How Much Do Public Adjusters Charge in Jacksonville: Complete 2026 Fee Guide

Quick Answer

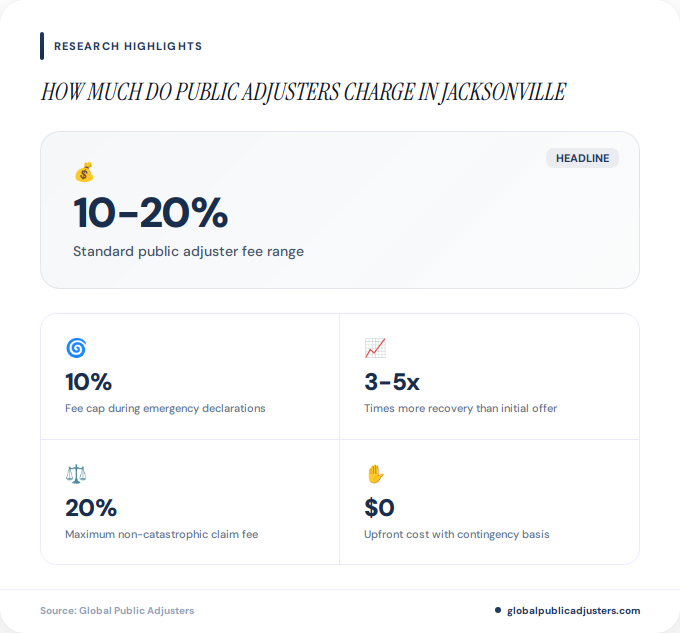

Public adjusters in Jacksonville typically charge between10-20% of your final insurance settlement, with fees capped at10% during declared states of emergencysuch as hurricanes. The exact percentage depends on whether your claim is catastrophic or non-catastrophic, and fees are based on the additional recovery they secure beyond what your insurer initially offered.

When insurance companies underpay or deny legitimate claims, Jacksonville homeowners face a critical decision: accept the lowball offer or hire a professional to fight for fair compensation. If you’ve suffered property damage from hurricanes, flooding, fire, or other perils common to Florida’s First Coast, understanding how much public adjusters charge in Jacksonville can mean the difference between recovering thousands or settling for pennies on the dollar.

The fees might seem substantial at first glance, but here’s the surprising reality:public adjusters often recover 3-5 times more than the initial insurance offer, making their commission a worthwhile investment for most complex claims. With Jacksonville’s unique exposure to tropical storms, coastal flooding, and the occasional tornado, knowing exactly what you’ll pay for professional claims assistance is essential.

This comprehensive guide breaks down every aspect of public adjuster fees in Jacksonville, from standard rates to emergency caps, legal requirements, and real-world examples that show exactly how much you’ll pay and what you’ll receive in return.

What Are the Standard Public Adjuster Fees in Jacksonville?

Public adjusters in Jacksonville operate under Florida’s regulatory framework, which establishes clear fee structures designed to protect consumers while ensuring adjusters are compensated for their expertise. TheFlorida Department of Financial Servicesgoverns these rates, and understanding them is crucial before signing any contract.

For non-catastrophic claims, such as fire damage, water damage from plumbing failures, or vandalism, public adjusters can chargeup to 20% of the total settlement amount. This represents the upper limit allowed by law, though many adjusters negotiate fees based on claim complexity and size.

During declared states of emergency, such as after Hurricane Ian or other major weather events that frequently impact Jacksonville’s coastal communities, fees are capped at10% of the insurance proceeds. This protection ensures homeowners aren’t exploited during vulnerable times when claims volume surges and assistance is desperately needed.

| Claim Type | Maximum Fee Percentage | When Applied |

|---|---|---|

| Non-Catastrophic Claims | Up to 20% | Standard claims (fire, water, theft) |

| Catastrophic/Emergency Claims | Capped at 10% | During declared state of emergency |

| Reopened Claims | 10-20% (varies) | Previously settled claims reopened |

How Does the Fee Structure Work in Florida?

Understanding the fee structure for public adjusters in Jacksonville requires familiarity with Florida Statute 626.854, which establishes the legal framework for these professionals. Unlike traditional contractors who charge upfront fees, public adjusters work on acontingency basis, meaning you pay nothing unless they successfully recover money from your insurance company.

