How a Denied Insurance Claim Public Adjuster in Florida Can Help You Win Your Appeal

Quick Answer

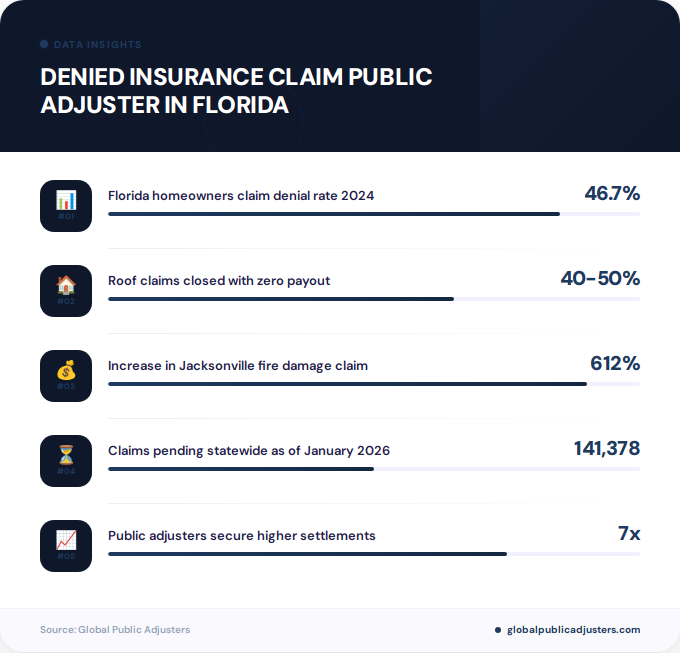

A denied insurance claim public adjuster in Florida can help you appeal underpaid or rejected claims, often securing settlements 7 times higher than initial offers. With Florida’s claim denial rate averaging 46.7% in 2024 and many roof claims closed with zero payout, hiring a public adjuster provides expert negotiation and documentation to maximize your settlement.

If your insurance company denied your property claim in Florida, you’re not alone. In 2024, Florida homeowners faced a staggering46.7% average denial rate, with many claims rejected or closed with zero payout despite legitimate damage. The state’s insurance market has become increasingly volatile following hurricanes like Milton, leaving thousands of policyholders scrambling for answers when carriers refuse to honor their coverage obligations.

The good news? Adenied insurance claim public adjuster in Floridacan level the playing field. These licensed professionals work exclusively for policyholders, not insurance companies, and have secured dramatic settlement increases. In one Jacksonville case, a fire damage claim initially valued at $12,500 by the insurer was successfully appealed to$89,000, representing a 612% increase. This comprehensive guide explores how public adjusters navigate Florida’s complex claims landscape and what you need to know to appeal a denied claim successfully.

Why Are Florida Insurance Claims Being Denied at Record Rates?

Florida’s insurance market is experiencing unprecedented turmoil, with denial rates skyrocketing across multiple categories. The46.7% homeowners claim denial ratein 2024 reflects systemic pressures from natural disasters, aggressive fraud prevention measures, and carrier instability. As of January 2026,141,378 claims remained pending statewide, with 63,826 new claims opened and 68,750 closed during that month alone.

The roof claim sector has been particularly hard hit. In 2024,40 to 50% of roof claims were closed with $0 payout. Carriers like Allstate Vehicle and Property denied 50.9% of roof claims, while USAA closed 49.5% without payment. This aggressive approach stems from insurers attempting to reduce losses following consecutive hurricane seasons and increased scrutiny of potentially fraudulent claims.

| Year | Homeowners Denial Rate | Roof Claims with $0 Payout |

|---|---|---|

| 2024 | 46.7% | 40-50% |

| Jan 2026 | Data pending | Trend continuing |

Policy cancellations compound the crisis.Praetorian Insurance posted an 11.19% cancellation rate, affecting 1 in 9 policies, while 9,865 nonrenewals occurred in January 2026 alone. Some carriers reported overall cancellation rates of 19%, leaving policyholders vulnerable precisely when they need coverage most.

What Is a Public Adjuster and How Do They Help With Denied Claims?

