Commercial insurance claims processis crucial for business owners, especially those in disaster-prone areas. It offers a structured way to seek compensation for unexpected damages, ensuring businesses can recover without shouldering the entire financial burden. Here’s how it generally works:

- Notice of Claim: Inform your insurer about the incident that caused the loss.

- Documentation: Gather evidence, like photos and reports, to support your claim.

- Investigation: An insurance adjuster evaluates the claim details.

- Approval or Denial: The insurer decides on the payout based on the coverage.

- Compensation: If approved, the payout is processed to cover financial losses.

Understanding this process helps you steer risks and ensures your business is protected financially.

In today’s unpredictable world, managing risk is more important than ever for businesses, particularly in areas prone to disasters. While no amount of planning can eliminate all risks, insurance acts as a financial safety net offering protection when things go awry.

Successful companies recognize thatrisk managementandinsuranceare intertwined, ensuring they’re not left holding the bag if disaster strikes. They leverage insurance as a tool to transfer risk, safeguarding against financial losses. This understanding can make the difference between smooth recovery and potentially devastating consequences.

What is a Commercial Insurance Claim?

Acommercial insurance claimis your formal request to an insurance company asking for reimbursement for a financial loss covered under your business insurance policy. It’s like waving a flag to say, “Hey, something went wrong, and I need help!”

Insurance Policy: Your Safety Net

Think of your insurance policy as a safety net. It’s a contract between you and the insurer, outlining what’s covered and how much you’ll receive if something goes wrong. For example, if a hurricane damages your bakery, yourcommercial property insurancecan cover the costs to repair the building, replace equipment, and even compensate for lost income during downtime.

Financial Losses: What’s at Stake?

When disaster strikes, businesses face various financial losses. These can include:

- Property Damage: Costs for repairing or replacing damaged buildings and equipment.

- Business Interruption: Income lost while your business is unable to operate.

- Liability Claims: Costs related to third-party injuries or property damage.

Reimbursement: Getting Your Business Back on Track

Once your claim is approved, the insurance company provides reimbursement to cover these losses. This compensation helps your business get back on its feet without a significant financial hit. For instance, if an electronics store experiences theft, the insurance can cover the stolen merchandise’s value and repair the storefront.

Real-World Example: Theft at an Electronics Store

Imagine an electronics store that was broken into overnight. Thieves stole thousands of dollars worth of merchandise and damaged the storefront. The store’scommercial property insurancekicked in, reimbursing the value of the stolen goods, covering repair costs, and compensating for business interruption during the repair period. This is a classic example of how a commercial insurance claim works in practice.

Understanding these basics can help you steer thecommercial insurance claims processwith confidence, ensuring your business is well-protected and financially resilient.

Triggers for a Commercial Insurance Claim

In business, unexpected events can lead to significant financial strain. Understanding what triggers a commercial insurance claim can help safeguard your business from these unforeseen challenges. Here are the key triggers:

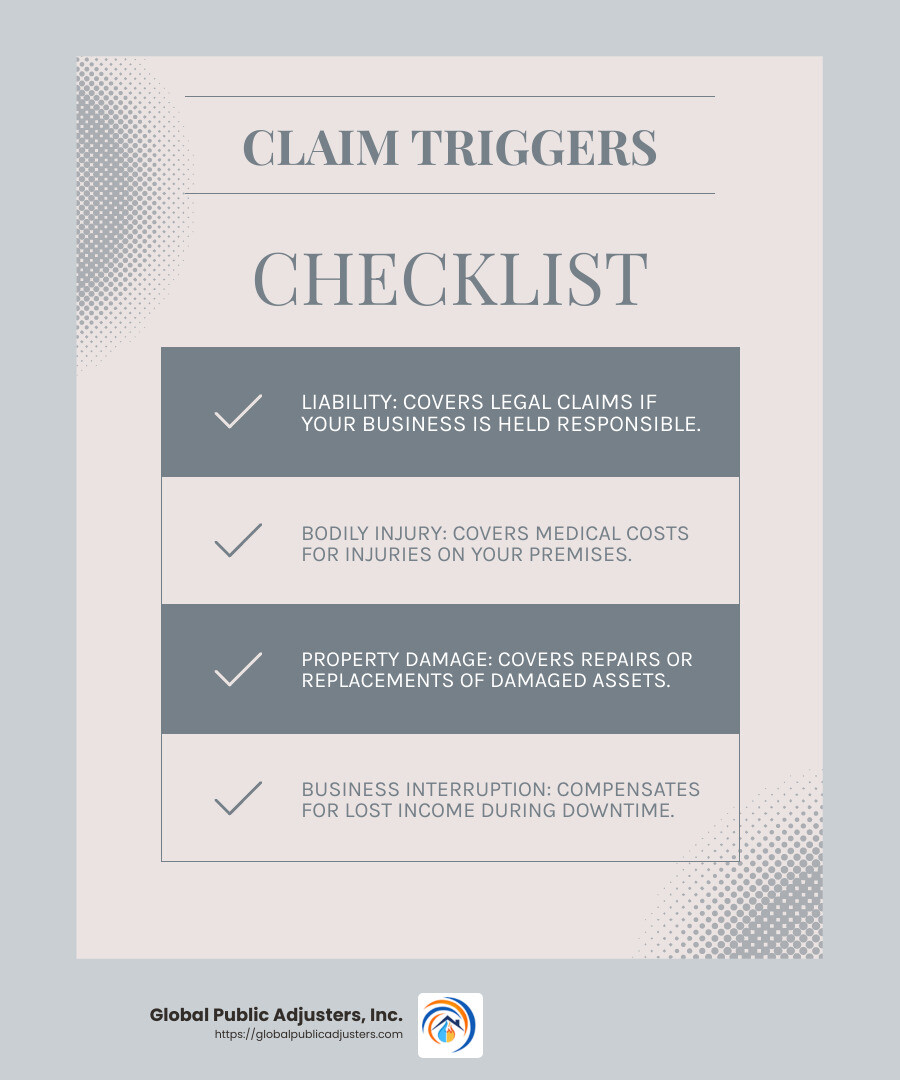

Liability: Protecting Your Business from Legal Claims

Liability claims arise when your business is held responsible for causing harm to others. For instance, if a customer slips on a wet floor in your store and breaks an arm, yourgeneral liability insurancecan cover the medical expenses and any legal fees if the customer decides to sue. This type of coverage is crucial as it protects your business from costly lawsuits.

Bodily Injury: Covering Medical Costs

Bodily injury claims are specific to injuries that occur on your business premises. For example, a construction worker who falls from scaffolding and breaks a leg can file a claim underworkers’ compensation insurance. This insurance covers medical bills and lost wages during recovery, ensuring employees receive the care they need without financial burden.

Property Damage: Repairing and Replacing Assets

Property damage claims focus on the physical assets of your business. Whether it’s a storm damaging your building or a fire destroying equipment,commercial property insuranceis there to help. This insurance covers the costs of repairing or replacing damaged property, keeping your business operational and minimizing downtime.

Business Interruption: Sustaining Your Business During Downtime

When an event halts your business operations, the financial impact can be severe.Business interruption insurancesteps in to cover lost income during these periods. For example, if a hurricane forces your bakery to close, this insurance can cover ongoing expenses like payroll and utilities, ensuring your business survives the interruption.

Real-World Case Study: Storm Damage to a Local Bakery

Consider a local bakery that was heavily damaged by a hurricane. The storm caused structural damage and ruined equipment. The bakery’scommercial property insurancecovered the repair costs, equipment replacement, and even compensated for lost income during the closure. This comprehensive coverage allowed the bakery to recover withouta crippling financial setback.

Understanding these triggers is essential for navigating thecommercial insurance claims processeffectively. By being aware of these potential risks, you can ensure your business is adequately protected and prepared for any eventuality.

The Commercial Insurance Claims Process

Navigating thecommercial insurance claims processcan seem daunting, but breaking it down into clear steps can make it manageable. Understanding each phase—from initial contact to investigation—ensures you’re prepared when an incident occurs.

Initial Contact: Reporting the Incident

The first step is to notify your insurance company as soon as an incident occurs. This prompt action sets the claims process in motion. When you contact your insurer, have all the details ready: the time, place, and nature of the incident. This includes any immediate actions taken, like calling the police or securing the property.

Keeping a log of dates, times, and communication details is crucial. It ensures that you have a clear record of all interactions with your insurer, which can be vital if there are any disputes later on.

Investigation: Assessing the Damage

Once you’ve reported the incident, the insurance company will begin its investigation. This is where an adjuster comes in. The adjuster’s job is to evaluate the extent of the damage and determine the cost of repairs or replacements. They may visit your business to inspect the damage firsthand.

During the investigation, it’s essential to provide all requested documentation promptly. This might include photographs, receipts, and any other evidence that supports your claim. Being organized and thorough can help speed up the investigation process.

The Role of the Adjuster

The adjuster is a key player in thecommercial insurance claims process. They act as the eyes and ears of the insurance company, ensuring that the claim is fair and accurate. While it might feel like they’re working for the insurer, their goal is to reach an equitable settlement based on the policy terms and the evidence provided.