This contingency model aligns the adjuster’s interests with yours: the more they recover, the more they earn. For Jacksonville homeowners dealing with complex claims, this arrangement provides access to professional expertise without upfront financial risk.

The fee calculation typically applies to the “new money” recovered, not necessarily the total claim amount. If your insurance company already paid $50,000 on a claim and apublic adjustersecures an additional $100,000, their fee applies to that $100,000 increment, not the entire $150,000. This distinction is critical and should beclearly outlined in your contract.

Beyond commission fees, public adjusters may also charge for reasonable out-of-pocket expenses. These can include costs for professional inspections, engineering reports, documentation fees, or specialized assessments required to substantiate your claim. According toindustry standards, these expenses should be transparently disclosed in your contract before work begins.

Why Are Fees Different for Catastrophic Claims?

Jacksonville’s location on Florida’s northeastern coast makes it particularly vulnerable to hurricanes, tropical storms, and coastal flooding. When the governor declares a state of emergency, the 10% fee cap automatically goes into effect, providing crucial protection for residents facing widespread property damage.

This reduced fee structure recognizes that catastrophic events create massive claim volumes and that homeowners in affected areas like Riverside, San Marco, and Jacksonville Beach face financial hardship. The10% emergency capensures that professional assistance remains accessible when it’s needed most.

The emergency fee cap typically applies forone year following the disaster declaration date. This means if Hurricane Season brings a major storm to Jacksonville in September 2026, claims filed within one year would qualify for the 10% maximum fee, even if the state of emergency is lifted earlier.

For homeowners in flood-prone neighborhoods like Springfield, Arlington, or Mandarin, understanding when these caps apply can save thousands of dollars. If you’re unsure whether your claim qualifies for the emergency rate, your adjuster is legally required to clarify this before you sign a contract.

How Do Public Adjusters Calculate Their Fees?

The actual calculation of public adjuster fees involves several important considerations that Jacksonville homeowners should understand before engaging services. The starting point is determining whether your claim falls under catastrophic or non-catastrophic categories, which establishes the maximum allowable percentage.

Most reputable public adjusters base their fee on thegross settlement amountthey recover, minus your deductible. For example, if they negotiate a $200,000 settlement and your policy has a $5,000 deductible, their 10% fee would apply to $195,000, resulting in a $19,500 commission.

However, some adjusters may structure fees differently based on case complexity. A straightforward wind damage claim might command a lower percentage than a complex mold remediation case requiring extensive documentation, expert testimony, and prolonged negotiations with carriers.

Understanding the distinction betweenpublic adjusters and insurance company adjustershelps clarify why these fees exist. Unlike company adjusters who work for insurers, public adjusters are your advocates, and their compensation reflects their expertise in maximizing your recovery.

What Do These Fees Look Like in Real Jacksonville Claims?

Understanding abstract percentages is one thing, but seeing real-world applications makes the cost-benefit analysis crystal clear. Let’s examine several typical Jacksonville scenarios to illustrate exactly what you’d pay and what you’d receive.

Final Settlement:$200,000

Adjuster Fee (10%):$20,000

Net Recovery:$180,000

Additional Gain:$130,000

Final Settlement:$150,000

Adjuster Fee (20%):$30,000

Net Recovery:$120,000

Additional Gain:$45,000

Final Settlement:$80,000

Adjuster Fee (20%):$16,000

Net Recovery:$64,000

Additional Gain:$39,000

Final Settlement:$275,000

Adjuster Fee (10%):$27,500

Net Recovery:$247,500

Additional Gain:$147,500

These examples demonstrate why homeowners in neighborhoods like Ortega, Avondale, and Atlantic Beach consistently choose to hire public adjusters despite the fees. The net additional recovery far exceeds the commission cost in virtually every complex claim scenario.

Consider a Jacksonville Beach condo owner whose initial claim for wind and water damage was offered at $60,000. After hiring a public adjuster who identified additional structural damage, code upgrade requirements, and proper valuation of damaged contents, the final settlement reached $180,000. Even after paying the 10% emergency fee of $18,000, the owner netted $162,000 compared to the original $60,000 offer, a gain of $102,000.

What Legal Protections Exist for Jacksonville Homeowners?