A public adjuster is a licensed insurance professional who works exclusively for policyholders, not insurance companies. Unlike the company adjuster assigned by your insurer, adenied insurance claim public adjuster in Floridaadvocates solely for your interests, ensuring you receive the full settlement you’re entitled to under your policy terms.

When an insurance company denies your claim, they typically provide minimal explanation or cite vague policy exclusions. Public adjusters bring specialized expertise to challenge these denials through comprehensive documentation, damage assessment, and aggressive negotiation. They understand Florida’s unique insurance regulations and know exactly how to counter common denial tactics like “pre-existing damage” allegations or technical filing errors.

The value proposition is clear:insurers paid an average of $3,600 less on claimswhen policyholders didn’t use public adjusters. In complex denied claims, the difference can be exponentially higher. Professional adjusters handle the entire appeals process, from initial review through appraisal or litigation if necessary, removing the burden from overwhelmed homeowners.

“With denial rates surging past 46% in Florida, public adjusters have become essential advocates for policyholders facing aggressive claim tactics. Our contingency fee model means we only succeed when you do, aligning our interests completely with maximizing your settlement.”

What Are the Most Common Reasons for Denied Insurance Claims in Florida?

Understanding why claims get denied is the first step toward a successful appeal.Florida insurers employ several standard denial reasons, many of which can be effectively challenged with proper documentation and expertise.

Pre-existing damage claimsrepresent the most common denial tactic. Insurers argue that hurricane damage or water intrusion existed before the current policy period, therefore isn’t covered. In reality, distinguishing new damage from old requires expert assessment that company adjusters often skip.

Filing errors and missed deadlinesaccount for numerous denials. Florida policies typically require claim notification within specific timeframes, often as short as days after discovery. Simple procedural mistakes like incomplete documentation or missed inspection appointments give insurers easy grounds for denial.

Fraud suspicionshave intensified following legislative crackdowns. Carriers now scrutinize claims more aggressively, sometimes denying legitimate damage due to overzealous fraud detection. The 2026 legislation (HB 427) reflects ongoing concerns about solicitation abuse while attempting to protect vulnerable policyholders from predatory practices.

Natural disaster overloadcreates systemic denial issues. Following Hurricane Milton and other major events, insurers faced unprecedented claim volumes. Some responded by tightening approval standards or using automated systems to deny claims en masse.Florida’s HB 527 legislationaddresses this by mandating human oversight for AI-driven claim denials.

Policy coverage disputesarise when insurers interpret exclusions broadly or claim specific damage types aren’t covered. Wind versus water damage in hurricane claims frequently generates disputes, as policies may cover one but exclude the other.

How Much More Can a Public Adjuster Recover on a Denied Claim?

The financial impact of hiring a public adjuster can be transformative. In documented cases across Florida, adjusters have secured settlements ranging from modest increases to complete reversals of denied claims. The Jacksonville fire damage case mentioned earlier demonstrates the potential upside: an initial company offer of$12,500 increased to $89,000after public adjuster intervention.

Statistics consistently show significant value differences. Without professional representation,policyholders receive on average $3,600 lessthan they would with a public adjuster. For complex property damage involving multiple systems, structural issues, or business interruption, the differential can reach tens or hundreds of thousands of dollars.

In January 2026 alone,1,792 appraisals were invokedin Florida, representing cases where policyholders and insurers couldn’t agree on settlement values. Of litigated claims,63% closed favorably for consumers, indicating that challenges to initial denials or lowball offers frequently succeed when properly presented.

Source:Company Adjuster

Status:Denied/Underpaid

Increase:612%

Status:Successfully Appealed

Litigation Success:63%

Appraisals (Jan 2026):1,792

The recovery potential varies based on claim complexity, damage extent, and policy limits. For those navigating major property damage, the expertise provided byGlobal Public Adjustersensures every recoverable dollar is identified and pursued through meticulous damage assessment and aggressive negotiation.

How Does the Denied Claim Appeal Process Work in Florida?

Appealing a denied insurance claim in Florida follows a structured process that requires prompt action and thorough documentation. Time is critical, as policies typically impose strict appeal deadlines ranging from 30 to 90 days after denial notification.

