Public Adjuster vs Insurance Company in Florida: Complete 2026 Guide to Maximizing Your Claim Settlement

Quick Answer

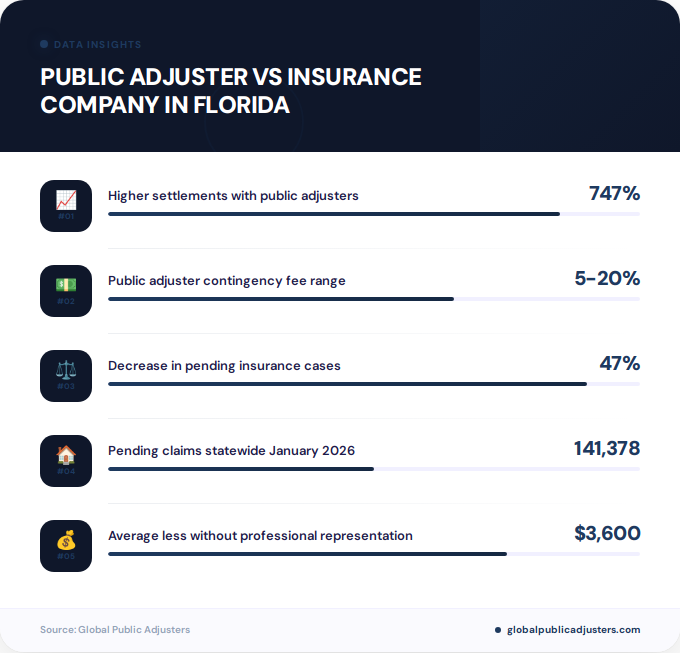

In Florida, public adjusters represent policyholders and can secure settlements up to 747% higher than initial insurance company offers, averaging $22,266 compared to $18,659 without professional representation. Insurance company adjusters work for insurers to minimize payouts, while public adjusters work exclusively for you on a contingency basis, typically earning 5-20% of the settlement only when you receive payment.

When your Florida home sustains damage from hurricanes, flooding, or other perils, understanding the difference between a public adjuster and an insurance company adjuster could mean tens of thousands of dollars in your pocket. With141,378 pending claimsstatewide as of January 2026 and insurance companies paying an average of$3,600 lesswhen policyholders navigate claims alone, the choice between these two professionals is not just important, it is financially critical.

Florida’s volatile property insurance market presents unique challenges. Recent reforms have decreased new litigation by40%and pending cases by47%, yet the fundamental conflict between policyholder interests and insurer profit motives remains unchanged. This comprehensive guide examines the public adjuster vs insurance company adjuster debate in Florida, providing you with data-driven insights to maximize your claim settlement.

What Is the Fundamental Difference Between Public Adjusters and Insurance Company Adjusters?

The most critical distinction between public adjusters and insurance company adjusters lies inwho employs them and whose interests they represent. Insurance company adjusters, also called staff adjusters or independent adjusters, work directly for your insurance carrier. Their primary responsibility is to evaluate your claim while minimizing the financial exposure for their employer.

Public adjusters, by contrast, are licensed professionals hired by policyholders to representtheir interests exclusively. In Florida, public adjusters operate under strict state regulations and earn compensation only when you receive a settlement, typically charging5-20% of the final payouton a contingency basis. This alignment of incentives fundamentally changes the claims process.

“The incentive structure is completely different. An insurance company adjuster gets paid the same salary whether your claim settles for $10,000 or $100,000, but they’re evaluated on how much money they save their employer. A public adjuster only earns a fee when you get paid, making their success directly tied to maximizing your settlement,” explains a Florida insurance industry analyst.

Insurance company adjusters are salaried employees or contract workers paid regardless of claim outcomes. According toIBISWorld’s 2026 industry analysis, Florida’s third-party administrators and claims adjusters market reached$16.0 billion, representing5.2% of state GDP. This massive industry employs thousands of adjusters focused on controlling costs for insurers.

How Does Florida’s Property Insurance Market Impact Your Claim?

Florida’s property insurance landscape in 2026 remains one of the most challenging in the nation, creating conditions where professional claim representation becomes especially valuable. The state’sJanuary 2026 Insurance Stability Unit Reportreveals persistent strain across major carriers.

Citizens Property Insurance, Florida’s insurer of last resort, carries the largest claim inventory with State Farm Florida and Slide following closely. High cancellation rates plague the market, with Praetorian Insurance leading at11.19% cancellation rate(approximately 1 in 9 policyholders) and9,865 nonrenewalsin January 2026 alone. These metrics suggest thousands of policyholders may face unreported claims before their coverage terminates.

The combination of hurricane exposure, high litigation costs, and market instability creates an environment where insurance companies aggressively defend against claims. Understanding this context helps Florida homeowners recognize why independent representation through a public adjuster can level the playing field. For homeowners dealing with property damage claims, much like those seekingprofessional insurance claim assistance, having an expert advocate makes a measurable difference.

| Carrier Metric | Data Point | Impact |

|---|---|---|

| Pending Claims (Jan 2026) | 141,378 statewide | High volume creates processing delays |

| Praetorian Cancellation Rate | 11.19% (1 in 9 policies) | Urgent need for claim filing |

| Citizens Open Lawsuits | 6,936 cases | Indicates aggressive claim denials |

What Settlement Differences Can You Expect in Florida?