Florida law provides substantial consumer protections for Jacksonville residents hiring public adjusters. These safeguards ensure transparency, fair dealing, and clear communication throughout the claims process.

First, all public adjusters must provide awritten contractthat explicitly states all fees, services, and payment terms before you sign. This contract must clearly specify whether the percentage applies to gross settlement, new money, or another calculation method. According toFlorida regulations, contracts lacking this clarity may be unenforceable.

Second, public adjusters cannot charge fees that exceed the statutory limits: 20% for non-catastrophic claims and 10% during declared emergencies. Any contract attempting to charge more is legally void, and homeowners have recourse through the Department of Financial Services.

Third, public adjusters must be properly licensed by the state of Florida. You can verify any adjuster’s license status, complaint history, and disciplinary actions through the Florida Department of Financial Services website before signing a contract.

Fourth, you have the right to cancel a public adjuster contract withinthree business daysof signing without penalty. This cooling-off period allows you to review terms, seek legal advice if needed, and ensure you’re comfortable with the arrangement.

Are Public Adjuster Fees Worth It in Jacksonville?

The critical question every Jacksonville homeowner asks is whether paying 10-20% of their settlement is justified. The answer depends on several factors specific to your situation, but industry data suggests that for complex claims, the return on investment is substantial.

Research indicates that public adjusters typically increase settlement amounts by3-5 times or morecompared to initial offers. For claims involving structural damage, hidden damages requiring expert assessment, or complex policy interpretation, this multiplier effect often justifies the commission.

Consider the alternative: accepting your insurance company’s first offer. Insurance adjusters work for the carrier, not for you, and their job is to minimize payouts while maintaining legal compliance. Without professional representation, Jacksonville homeowners frequently accept settlements that don’t cover the full extent of damages or fail to account for code upgrades, depreciation disputes, or additional living expenses.

Public adjusters bring specialized knowledge of Florida building codes, local construction costs, and insurance policy language. In Jacksonville’s unique climate, where moisture intrusion can lead to mold, where hurricanes create both wind and water damage, and where aging infrastructure compounds losses, this expertise translates directly into higher settlements.

| Scenario | Without Public Adjuster | With Public Adjuster |

|---|---|---|

| Simple, clear-cut claims | May not need adjuster | Moderate benefit |

| Denied or underpaid claims | Minimal recovery | 3-5x higher settlements |

| Complex damage (multiple perils) | Significant underpayment risk | Substantial increase likely |

| Business interruption claims | Often overlooked or undervalued | Professional documentation crucial |

For Jacksonville homeowners dealing with claims exceeding $50,000, complex damage scenarios, or disputes with their insurance company, the statistical evidence strongly supports hiring a public adjuster despite the commission fees.

How Should You Choose a Public Adjuster in Jacksonville?

Not all public adjusters offer equal value, and selecting the right professional can significantly impact both your settlement amount and your overall experience. Jacksonville residents should evaluate several key factors before committing to a contract.

First, verify licensing and credentials. Every legitimate public adjuster in Florida must hold an active license from the Department of Financial Services. Check for complaints, disciplinary actions, or license suspensions before proceeding.

Second, ask about local experience. Adjusters familiar with Jacksonville’s specific challenges including coastal flood risks, hurricane preparedness standards, and local building codes bring invaluable expertise to your claim. An adjuster experienced with Duval County construction costs and regional insurance carrier practices will negotiate more effectively than someone unfamiliar with the area.

Third, understand the fee structure completely. Don’t just focus on the percentage, clarify exactly what that percentage applies to. Does it apply to gross settlement, new money, or settlement minus deductible? Are there additional expenses beyond the commission?Transparent fee disclosureis a hallmark of reputable adjusters.

Fourth, request references from recent Jacksonville clients. Speak with homeowners who’ve completed claims with the adjuster, particularly those in neighborhoods similar to yours or with comparable damage types.

Fifth, evaluate communication and responsiveness during your initial consultation. The adjuster who will handle your claim should be accessible, clear in explanations, and proactive about updates. Poor communication during the sales process rarely improves after contract signing.