Step 1: Review the denial letter.Insurers must provide written explanation for claim denials. Public adjusters analyze this documentation to identify weaknesses in the insurer’s reasoning and develop counter-arguments based on policy language and damage evidence.

Step 2: Conduct independent damage assessment.Professional adjusters perform comprehensive property inspections, often bringing in specialized contractors, engineers, or estimators to document damage the company adjuster missed or undervalued. This creates an evidence package to support the appeal.

Step 3: File formal appeal.The appeal package includes detailed damage documentation, repair estimates, policy analysis, and legal arguments why the denial was improper. Professional presentation significantly impacts success rates.

Step 4: Negotiate settlement.Most appeals resolve through negotiation before reaching appraisal or litigation. Public adjusters leverage their expertise and relationships with insurance companies to secure fair settlements without extended legal battles.

Step 5: Invoke appraisal or pursue litigation.When negotiation fails, Florida policyholders can invoke appraisal clauses (1,792 invoked in January 2026) or file lawsuits.Legal action proved successful in 63% of cases, demonstrating that persistence pays.

Throughout this process, adenied insurance claim public adjuster in Floridamanages all communication with the insurer, relieving policyholders of the stress and technical complexity involved in challenging powerful insurance companies.

How to Choose the Right Public Adjuster for Your Denied Claim

Selecting the right public adjuster dramatically affects your appeal’s outcome. Florida requires public adjusters to hold state licenses, but credentials alone don’t guarantee quality service. Look for adjusters with specific experience handling denied claims similar to yours, whether fire damage, hurricane losses, water intrusion, or roof failures.

Verify licensing and credentials.Check the Florida Department of Financial Services database to confirm active licensing and investigate any disciplinary actions. The2026 HB 427 legislationintroduced new consumer protections, including enhanced DFS authority to fine solicitors up to $5,000 per violation and special contract cancellation rights for vulnerable adults.

Assess local expertise.Florida’s insurance market varies significantly by region. An adjuster familiar with Miami-Dade hurricane claims may lack experience with Panhandle tornado damage or Tampa Bay flood issues. Choose adjusters with proven track records in your specific area and damage type.

Understand fee structures.Most public adjusters work on contingency, typically charging 10% to 20% of the settlement. This “no win, no fee” model aligns their interests with yours. Be cautious of adjusters requesting upfront payments or charging unreasonably high percentages.

Review case studies and references.Reputable adjusters provide documented success stories, like the Jacksonville case where a denied claim increased 612%. Request references from recent clients with similar claim types and verify their satisfaction.

What Does It Cost to Hire a Public Adjuster in Florida?

Public adjuster fees in Florida typically range from10% to 20% of the final settlement, though pricing varies based on claim complexity, damage severity, and the work required to successfully appeal. This percentage-based model means adjusters only earn payment when they secure a settlement, creating strong incentive to maximize your recovery.

For denied claims specifically, fees often fall toward the higher end of this range due to the additional expertise and effort required to overturn denials and negotiate with resistant insurers. However, even at 20%, the net recovery frequently exceeds what policyholders would receive handling claims independently.

Consider the mathematics: if an insurer denies your $100,000 claim entirely, you receive $0 without intervention. A public adjuster charging 20% who successfully appeals and secures the full $100,000 settlement leaves you with $80,000. That’s infinitely better than zero, and in many cases, adjusters secure amounts exceeding initial estimates.

Pricing varies based on your specific project complexity, property type, damage extent, and appeal difficulty. Premium public adjusting firms emphasize value and comprehensive service over low-cost providers who may lack the resources or expertise to challenge major denials effectively. For custom quotes based on your situation, contact experienced professionals who can evaluate your specific needs.

Additional costs to consider:Some claims require independent expert assessments (engineers, contractors, forensic specialists) to document damage properly. Reputable public adjusters typically advance these costs and recover them from the settlement, but clarify this arrangement upfront.

Key Takeaways

- Florida’s 46.7% claim denial rate in 2024makes public adjuster representation increasingly essential for securing fair settlements on legitimate damage.

- Public adjusters secure settlements averaging $3,600 morethan policyholders receive independently, with some denied claims increasing over 600% after professional intervention.

