Public Adjuster Fees Florida Explained in Jacksonville: 2026 Complete Guide

Quick Answer

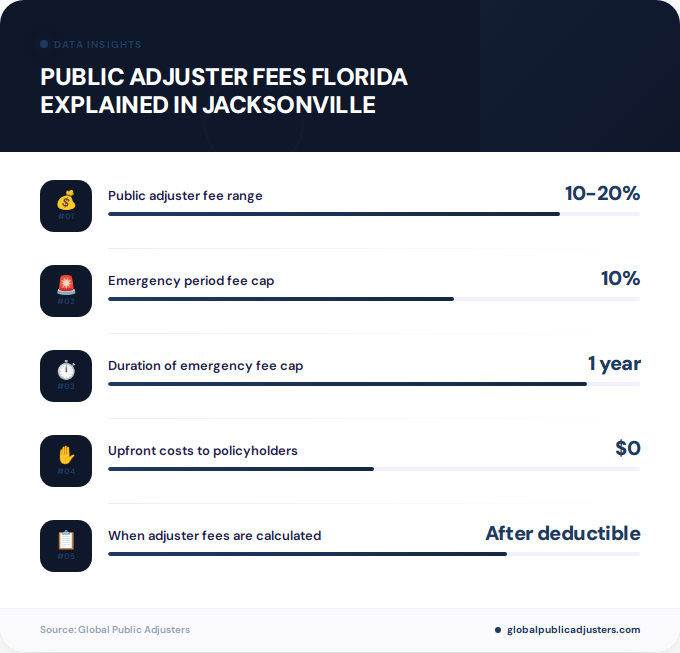

Public adjuster fees in Jacksonville, Florida, range from10% to 20%of the final insurance settlement, with no upfront costs and payment only upon successful claim resolution. Fees are capped at10% for one yearfollowing a governor-declared state of emergency and are deducted from the settlement after your deductible is paid.

When hurricane damage, flooding, or fire impacts your Jacksonville property, understandingpublic adjuster fees in Floridacan mean the difference between leaving money on the table and securing a fair settlement. Unlike insurance company adjusters who work for insurers, public adjusters advocate exclusively for policyholders, navigating complex claims while charging contingency-based fees that align their success with yours.

The fee structure for public adjusters in Jacksonville and across Florida is strictly regulated by theFlorida Department of Financial Services, protecting consumers while ensuring professionals are compensated fairly. With Jacksonville’s vulnerability to hurricanes, tropical storms, and coastal flooding, knowing these regulations becomes critical for property owners in neighborhoods from Riverside to San Marco to the Beaches.

What Are Public Adjuster Fees in Jacksonville?

Public adjuster fees represent the percentage-based commission charged by licensed professionals who manage your insurance claim from documentation through final settlement. In Jacksonville, these fees operate on acontingency basis, meaning you pay nothing upfront and only compensate the adjuster when your claim successfully resolves.

This payment structure aligns incentives: the higher your settlement, the more the adjuster earns. For Jacksonville homeowners facing damage from coastal weather patterns or commercial property owners dealing with losses in Arlington or Mandarin, this arrangement provides professional representation without financial risk if the claim fails.

The fees are calculated as a percentage of the gross settlement amountafter your deductible is subtracted. For example, if your insurance company pays $100,000 and your deductible is $5,000, the adjuster’s fee applies to the $95,000 net payment you receive.

How Much Do Public Adjusters Charge in Jacksonville?

The standard fee range for public adjusters in Jacksonville falls between10% and 20%of the final insurance settlement. This range remains consistent with statewide Florida practices and reflects the complexity and scope of your particular claim.

Several factors influence where within this range your specific fee lands, including claim complexity, property type, damage extent, and whether your claim involves multiple coverage types. A straightforward residential roof claim might command fees at the lower end, while a complex commercial property loss involving business interruption could justify higher percentages.

| Fee Type | Percentage Range | When It Applies |

|---|---|---|

| Standard Fee | 10-20% | Non-emergency claims |

| Emergency Cap | 10% maximum | First year after emergency declaration |

| Post-Emergency | Up to 20% | After one-year emergency period expires |

According toindustry data from Florida’s public adjuster associations, these fees have remained relatively stable over the past decade, providing predictable costs for policyholders across Duval County and surrounding areas.

What Florida Regulations Govern Public Adjuster Fees?

Florida maintains some of the nation’s most comprehensive public adjuster regulations, administered through the Florida Department of Financial Services (DFS). These rules protect Jacksonville consumers while establishing professional standards that exceed requirements in many other states.

Public adjusters in Florida must complete rigorous licensing requirements, including apprenticeship periods and continuing education. This elevated barrier to entry results in demonstrably lower complaint rates compared to states with minimal licensing standards, benefiting Jacksonville property owners who hire these professionals.

