How Much Do Public Adjusters Charge in Jacksonville: Complete Fee Guide for 2026

Quick Answer

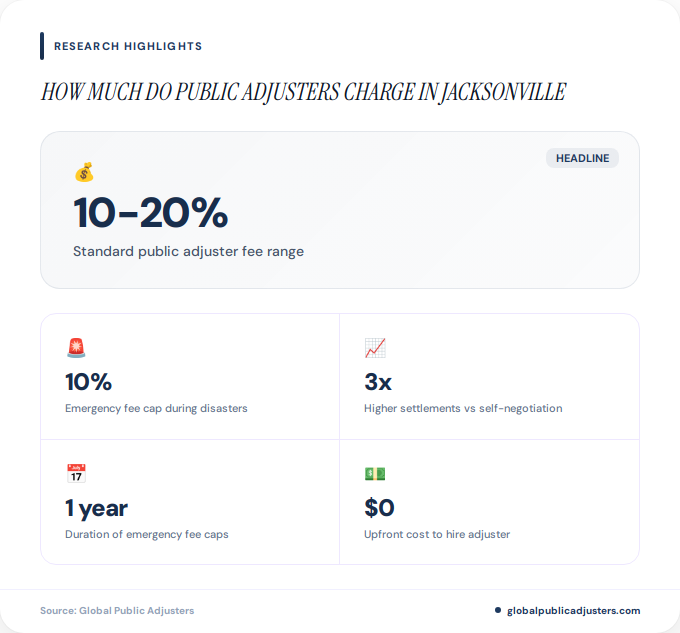

Public adjusters in Jacksonville typically charge between 10-20% of the insurance settlement amount on a contingency basis, with fees strictly capped at 10% during governor-declared states of emergency (common after hurricanes). Florida law ensures you pay nothing upfront and only pay if they recover money for your claim.

Did you know thatpublic adjusters secure settlements averaging 3 times higherthan what policyholders negotiate on their own? Yet in Jacksonville, Florida, many homeowners still hesitate to hire these professionals due to uncertainty about costs. Whether you’re dealing with hurricane damage along the St. Johns River or filing a claim for fire damage in Riverside, understanding public adjuster fees is critical to maximizing your insurance recovery.

This comprehensive guide breaks down exactly how much public adjusters charge in Jacksonville, when emergency caps apply, and whether the investment delivers real value for Northeast Florida homeowners.

What Is the Standard Public Adjuster Fee in Jacksonville?

In Jacksonville, public adjusters typically operate on acontingency fee basis ranging from 10% to 20%of the total insurance settlement amount, minus your deductible. This means you pay nothing upfront and only compensate the adjuster if they successfully recover money from your insurance claim.

For standard residential claims such as fire damage, water damage, or theft, the most common fee structure is20% of the gross settlementminus the deductible. However, many Jacksonville adjusters advertise fees closer to10-15%depending on claim complexity, settlement size, and competitive market factors.

| Claim Type | Settlement Amount | Fee at 10% | Net to Policyholder |

|---|---|---|---|

| Hurricane Damage (Emergency Cap) | $200,000 | $20,000 | $180,000 |

| Fire/Water Damage (Standard) | $200,000 | N/A (20% typical) | $160,000 (at 20%) |

| Supplement/Reopened Claim | $50,000 (new money) | $5,000 | $45,000 |

According toFlorida Best Public Adjusters, the contingency model protects homeowners by aligning the adjuster’s incentives with maximizing your settlement. If your claim is denied or no recovery is achieved, you owe nothing.

For supplement claims where you’re seeking additional compensation on a previously settled claim, Jacksonville adjusters typically charge either10% of the gross settlement minus deductible, or 25% of the new money recovered, whichever is less.

How Do Emergency Fee Caps Work in Jacksonville?

When the Florida Governor declares a state of emergency, such as during hurricane season or after major storms impact Duval County, public adjuster fees are strictly capped at10% of the settlement amount minus the deductible. This consumer protection measure has been particularly relevant in Jacksonville given the city’s vulnerability to hurricanes and tropical storms.

These emergency caps remain in effect forone year from the date of the disaster declaration. For example, if a hurricane strikes Jacksonville in September 2026, any claims filed through September 2027 would fall under the 10% emergency cap, regardless of when the settlement is finalized.