It’s beneficial to maintain open communication with the adjuster. Answer their questions honestly and provide any additional information they might need. If you disagree with their assessment, you can negotiate or provide further documentation to support your claim.

A Smooth Process with Documentation and Communication

The key to a successful claims process is documentation and communication. Keep detailed records, respond quickly to requests, and maintain open lines of communication with your insurer and adjuster. This proactive approach not only helps in resolving claims efficiently but also positions your business for a favorable settlement.

By understanding each step, from initial contact to the adjuster’s role, you can steer thecommercial insurance claims processwith confidence and clarity. This knowledge ensures that your business is protected and that you’re prepared to handle any incidents that may arise.

Types of Commercial Insurance Policies

When it comes to commercial insurance, understanding the different types of policies is crucial. Let’s break down three key terms:claims-made,occurrence, andtail coverage.

Claims-Made Policies

Aclaims-madepolicy offers protection for incidents that both happen and are reported during the policy year. This means if a claim is made after the policy expires, it won’t be covered—even if the incident occurred while the policy was active.

Cost: These policies often start with lower premiums, which gradually increase over the first five years as the policy matures.

Flexibility: Some insurers offer an option called “tail coverage,” which we’ll discuss next, to extend the reporting period even after the policy ends.

Occurrence Policies

Anoccurrencepolicy covers incidents that happen during the policy’s active period, regardless of when the claim is filed. This means even if a claim is made years later, as long as the incident occurred while the policy was active, it will be covered.

Cost: These policies usually have higher upfront premiums compared to claims-made policies, but the rates remain stable over time unless significant changes occur.

Lifetime Coverage: Unlike claims-made policies, occurrence policies don’t require tail coverage because they provide lifetime protection for incidents that occur during the policy period.

Tail Coverage

Tail coverage, or an extended reporting period (ERP), is an option available withclaims-made policies. It allows businesses to file claims even after the policy has expired, as long as the incident occurred during the active policy period.

Importance: This is particularly useful for businesses that switch insurers or discontinue a policy but still want protection for past incidents.

Consideration: Tail coverage can be a valuable addition to a claims-made policy, providing peace of mind and extended protection.

Understanding these policy types helps businesses choose the right coverage to protect against potential losses. By knowing the differences, you can make informed decisions and ensure that your business is well-protected.

Steps to File a Commercial Insurance Claim

Filing acommercial insurance claimcan seem daunting, but breaking it down into simple steps makes it manageable. Here’s how you can ensure a smooth claims process:

1. Contact Your Insurer

First things first, notify your insurance company as soon as possible. Quick action is crucial. Most policies require you to report a claim promptly, sometimes within 24 hours of the incident.

- Tip: Keep your insurance policy and contact information handy. This will help speed up the process.

2. Document the Damage

Once you’re safe, start documenting everything. Detailed records are your best friend when filing a claim.

Take Photos and Videos: Capture clear images and videos of the damage. Include wide shots and close-ups from various angles.

Write It Down: Note the time, date, and location of the incident. If there were witnesses, get their statements too.

Keep a Log: Maintain a log of all interactions with your insurer, including dates, times, and the names of the people you speak with.

3. Provide Proof of Loss

Your insurer will require a “proof of loss” form. This form details what happened and the extent of the damage or loss.

Be Detailed: Include all necessary documentation, such as receipts, repair estimates, and any correspondence related to the incident.

Stay Honest: Provide accurate information. Misrepresenting facts can lead to claim denial.

4. Make Temporary Repairs

Prevent further damage by making necessary temporary repairs. This step is often required by your policy.

Act Quickly: For example, if a window is broken, board it up to prevent weather damage.

Save Receipts: Keep records of all expenses related to these repairs. You can include them in your claim.

By following these steps, you’ll be well-prepared to steer thecommercial insurance claims process. Next, we’ll explore some common examples of claims to further illustrate how this process plays out in real-life situations.

Common Examples of Commercial Insurance Claims

Understanding commoncommercial insurance claimscan help you steer potential issues your business might face. Here are some real-life scenarios:

Storm Damage

Imagine a local bakery in Florida hit by a hurricane. The storm causes structural damage, ruins baking equipment, and spoils inventory. Fortunately, the bakery has commercial property insurance. This policy helps cover the costs to repair the building, replace equipment, and compensate for lost income during the business interruption. It’s a lifeline that ensures the bakery can continue paying bills and payroll while recovering.

Theft

Consider an electronics store that experiences a break-in overnight. Thieves make off with thousands of dollars worth of merchandise and leave the storefront damaged. The store’s commercial property insurance comes to the rescue. It reimburses the store for the stolen goods, repairs the storefront, and covers the business interruption during the repair period. This allows the store to get back on its feet quickly.

