analysis, the reforms maintain Florida’s position as both a highly regulated market and one where public adjusters play a crucial role in securing fair settlements.

Key Takeaways

- Public adjusters in Florida significantly increase settlements:Data shows non-catastrophe claims average $9,379 with representation versus $1,391 without, a 574% difference that can mean tens of thousands of dollars for property owners.

- Florida’s 2026 insurance market remains volatile:With 141,378 pending claims, 241,710 policy cancellations, and a 1.98% monthly churn rate, professional advocacy is more critical than ever for navigating complex claims.

- Fee caps protect consumers:Non-emergency claims are limited to 20% of settlement, while state-of-emergency claims cap at 10% initially (rising to 20% after one year), ensuring affordable access to professional representation.

- Recent legislation strengthens consumer protections:SB 266 and SB 427 (effective July 1, 2026) mandate detailed contract disclosures, protect vulnerable adults, and authorize fines up to $5,000 per violation for non-compliant adjusters.

- Litigation success favors represented policyholders:63% of litigated property claims close favorably for consumers, with appraisal invoked 1,792 times in January 2026 alone, demonstrating the value of expert advocacy.

- License verification is essential:Florida maintains strict licensing standards through the Department of Financial Services, and consumers should always verify an adjuster’s credentials before signing contracts.

- Early engagement maximizes results:Hiring a public adjuster immediately after damage occurs (before filing claims) allows comprehensive documentation and prevents common pitfalls that reduce settlement amounts.

People Also Ask

Yes, data shows public adjusters increase non-catastrophe settlements by 574% ($9,379 vs. $1,391) and hurricane claims by 747% ($17,187 vs. $2,029) compared to unrepresented policyholders. Given Florida’s complex insurance market and 141,378 pending claims statewide, professional representation typically pays for itself many times over.

A public adjuster Florida works exclusively for policyholders to document property damage, interpret policy coverage, prepare detailed claim submissions, negotiate with insurance companies, and secure maximum settlements. They handle all aspects of the claims process from initial assessment through final payment.

There’s no specific timeline for public adjusters, but Florida law requires insurance companies to acknowledge claims within 14 days and settle or deny within 90 days. Public adjusters work within these frameworks to expedite settlements, with 68,750 claims closed in January 2026 alone.

Absolutely, many policyholders hire public adjusters after receiving claim denials or lowball offers. Adjusters can review denial letters, identify coverage issues, gather additional documentation, and negotiate with insurers or pursue appraisal/litigation if necessary, contributing to the 63% favorable consumer outcome rate in litigated claims.

Yes, Florida public adjusters typically work on contingency, charging a percentage (up to 20% for non-emergency claims, 10-20% for emergency claims) of the final settlement. You pay nothing upfront and only compensate the adjuster if they successfully secure payment from your insurer.

Florida public adjusters handle hurricane damage, wind and hail, flooding, water damage, fire, smoke damage, theft, vandalism, sinkholes, and mold claims. They work on residential, commercial, and condominium properties across all regions from Miami to Pensacola.

Frequently Asked Questions

Visit the Florida Department of Financial Services website and use their license search tool to verify any public adjuster’s credentials. You can check their license status, view any disciplinary actions, and confirm they’re authorized to practice in Florida.

As of July 1, 2026, contracts must include the firm name, adjuster’s license number, detailed loss description, compensation percentage in 18-point font, and written loss estimates. The contract should also specify services provided, timeline expectations, and cancellation terms.

Most Florida public adjuster contracts include a cancellation period (typically 3-5 days) after signing. Vulnerable adults have unlimited cancellation rights without penalty under SB 427 (effective July 1, 2026), providing extra protection for this population.

The timeline varies based on damage complexity and insurer responsiveness, but Florida law requires insurers to acknowledge claims within 14 days and settle or deny within 90 days. Public adjusters work to expedite this process, though complex claims may take several months, especially when appraisal or litigation is necessary.

No, you have the legal right to hire a public adjuster, and insurers cannot penalize you or cancel your policy for doing so. In fact, insurers are accustomed to working with public adjusters and often take claims more seriously when professional representation is involved.

Insurance company adjusters work for the insurer and aim to minimize claim payouts, while public adjusters work exclusively for policyholders to maximize settlements. This fundamental difference in loyalty explains why settlements with public adjusters average 574% higher than those without representation.

For claims under $10,000, you may be able to handle the process yourself, though a public adjuster can still help ensure full compensation. For claims exceeding $10,000 or involving coverage disputes, professional representation typically provides significant value that outweighs the fee percentage.