Recent hurricane activity affecting Northeast Florida has made these caps increasingly relevant. Jacksonville homeowners should verify whether their claim qualifies under emergency provisions by checking the date of damage against official governor declarations. Understanding the difference betweenpublic adjusters and insurance company adjustersbecomes even more important during emergencies when settlements can reach six figures.

What Governs Public Adjuster Fees in Florida?

Florida Statute 626.854comprehensively regulates public adjuster compensation throughout the state, including Jacksonville. This legislation ensures transparency, prevents exploitation, and mandates specific contract requirements that protect consumers.

Key provisions under Florida law include:

- Written contracts:All fee agreements must be in writing and clearly specify services, compensation structure, and both parties’ obligations

- State approval:Contracts must reference Florida Statute 626.854 and comply with Department of Financial Services regulations

- Contingency basis:Fees can only be charged as a percentage of the settlement, never as flat fees or hourly rates for residential claims

- Emergency caps:The 10% maximum during declared emergencies is legally enforceable statewide

- No upfront costs:Public adjusters cannot charge retainers, application fees, or any payment before recovery

According toInsurance Claim Recovery Support, Florida’s regulatory framework is among the strictest in the nation, providing Jacksonville homeowners with significant consumer protections compared to other states where fees can reach 40% or higher.

Before signing any agreement with a Jacksonville public adjuster, verify their license through the Florida Department of Financial Services database. Licensed adjusters must maintain bonds, carry errors and omissions insurance, and adhere to continuing education requirements.

How Do Jacksonville Fees Compare to National Averages?

While Jacksonville public adjuster fees align with Florida’s regulated structure, they represent a significant value compared to national norms where fees can vary dramatically by state.

Emergency Cap:10%

Average:10-15%

Regulation:Strict state caps

Typical:10-15%

Caps:Vary by state

Regulation:Inconsistent

Emergency Caps:Rare

Consumer Protection:Limited

Contract Requirements:Minimal

Florida’s legislative framework provides Jacksonville residents with predictable, regulated pricing. Some states allow adjusters to charge fees approaching 40% for complex commercial claims, with minimal oversight or consumer protections.

For perspective,Harrell Adjustingreports that the national median hovers around 10-15%, placing Jacksonville squarely within typical industry standards while benefiting from Florida’s strict caps during emergencies.

When Is Hiring a Public Adjuster Worth the Cost?

Despite the percentage-based fee, Jacksonville homeowners typically realize substantially higher net recoveries when using public adjusters for complex or large claims. Research consistently shows public adjusters secure settlementsaveraging 3 times higherthan what homeowners negotiate independently.

Consider these scenarios where the investment makes financial sense:

Hurricane and storm damage:Jacksonville’s coastal location and proximity to the Atlantic make hurricane claims common. These complex claims involving roof damage, water intrusion, and structural issues benefit enormously from professional representation. A $150,000 settlement at 10% (emergency cap) yields $135,000 to the homeowner compared to a typical $45,000 DIY settlement at $0 fee but $105,000 less net recovery.

Large residential claims exceeding $50,000:As claim complexity and value increase, the expertise gap widens between homeowners and insurance company adjusters. Public adjusters understand policy language, depreciation calculations, and replacement cost valuations that significantly impact payouts.

Denied or underpaid initial claims:Supplement claims represent a growing segment in Jacksonville, particularly in neighborhoods like Mandarin and Ponte Vedra Beach where property values are high. Public adjusters charging 25% of new money recovered can turn a $0 denied claim into a $100,000 settlement, netting the homeowner $75,000.

AtGlobal Public Adjusters, we’ve seen countless Jacksonville families recover full replacement costs after initial lowball offers. The fee percentage becomes irrelevant when comparing net outcomes.

Are Public Adjuster Fees Negotiable in Jacksonville?

Yes, public adjuster fees are negotiable within Florida’s legal parameters. While the law sets maximum caps (20% standard, 10% emergency), Jacksonville adjusters often compete for business by offering lower percentages or tiered structures based on settlement size.