- Roof claims face particularly high denial rates, with 40-50% closed at $0 payout in 2024, requiring expert documentation to overcome insurer resistance.

- The appeal process requires prompt actionwithin 30-90 days of denial and benefits significantly from professional damage assessment and policy analysis.

- Contingency fee structures (10-20% of settlement)align public adjuster incentives with policyholders, eliminating upfront costs while ensuring aggressive representation.

- Florida legislation protects consumersthrough HB 527 (AI oversight) and HB 427 (vulnerable adult protections), but navigating these regulations requires specialized knowledge.

- With 141,378 pending claims as of January 2026and ongoing carrier instability, prompt action with qualified representation prevents claim abandonment or underpayment.

People Also Ask

What percentage of insurance claims get denied in Florida?

Florida homeowners insurance claims faced a 46.7% average denial rate in 2024, driven by hurricanes like Milton and increased insurer scrutiny. Roof claims experienced even higher denial rates, with 40-50% closed with zero payout at major carriers.

Why are Florida insurance claims being denied?

Common denial reasons include pre-existing damage allegations, filing errors, fraud suspicions, natural disaster claim overload, and aggressive policy exclusion interpretations. Insurers facing financial pressure from consecutive hurricane seasons have tightened approval standards significantly.

Do I need a public adjuster for a denied claim in Florida?

Yes, public adjusters provide significant value for denied or underpaid claims, securing settlements averaging $3,600 more than policyholders receive independently. In complex cases, increases of 612% or more have been documented, making professional representation highly worthwhile.

How long do I have to appeal a denied insurance claim in Florida?

Most Florida insurance policies require appeals within 30 to 90 days of receiving the denial letter. Prompt action is critical, as missing these deadlines can permanently forfeit your right to challenge the denial and recover settlement funds.

Can a public adjuster reopen a closed claim in Florida?

Public adjusters can often reopen claims closed with inadequate settlements or denied improperly, provided you’re within policy deadlines and statute of limitations periods. They identify new damage evidence or policy interpretation errors that justify reconsideration.

What is the success rate for appealing denied insurance claims in Florida?

In litigated cases, 63% of claims closed favorably for consumers in recent Florida data. With professional public adjuster representation, success rates typically exceed this baseline through effective negotiation that resolves most appeals before litigation becomes necessary.

Frequently Asked Questions

How quickly should I hire a public adjuster after my claim is denied?+

Contact a public adjuster immediately after receiving a denial letter, as most policies impose 30-90 day appeal deadlines. Early intervention allows adjusters to preserve evidence, document damage properly, and develop comprehensive appeal strategies before critical deadlines expire.

Will hiring a public adjuster make my insurance company retaliate?+

No, Florida law prohibits insurers from canceling policies or retaliating against policyholders who hire public adjusters. Your right to professional representation is protected, and adjusters actually facilitate smoother claim resolution through professional documentation and communication.

Can a public adjuster help if my claim was denied due to late filing?+

Public adjusters often successfully challenge late filing denials by documenting reasonable causes for delay, such as evacuation orders, continuing damage discovery, or insurer communication failures. Many technical denials can be overturned with proper legal arguments and documentation.

What documents do I need to provide to a public adjuster?+

Bring your insurance policy, denial letter, all correspondence with the insurer, photos of damage, contractor estimates, and receipts for emergency repairs. The public adjuster will obtain additional documentation through independent inspections and expert assessments as needed.

How long does the appeal process take with a public adjuster?+

Simple appeals may resolve within 30-60 days through negotiation, while complex cases requiring appraisal or litigation can take 6-12 months or longer. Public adjusters expedite the process through efficient documentation and aggressive negotiation tactics.

Are public adjuster fees tax deductible in Florida?+

Public adjuster fees for casualty losses may be tax deductible under certain circumstances, particularly for business property claims. Consult a tax professional regarding your specific situation, as deductibility depends on loss type, property use, and applicable tax law.

Can I switch public adjusters if I’m unhappy with my current one?+

Yes, you can terminate a public adjuster contract, though early termination may involve fee obligations for work already completed. The 2026 HB 427 legislation provides special cancellation rights for vulnerable adults without penalty, recognizing the need for consumer protection.