Key Takeaways

- Public adjusters in Jacksonville charge 10-20% of settlements, with 10% caps during emergencies

- Fees are typically contingency-based with no upfront costs

- Emergency fee caps apply for one year following disaster declarations

- Adjusters typically increase settlements by 3-5 times initial offers

- Florida law requires written contracts with transparent fee disclosure

- Fees apply to new money recovered, not always total settlement amounts

- Licensed adjusters must comply with Florida Statute 626.854 regulations

People Also Ask

Can public adjusters charge more than 20% in Jacksonville?

No, Florida law caps public adjuster fees at 20% for non-catastrophic claims and 10% during declared states of emergency. Any contract attempting to charge more is legally unenforceable and should be reported to the Department of Financial Services.

Do I pay public adjuster fees upfront?

No, public adjusters work on contingency, meaning you pay nothing unless they successfully recover money from your insurance company. This arrangement protects homeowners from upfront costs while aligning the adjuster’s interests with maximizing your settlement.

How long does the 10% emergency fee cap last in Jacksonville?

The 10% emergency fee cap applies for one full year following the date of the governor’s state of emergency declaration. Claims filed within that 12-month window qualify for the reduced rate, even if the emergency declaration is lifted earlier.

Are public adjuster fees tax deductible in Florida?

Tax treatment of public adjuster fees varies based on individual circumstances and whether the loss relates to personal or business property. Consult a qualified tax professional to determine deductibility for your specific situation, as IRS rules on casualty loss deductions have changed in recent years.

Can I negotiate public adjuster fees in Jacksonville?

Yes, while fees cannot exceed statutory limits, some adjusters may negotiate lower percentages based on claim size, complexity, or other factors. Larger claims may command lower percentage fees, while complex cases requiring extensive expert analysis may warrant rates closer to the legal maximum.

What happens if my claim is denied after hiring a public adjuster?

With contingency-based fee structures, you owe nothing if your adjuster fails to recover any settlement from your insurance company. This no-recovery, no-fee arrangement protects homeowners from financial loss when claims are unsuccessful, though you may be responsible for documented out-of-pocket expenses if specified in your contract.

Frequently Asked Questions

What percentage do most public adjusters charge in Jacksonville?+

Most public adjusters in Jacksonville charge between 10-20% of the final settlement, depending on whether your claim is catastrophic or non-catastrophic. During declared states of emergency like hurricanes, fees are legally capped at 10%. For standard claims like fire or water damage, fees can reach up to 20% but are often negotiable based on claim size and complexity.

When does the 10% emergency fee cap apply in Jacksonville?+

The 10% emergency fee cap applies whenever the Florida governor declares a state of emergency affecting Jacksonville or Duval County. This typically occurs during hurricanes, tropical storms, or other major disasters. The cap remains in effect for claims filed within one year of the emergency declaration date, protecting homeowners during vulnerable recovery periods.

Do public adjusters charge fees if they don’t increase my settlement?+

No, public adjusters work on contingency, meaning they only get paid if they successfully recover money from your insurance company. If they cannot increase your settlement beyond what was initially offered, you owe nothing for their services. However, you may be responsible for documented out-of-pocket expenses like inspection fees if specified in your contract.

Are there additional costs beyond the percentage fee?+

Some public adjusters charge for out-of-pocket expenses beyond their commission, including professional inspections, engineering reports, or documentation fees. These costs should be clearly disclosed in your written contract before you sign. Reputable adjusters provide itemized expense estimates upfront and never charge hidden fees.

How do public adjuster fees compare to attorney fees for insurance claims?+

Public adjusters typically charge 10-20% of settlements, while attorneys handling insurance disputes may charge 25-40% depending on whether litigation is required. Public adjusters handle the claims process and negotiations, while attorneys become necessary if your claim requires legal action. Many homeowners start with a public adjuster and add attorney representation only if the claim reaches litigation.

Can I switch public adjusters if I’m unhappy with their service?+

Yes, you can terminate a public adjuster contract, but timing and terms matter. Florida law provides a three-day cooling-off period after signing during which you can cancel without penalty. After that, cancellation terms depend on your specific contract. If you switch adjusters mid-claim, both may claim a right to fees for work performed, so review contract terms carefully.

Does my insurance company pay the public adjuster fee?+

No, the public adjuster fee comes from your settlement proceeds, not directly from the insurance company. Your adjuster negotiates the highest possible settlement, and their fee is calculated as a percentage of that total. While this reduces your net recovery, the increased settlement typically results in substantially more money than you would have received without professional representation.