Premises Liability

In a department store, a customer slips on a wet floor and breaks her arm. This is where general liability insurance steps in. The policy covers the customer’s medical bills, ongoing physical therapy, and legal expenses when she threatens to sue. This protection helps the store manage unexpected incidents without crippling financial consequences.

Auto Accident

Picture an employee driving a company vehicle who rear-ends another car. Both vehicles sustain damage, and the other driver suffers minor injuries. The company’s commercial auto insurance covers the repairs for both vehicles, the medical expenses of the injured driver, and legal fees when the driver initially threatens to sue. This ensures the company can handle the situation without significant financial strain.

Employee Injury

A construction worker falls from scaffolding at a worksite, breaking his leg. He requires surgery and several weeks off work. Workers compensation insurance is there to help. It covers the worker’s medical bills, rehabilitation costs, and replaces lost wages during recovery. This coverage is crucial for both the employee’s well-being and the company’s financial stability.

These examples highlight the importance of having the right insurance policies in place. They protect businesses from unexpected events and help ensure a swift recovery. Next, we’ll dive into frequently asked questions about thecommercial insurance claimsprocessto further explain this essential aspect of business operations.

Frequently Asked Questions about the Commercial Insurance Claims Process

What are the differences between personal and commercial insurance claims?

Personal insurance claimstypically involve individual coverage like home or auto insurance. These claims are often simpler, focusing on personal assets or damages, such as a tree falling on your house or a fender bender. The process usually involves fewer parties and less complex investigations.

On the other hand,commercial insurance claimsinvolve business-related incidents. These can range from property damage, like a fire in a warehouse, to liability claims, such as a customer injury at a store. Commercial claims often require detailed documentation and involve multiple stakeholders, such as employees, customers, and vendors. The stakes are higher, and the process can be more intricate due to the potential financial impact on the business.

How does technology impact the claims process?

Technology is changing thecommercial insurance claims processin several ways:

Digital Documentation: Businesses can now submit claims online, speeding up the process. Photos and videos of damages can be uploaded instantly, providing immediate evidence.

AI and Automation: Insurance companies use artificial intelligence to analyze claims faster and more accurately. This helps in detecting fraud and accelerating payouts.

Data Analytics: Advanced analytics provide insurers with insights into risk patterns. This helps in tailoring policies and improving the speed and fairness of the claims process.

IoT and Smart Devices: Internet of Things (IoT) devices can monitor business properties in real-time. For example, sensors can detect water leaks or fire hazards, allowing businesses to prevent damage before it happens.

These technological advancements make the claims process more efficient, reducing the time and effort required from both the insurer and the insured.

What should you do if your claim is denied?

If your commercial insurance claim is denied, don’t panic. Here’s a step-by-step approach to handle the situation:

Review the Denial Letter: Carefully read the explanation provided by your insurance company. The denial could be due to missing documentation or misunderstandings.

Gather Evidence: Collect supporting documents, such as photographs, witness statements, or expert opinions that might have been overlooked.

File an Appeal: Most insurance companies have an appeals process. Write a detailed appeal letter, outlining why you believe the denial was incorrect, and attach your supporting evidence.

Seek Legal Advice: If your appeal is denied again, consider consulting a lawyer specializing in insurance claims. They can guide you on further steps or legal action if necessary.

Understanding these steps can help you steer a denial and potentially reverse the decision, ensuring your business gets the compensation it deserves.

Next, we’ll explore the various types of commercial insurance policies to help you choose the right coverage for your business needs.

Conclusion

At Global Public Adjusters, Inc., we understand that navigating thecommercial insurance claims processcan be daunting. Our mission is to turn this complex journey into a straightforward path toward maximizing your settlement. With over 50 years of experience, we’re not just adjusters; we’re your advocates against insurance companies.

Maximizing Settlements

Our team specializes in ensuring you receive the compensation you deserve. We carefully assess every detail of your claim, from initial contact to settlement. By leveraging our expertise, we aim to secure the highest possible payout for your business, covering everything from property damage to business interruptions.

Advocacy Against Insurance Companies

Insurance companies often have their interests at heart, which can make the claims process challenging for policyholders. That’s where we come in. We stand by your side, advocating for your rights and ensuring that your claim is handled fairly and efficiently. Our goal is to alleviate the stress of dealing with insurers, allowing you to focus on what matters most—running your business.

If you’re facing a commercial insurance claim and need expert advocacy,contact us todayto learn how we can help maximize your settlement and provide peace of mind in uncertain times.