Common negotiation strategies include:

- Large claim discounts:Settlements exceeding $200,000 may qualify for reduced percentages (8-12%) since the adjuster’s work effort doesn’t scale linearly with settlement size

- Tiered structures:Some Jacksonville firms offer graduated fees such as 15% on the first $100,000, 10% on amounts above

- Multiple property discounts:Investors or owners with multiple claims may negotiate portfolio pricing

- Referral incentives:Existing clients referring new business sometimes receive retroactive fee reductions

According toTiger Adjusters, negotiation success often depends on claim timing, complexity, and the adjuster’s current workload. Jacksonville’s competitive market with numerous licensed adjusters creates opportunities for homeowners to shop around.

Always obtain2-3 written quotesbefore committing. Reputable adjusters provide free claim assessments, allowing you to compare not just fees but also experience, references, and proposed strategies.

How to Avoid Excessive Public Adjuster Costs

Jacksonville homeowners can maximize value and minimize unnecessary expenses by following these best practices when engaging public adjusters:

Verify licensing and credentials:Check the Florida Department of Financial Services database to confirm active licensure, disciplinary history, and bond status. Unlicensed adjusters may charge non-compliant fees or provide substandard service.

Read contracts thoroughly:Ensure the agreement specifically references Florida Statute 626.854, clearly states the fee percentage, defines what constitutes the settlement amount, and specifies services included. Watch for hidden charges for engineering reports, photography, or administrative costs.

Understand emergency caps:If your Jacksonville property sustained damage during a declared emergency, confirm the contract reflects the 10% cap. Some adjusters may attempt higher fees if homeowners are unaware of emergency declarations.

Document everything independently:Take comprehensive photos and videos immediately after damage occurs. While your adjuster will conduct thorough documentation, your independent records provide backup and reduce adjuster workload, potentially strengthening your negotiating position on fees.

Compare multiple proposals:The Jacksonville market includes both large firms and independent adjusters. Obtain at least three written assessments comparing estimated settlements, proposed fees, timeline projections, and references from similar claims in areas like Arlington, Riverside, or Neptune Beach.

Timing matters:Florida law allows claims to be filed within specific timeframes after damage. Hiring an adjuster early, ideally within 90 days of loss, maximizes their ability to document damage before repairs begin and strengthens your claim position.

For more context on how public adjusters differ from insurance company representatives, review our detailed comparison ofpublic adjusters versus insurance company adjusters in Florida.

People Also Ask

Do I pay anything upfront to hire a public adjuster in Jacksonville?

No, Jacksonville public adjusters work strictly on contingency, meaning you pay nothing upfront and only compensate them if they successfully recover money from your insurance claim. Florida law prohibits retainers or application fees for residential claims.

What happens if my claim is denied by the insurance company?

If your Jacksonville claim is denied and no settlement is recovered, you owe the public adjuster nothing under the contingency fee model. This no-recovery, no-fee structure protects homeowners from financial risk when challenging denied claims.

How long does the emergency 10% fee cap last in Jacksonville?

The 10% emergency fee cap remains in effect for one year from the date of the governor’s disaster declaration. Any claim filed within that 12-month window qualifies for the reduced fee, even if settlement occurs after the year expires.

Can public adjusters charge hourly rates in Florida?

No, Florida Statute 626.854 prohibits hourly billing for residential property claims. Jacksonville public adjusters must charge percentage-based contingency fees only, ensuring their compensation aligns with maximizing your settlement rather than prolonging the process.

Should I hire a public adjuster for small claims under $10,000?

For minor Jacksonville claims below $10,000, the cost-benefit may not justify hiring a public adjuster since their fee would be $1,000 to $2,000. However, if the claim is complex, denied, or you suspect underpayment, the potential increase often exceeds the fee.

Do public adjuster fees include expert services like engineering reports?

Most Jacksonville public adjusters include standard documentation, photography, and estimate preparation in their contingency fee. However, specialized services like structural engineering reports, environmental testing, or legal consultations may involve separate costs that should be clearly outlined in your contract.

Frequently Asked Questions

How much do public adjusters charge in Jacksonville for hurricane claims?+

Jacksonville public adjusters charge a maximum of 10% of the settlement amount (minus deductible) for hurricane claims filed during governor-declared emergencies. This emergency cap applies for one year from the disaster declaration date and provides significant savings compared to standard 20% fees for non-emergency claims.