Florida’s public adjuster licensing requirements create a professional standard that protects consumers while ensuring adjusters possess the technical knowledge needed to maximize legitimate claim values. The apprenticeship requirement alone weeds out those who view this as a quick-money opportunity rather than a professional career.

Key regulatory protections include prohibitions on charging fees for services not performed, restrictions on collecting fees before the insurance company makes payment, and limitations on when and how adjusters can solicit clients. Solicitation is permitted only Monday through Saturday between 8 a.m. and 8 p.m., protecting vulnerable homeowners from predatory practices following disasters.

Theproposed Senate Bill 266, effective July 1, 2026, strengthens these protections further by requiring contract disclosures in minimum 18-point font and enhancing cancellation rights for vulnerable adults.

When Is Payment Due to a Public Adjuster?

Payment to your public adjuster occurs only after the insurance company disburses funds to you, creating a true contingency arrangement with zero upfront costs. This timing protects Jacksonville homeowners and business owners from paying for services before seeing results.

When your insurer issues a settlement check, the payment typically follows one of two formats: a joint check made payable to both you and the adjuster, or a check to you alone with a separate invoice from the adjuster. The specific payment mechanism should be clearly outlined in your contract.

For claims involving multiple payments over time, such as initial emergency funds followed by supplemental payments for additional discovered damage, the adjuster’s fee applies to each disbursement. If your initial settlement is $50,000 and a later supplement adds $25,000, the agreed percentage applies separately to both amounts.

Importantly, Florida law prohibits adjusters from charging fees on insurance payments made before you signed the contract. If your insurer already issued a partial payment for emergency repairs before you hired representation, that amount remains entirely yours.

How Do Emergency Fee Caps Work?

Florida’s emergency fee cap represents one of the state’s most significant consumer protections, limiting public adjuster fees to10% maximum for one yearfollowing a governor-declared state of emergency. For Jacksonville residents, this provision frequently activates during hurricane season and major storm events.

When the Governor declares a state of emergency affecting Duval County, any public adjuster contract signed during the subsequent 12 months for damage related to that event cannot exceed 10% of claim payments. This cap applies regardless of claim complexity or property type.

After the one-year emergency period expires, fees can increase to the standard 20% maximum. However, contracts signed during the emergency period remain bound by the original 10% cap for the duration of that specific claim, even if resolution extends beyond the one-year window.

For example, if Hurricane Season 2026 brings a qualifying storm to Jacksonville in August and you sign a public adjuster contract in September 2026, your fee remains capped at 10% even if the claim settles in 2027. This protection proved valuable following recent hurricanes when claim resolution often extended 18-24 months due to contractor shortages and complex damage assessments.

What Should Your Public Adjuster Contract Include?

A legally compliant public adjuster contract in Jacksonville must contain specific elements mandated by Florida law. Understanding these requirements helps you identify legitimate professionals and avoid problematic agreements.

Every contract must display the adjuster’s license number, firm name, complete loss description, and fee percentage. Under the updated regulations taking effect in 2026, the fee disclosure must appear inminimum 18-point font, making it impossible to miss or misunderstand.

Fee Percentage:18-point font minimum

Firm Information:Legal name and address

Cancellation Rights:Clear timeframe stated

Payment Terms:Contingency basis explained

Service Scope:All included services listed

Dispute Resolution:Process clearly outlined

The contract should specify whether the fee percentage applies to gross or net settlement amounts and clarify how deductibles affect calculations. Reputable Jacksonville adjusters provide contracts written in plain language that clearly explain these financial arrangements without legal jargon.

Beware of contracts containing provisions that seem to favor the adjuster disproportionately, such as clauses allowing unilateral fee increases or limiting your ability to communicate directly with your insurance company. Such terms may violate Florida regulations and signal unprofessional practices.

How Do You Verify a Public Adjuster’s Credentials?

Verifying your public adjuster’s credentials protects you from unlicensed operators and ensures you work with qualified professionals. The Florida Department of Financial Services maintains a searchable database where you can confirm licenses and review complaint histories.

Request to see the adjuster’s license on-site before signing any contract. The license should display current status, the adjuster’s full legal name, and a unique license number. Cross-reference this information with the DFS database to confirm validity and check for disciplinary actions or consumer complaints.

Beyond basic licensing, inquire about professional affiliations such as membership in theFlorida Association of Public Insurance Adjusters (FAPIA). While not mandatory, such memberships often indicate commitment to industry standards and ongoing professional development.

For Jacksonville-specific claims, consider whether the adjuster maintains familiarity with local building codes, typical construction costs in Duval County, and regional weather patterns that affect damage assessment. An adjuster experienced with coastal properties understands how saltwater exposure, wind-driven rain, and humidity impact claims differently than inland damage.

What Are Your Cancellation Rights?