The financial impact of hiring a public adjuster versus relying solely on an insurance company adjuster is substantial and well-documented.Florida industry studiesshow public adjuster-assisted claims average$22,266compared to$18,659for unrepresented policyholders, representing a19.4% increase or $3,607 difference.

Even more dramatic outcomes occur in complex or severely undervalued claims. Some Florida cases demonstrate increases ofup to 747%from initial offers. For example, an insurance company might offer $10,000 for hurricane damage, but after public adjuster involvement and proper documentation, the same claim settles for approximately $85,000. These exceptional results typically occur when insurance company adjusters miss significant damage, underestimate repair costs, or incorrectly apply policy provisions.

The math becomes compelling when you factor in contingency fees. Even after paying a public adjuster10-15% of the settlement, policyholders typically net thousands more than accepting an insurance company’s initial evaluation. For a $50,000 claim that a public adjuster increases to $65,000, the policyholder pays approximately $6,500-9,750 in fees but nets $55,250-58,500, still substantially more than the original offer.

| Claim Scenario | Without Public Adjuster | With Public Adjuster |

|---|---|---|

| Average Settlement | $18,659 | $22,266 (19.4% higher) |

| Documented Maximum Increase | Baseline offer | 747% increase ($10K to $85K) |

| Net Benefit (after 10% fee) | $18,659 | $20,039 ($1,380+ more) |

When Should You Hire a Public Adjuster in Florida?

Timing significantly impacts the effectiveness of public adjuster representation in Florida. The optimal moment to hire a public adjuster isimmediately after damage occurs and before filing your claim. Early involvement allows the public adjuster to document all damage comprehensively, preventing insurance company adjusters from disputing the extent or cause of losses.

However, public adjusters can also intervene effectively after an insurance company has made an unsatisfactory offer. Florida law provides policyholders with dispute resolution mechanisms includingmediation and appraisal. January 2026 data shows2,294 mediation casesand1,792 appraisal cases, with appraisal particularly effective for undervaluation disputes where the cause of damage isn’t contested but the repair cost estimate is inadequate.

Certain claim scenarios particularly benefit from public adjuster involvement in Florida:

- Hurricane and wind damage claims:Complex damage patterns requiring specialized assessment

- Water damage and mold:Hidden damage often missed by insurance company adjusters

- Fire and smoke damage:Extensive documentation needed for contents and structural losses

- Sinkhole claims:Highly technical evaluations requiring engineering expertise

- Large commercial property claims:Business interruption and complex valuation issues

- Claims exceeding $50,000:Higher stakes justify professional representation costs

With Praetorian Insurance’s11.19% cancellation rateand thousands of nonrenewals monthly, Florida policyholders facing policy termination should prioritize filing claims before coverage ends. A public adjuster can expedite documentation and filing to preserve claim rights.

How Do Public Adjusters Get Paid vs Insurance Company Adjusters?

The compensation models for public adjusters versus insurance company adjusters in Florida fundamentally shape their claim handling approaches. Insurance company adjusters receivesalaries or hourly wagesregardless of claim outcomes. Their performance reviews often emphasize cost containment, claim closure rates, and adherence to company reserve guidelines, creating inherent conflicts with policyholder interests.

Public adjusters in Florida operate oncontingency fee arrangements, typically charging5-20%of the final settlement with no upfront costs. This “no recovery, no fee” structure aligns their financial success directly with maximizing your claim. Florida public adjusters earned an average salary of$48,531 annually ($23.33/hour)as of March 2026, though experienced professionals handling large claims earn substantially more through percentage-based fees.

Florida law strictly regulates public adjuster fees and contracts. Public adjusters must provide written contracts specifying their fee percentage, services included, and policyholder rights. The contract must clearly state that policyholders can cancel within72 hourswithout penalty. Excessive fees or unethical practices can result in license suspension or revocation.

“The contingency model creates accountability. If a public adjuster doesn’t deliver value by increasing your settlement beyond their fee, they’ve failed you. An insurance company adjuster faces no such accountability to the policyholder,” notes a Florida property insurance expert.

When evaluating whether a public adjuster’s fee represents good value, calculate your net benefit. If an insurance company offers $30,000 and a public adjuster believes they can secure $45,000, your calculation looks like this: $45,000 settlement minus 10% fee ($4,500) equals$40,500 net, or$10,500 more than accepting the original offer. The public adjuster earns their fee by delivering tangible financial benefit.

What Are Florida’s Current Insurance Litigation Trends?

Florida’s insurance litigation landscape underwent significant transformation following 2022-2023 tort reforms, directly impacting the public adjuster vs insurance company adjuster dynamic.Legal practice analysesconfirm new litigation decreased40%while pending cases dropped47%, reducing attorney involvement costs for insurers and contributing to rate stabilization.