What is the average public adjuster fee in Jacksonville?+

The average public adjuster fee in Jacksonville ranges from 10-15% of the settlement amount, depending on claim complexity and whether emergency caps apply. While Florida law allows up to 20% for standard residential claims, competitive market conditions and large settlement sizes often result in negotiated rates toward the lower end of this spectrum.

Are there any upfront costs when hiring a Jacksonville public adjuster?+

No, there are zero upfront costs when hiring a public adjuster in Jacksonville. Florida law requires public adjusters to work on a contingency basis only, meaning you pay nothing unless they successfully recover money from your insurance claim. This no-win, no-fee structure eliminates financial risk for homeowners.

How do supplement claim fees work in Jacksonville?+

For supplement claims in Jacksonville where you’re seeking additional money on a previously settled claim, public adjusters typically charge either 10% of the total gross settlement minus deductible, or 25% of the new money recovered, whichever amount is less. This ensures fair compensation when reopening underpaid claims.

Can I negotiate public adjuster fees in Jacksonville?+

Yes, public adjuster fees are negotiable within Florida’s legal limits. Jacksonville’s competitive market allows homeowners to negotiate lower percentages, particularly for large claims exceeding $100,000, multiple properties, or when obtaining quotes from several adjusters. Always get 2-3 written proposals before committing.

What does Florida law say about public adjuster fees?+

Florida Statute 626.854 governs all public adjuster fees statewide, including Jacksonville. The law caps fees at 20% for standard residential claims, 10% during declared emergencies, and prohibits any charges beyond contingency percentages. All contracts must be written, reference the statute, and clearly specify compensation terms.

Is hiring a public adjuster worth the cost in Jacksonville?+

Hiring a Jacksonville public adjuster is typically worth the cost for claims exceeding $25,000, complex hurricane damage, denied claims, or situations where initial offers seem inadequate. Public adjusters secure settlements averaging 3 times higher than DIY efforts, meaning the net recovery after fees far exceeds what homeowners negotiate alone.

Key Takeaways

- Jacksonville public adjusters charge 10-20% on contingency, with emergency caps at 10% during governor-declared disasters lasting one year from the declaration date

- Zero upfront costsare guaranteed under Florida law, with fees only paid if your claim successfully recovers money from the insurance company

- Florida Statute 626.854 provides strict consumer protections, including written contract requirements, state approval, and prohibition of hourly billing for residential claims

- Public adjusters secure settlements 3x higher on average, making the percentage fee worthwhile for complex claims exceeding $25,000 or denied initial settlements

- Fees are negotiable within legal limits, especially for large claims, multiple properties, or when comparing quotes from 2-3 licensed Jacksonville adjusters

- Supplement claims charge either 10% of total or 25% of new money, whichever is less, providing cost-effective representation for reopened or underpaid claims

- Verify licensing through Florida DFSbefore signing any agreement to ensure compliance with state regulations and avoid unlicensed operators charging non-compliant fees

Conclusion: Making the Right Decision for Your Jacksonville Property Claim

Understanding how much public adjusters charge in Jacksonville empowers you to make informed decisions when facing property damage. Whether you’re dealing with hurricane damage in Ponte Vedra Beach, fire loss in San Marco, or water damage in Mandarin, the 10-20% contingency fee structure aligns the adjuster’s success with maximizing your insurance recovery.

Florida’s strict regulatory framework, including emergency caps and prohibition of upfront costs, provides Jacksonville homeowners with significant protections unavailable in many other states. The data consistently shows that professional representation yields substantially higher settlements, often tripling what homeowners negotiate independently.

Before selecting a public adjuster, verify licensing, compare multiple written proposals, and ensure contracts comply with Florida Statute 626.854. For complex claims, the investment in professional representation typically delivers exponential returns that far exceed the percentage-based fee.

If you’re facing a denied claim, inadequate settlement offer, or complex property damage in Jacksonville, contactGlobal Public Adjusterstoday for a free claim assessment. Our licensed professionals understand Northeast Florida’s unique challenges and have secured millions in additional recoveries for homeowners throughout Duval County.