Florida law provides robust cancellation rights that allow you to exit a public adjuster contract under various circumstances without penalty. Understanding these rights prevents you from feeling locked into arrangements that no longer serve your interests.

Standard cancellation rights extend10 business daysfrom the date you sign the contract. During this period, you can cancel for any reason without owing fees or facing penalties. Simply provide written notice to the adjuster within the specified timeframe.

Enhanced cancellation rights apply during declared emergencies. For contracts signed after a governor-declared state of emergency, you can cancel within30 days of the loss occurrence or 10 days after signing, whichever period is longer. This extended window recognizes that disaster victims may sign contracts under duress and deserve additional time to reconsider.

Vulnerable adults receive even greater protection under Florida’s updated regulations. If you qualify as a vulnerable adult, you can cancel your public adjuster contract at any time without penalty, providing crucial safeguards for seniors and individuals with disabilities who may be targeted by unscrupulous operators following Jacksonville area disasters.

Do Fees Differ Between Commercial and Residential Claims?

The same fee caps and regulatory framework apply to both commercial and residential claims in Jacksonville. Whether you’re filing a claim for your San Jose home or your Southside commercial property, the 10-20% fee structure and emergency caps remain identical.

However, commercial claims often involve greater complexity that may influence where within the allowable range your actual fee falls. Business interruption calculations, inventory losses, equipment valuations, and compliance with commercial policy provisions require specialized expertise that adjusters may price toward the higher end of the spectrum.

Commercial claims in Jacksonville’s business districts frequently involve multiple coverage types simultaneously: property damage, business income loss, extra expense coverage, and potentially civil authority or ingress/egress provisions. The coordination required across these coverage areas justifies thorough professional representation.

Regardless of property type, your contract must clearly state the fee percentage and apply it consistently across all coverage components. An adjuster cannot charge 10% on property damage while charging 20% on business interruption without explicit disclosure and your informed consent.

How Do Public Adjusters Impact Settlement Amounts?

Research demonstrates that policyholders who hire public adjusters typically receive substantially higher settlements than those who negotiate directly with insurance companies. A statewide Florida study from 2008-2009 found that claimants with public adjusters averaged$9,379 per non-catastrophe claim, providing data-driven justification for the fees charged.

Public adjusters bring technical expertise in policy interpretation, damage assessment, and loss documentation that individual property owners typically lack. They understand coverage nuances that might otherwise go unnoticed, ensuring you receive payment for all legitimate claim elements.

For Jacksonville properties, this expertise proves particularly valuable given the region’s exposure to multiple peril types. A public adjuster recognizes when wind damage triggers different coverage provisions than flood damage, maximizes claims involving both primary structure and detached buildings, and identifies additional living expense entitlements that homeowners might overlook.

The negotiation skills public adjusters bring to claim discussions often prove decisive. Insurance companies employ experienced adjusters and legal teams; having professional representation levels the playing field and prevents settlements that undervalue legitimate losses.

Even after deducting the adjuster’s fee, policyholders frequently net more money than they would have received negotiating independently. If hiring an adjuster increases your settlement from $75,000 to $125,000, paying a 10-15% fee on the higher amount still leaves you significantly ahead financially while eliminating the stress of managing the claim yourself.

What Are the Best Practices When Hiring in Jacksonville?

Following established best practices when hiring a public adjuster maximizes your chances of a successful claim outcome while protecting you from problematic service providers. Jacksonville property owners should approach this decision systematically rather than signing with the first adjuster who contacts them.

Document everything before the adjuster arrives.Take comprehensive photos and videos of all damage, create written inventories of damaged property, and preserve evidence of loss. This documentation supports your claim regardless of who represents you and provides your adjuster with thorough baseline information.

Interview multiple adjusters before making a selection. Compare not just fee percentages but also experience with your specific damage type, familiarity with Jacksonville’s neighborhoods and construction practices, and communication style. The lowest fee doesn’t guarantee the best outcome if that adjuster lacks relevant expertise.

Request and check references from previous Jacksonville-area clients. Reputable adjusters readily provide contact information for satisfied customers who experienced similar losses. Speaking with these references reveals insights about communication frequency, claim timelines, and settlement satisfaction that marketing materials cannot.

Understand that emergency situations create urgency but shouldn’t eliminate due diligence. Even when facing displaced living situations after hurricane damage in Beaches neighborhoods or fire loss in Riverside, taking time to verify credentials and review contracts carefully pays dividends throughout the months-long claim process.

For homeowners dealing with complex property issues, the expertise found atprofessional public adjusting firmscan make a substantial difference in claim outcomes. While the specific nature of damage varies considerably, from the garage door issues some homeowners face to the larger structural concerns that require professional assessment, qualified public adjusters bring specialized knowledge to maximize legitimate claim values.

Key Takeaways

- Standard fees range from 10-20%of your insurance settlement in Jacksonville, with no upfront costs and payment only after successful claim resolution

- Emergency caps limit fees to 10%for one year following governor-declared emergencies, protecting disaster victims from excessive charges

- All contracts must include license numbers, fee percentages in 18-point font, and clear cancellation rightsunder Florida law effective July 2026

- Verify credentials through the Florida Department of Financial Services databasebefore signing any contract to ensure you work with licensed professionals

- Cancellation rights extend 10-30 days depending on circumstances, with enhanced protections for vulnerable adults who can cancel anytime

- Research shows adjusters increase settlement values substantially, often exceeding their fees and netting policyholders more money than self-representation

- Commercial and residential claims follow identical fee structures, though complexity may influence where within the allowable range specific fees fall

People Also Ask

Are public adjuster fees tax deductible in Florida?

Public adjuster fees may be tax deductible as a miscellaneous itemized deduction related to casualty losses, though tax law changes have limited such deductions. Consult a qualified tax professional regarding your specific situation, as deductibility depends on whether the loss qualifies under IRS rules and exceeds applicable thresholds.

Can I negotiate public adjuster fees?

Public adjuster fees are negotiable within Florida’s regulatory limits of 10-20%, with emergency caps at 10%. Factors influencing negotiation include claim complexity, potential settlement size, and competitive market conditions. Larger claims sometimes command lower percentage fees while maintaining adjuster profitability, creating room for discussion.

What happens if my claim is denied?

If your insurance company denies your claim, you owe no fees to your public adjuster under contingency arrangements, as payment only occurs upon successful settlement. However, some adjusters may pursue appeals or litigation, potentially involving additional costs or modified fee structures that should be discussed before proceeding beyond initial denial.

Do public adjusters charge for initial consultations?

Most Jacksonville public adjusters offer free initial consultations to assess your claim and explain their services. This no-obligation meeting allows you to understand potential claim value, discuss fee structures, and evaluate whether professional representation makes financial sense for your specific situation before committing to a contract.

How long does it take to settle a claim with a public adjuster?

Claim settlement timelines vary from several weeks for straightforward losses to 12-24 months for complex disasters, depending on damage extent, insurance company responsiveness, and whether disputes require formal resolution. Public adjusters cannot accelerate insurer decision-making but often expedite the process through thorough documentation and professional communication.

Should I hire a public adjuster before or after filing a claim?

Hiring a public adjuster immediately after damage occurs but before filing provides maximum benefit, as they can document losses comprehensively, prepare accurate estimates, and file properly the first time. However, adjusters can also assist with denied or undervalued claims already in process, potentially recovering additional compensation through supplemental claims or appeals.

Frequently Asked Questions

What percentage do public adjusters charge in Jacksonville?+

Public adjusters in Jacksonville charge between 10% and 20% of your final insurance settlement on a contingency basis. During declared emergencies, fees are capped at 10% for the first year. The exact percentage depends on claim complexity, property type, and damage extent, with all fees deducted after your deductible.

Do I pay a public adjuster if my claim is denied?+

No, you owe no fees if your claim is denied, as public adjusters work on contingency and only receive payment when you receive a successful settlement. This no-win, no-fee structure protects you from paying for unsuccessful representation, aligning the adjuster’s incentives directly with achieving a positive outcome for your claim.

When exactly do I pay my public adjuster?+

You pay your public adjuster only after the insurance company issues payment on your claim, not before. Payment typically occurs when you receive settlement checks, which may be joint checks requiring both signatures or separate disbursements where you pay the adjuster directly according to the contract terms established upfront.

How do I verify a public adjuster’s license in Florida?+

Verify public adjuster licenses through the Florida Department of Financial Services online database by searching the adjuster’s name or license number. Request to see the physical license before signing any contract, cross-reference the information with DFS records, and check for complaints, disciplinary actions, or license status issues.

Can I cancel my public adjuster contract in Jacksonville?+

Yes, Florida law provides cancellation rights ranging from 10 business days standard to 30 days during declared emergencies, whichever provides longer protection. Vulnerable adults can cancel anytime without penalty. Cancellation must be submitted in writing, and you owe no fees for services not yet performed or before insurance payments are received.

Are public adjuster fees the same for commercial and residential claims?+

Yes, the same 10-20% fee structure and emergency caps apply equally to commercial and residential claims in Jacksonville. However, commercial claims often involve greater complexity with multiple coverage types, which may influence where within the allowable range your specific fee falls based on the work required to maximize your settlement.

Is hiring a public adjuster worth the cost?+

Research shows policyholders with public adjusters receive substantially higher settlements that typically exceed the fees charged. A Florida study found claimants averaged $9,379 per non-catastrophe claim with professional representation. Even after deducting fees, most policyholders net more money than self-representation would yield, while eliminating claim management stress and ensuring thorough documentation.