Despite these reforms, significant litigation continues. Citizens Property Insurance faces6,936 open lawsuitswith only44% favorable outcomesfor policyholders, the lowest success rate among major carriers. By contrast, State Farm Florida’s3,416 open suitsshow84% favorableoutcomes for consumers. Security First (95%), TypTap (89%), and Slide (88%) demonstrate even stronger policyholder win rates.

These litigation patterns reveal important insights for Florida homeowners. Lower favorable outcome rates with certain carriers suggest more aggressive claim denials, making public adjuster representation particularly valuable. Public adjusters can navigate dispute resolution mechanisms like appraisal to avoid litigation costs while still securing fair settlements.

Favorable Outcomes:44%

Status:Lowest policyholder win rate

Favorable Outcomes:84%

Status:Above average for consumers

Favorable Outcomes:95%

Status:Highest policyholder win rate

Appraisal Cases:1,792 (Jan 2026)

Status:Effective for undervaluation disputes

The63% overall favorable closure ratefor claims involving professional representation demonstrates that public adjusters significantly improve policyholder outcomes, whether through negotiation, appraisal, or litigation support. Understanding your carrier’s litigation patterns helps inform whether aggressive professional representation is warranted.

How to Choose the Right Public Adjuster in Florida

Selecting a qualified public adjuster in Florida requires careful vetting to ensure you receive competent, ethical representation. Start by verifyingactive licensurethrough the Florida Department of Financial Services. All public adjusters must hold current licenses, and you can check complaint histories and disciplinary actions online.

Experience with your specific claim type matters significantly. A public adjuster specializing inhurricane damage in coastal areaslike Miami, Tampa, or Jacksonville brings different expertise than one focused on sinkhole claims in central Florida. Ask prospective adjusters about their track record with similar claims, average settlement increases, and familiarity with your insurance carrier’s practices.

Request and carefully review the written contract before signing. Florida law requires public adjusters to provide contracts specifying:

- Exact fee percentage and payment terms

- Scope of services provided

- Estimated timeline for claim resolution

- Your right to cancel within 72 hours

- Adjuster’s license number and contact information

Beware of red flags includingupfront fee demands(legitimate public adjusters work on contingency), pressure tactics to sign immediately without review time, promises of specific settlement amounts, or unwillingness to provide references. Ethical public adjusters like those atGlobal Public Adjusterswelcome questions and provide transparent information about their process and credentials.

Compare fee structures among multiple public adjusters. While the10-20% rangeis standard, some adjusters offer lower percentages for larger claims or simplified cases. However, the lowest fee doesn’t always represent the best value if the adjuster lacks expertise to maximize your settlement.

Key Takeaways

- Representation matters financially:Public adjusters secure average settlements of $22,266 versus $18,659 for unrepresented claims in Florida, with some cases achieving up to 747% increases from initial offers

- Incentive alignment drives outcomes:Insurance company adjusters work to minimize payouts for their employers, while public adjusters earn contingency fees (5-20%) only when you receive settlement, aligning their success with yours

- Florida’s market creates challenges:With 141,378 pending claims and high carrier cancellation rates (Praetorian at 11.19%), professional representation helps navigate a strained insurance environment

- Litigation patterns reveal carrier behavior:Citizens’ 44% favorable outcome rate versus Security First’s 95% shows significant variation in claim handling, informing when aggressive representation is needed

- Alternative dispute resolution works:Florida’s 1,792 appraisal cases and 2,294 mediation cases in January 2026 demonstrate effective paths to fair settlements without full litigation

- Early involvement maximizes results:Hiring a public adjuster before filing your claim allows comprehensive damage documentation and prevents disputes over loss extent

- Licensing and credentials matter:Verify active Florida licensure, relevant experience, and transparent fee agreements before engaging any public adjuster

People Also Ask

Can I hire a public adjuster after the insurance company makes an offer?

Yes, you can hire a public adjuster at any point during the claims process, even after receiving an initial settlement offer. Public adjusters frequently intervene to dispute inadequate offers through appraisal, mediation, or reopening claim investigations with additional documentation.

Do insurance companies treat claims differently when a public adjuster is involved?

Insurance companies typically respond more thoroughly when public adjusters represent claims, knowing that professional documentation and policy interpretation will challenge lowball offers. The presence of a public adjuster signals that the policyholder understands their rights and won’t accept inadequate settlements easily.

How long does a public adjuster take to settle a claim in Florida?

Settlement timelines vary based on claim complexity, but public adjusters typically resolve straightforward Florida property claims within 60-90 days. Complex claims involving extensive damage, multiple policy provisions, or disputed valuations may take 6-12 months, especially if appraisal or litigation becomes necessary.

What percentage do public adjusters charge in Florida?

Florida public adjusters typically charge contingency fees ranging from 5-20% of the final settlement, with 10-15% being most common. Higher percentages may apply to smaller claims or those requiring extensive investigation, while larger settlements often command lower percentage fees.

Are public adjusters worth it for small claims?

For claims under $10,000, public adjuster fees may consume much of the settlement increase, making self-representation more economical. However, if the insurance company denies or severely undervalues even a small claim, a public adjuster’s expertise can turn a $0 denial into a meaningful recovery that justifies their fee.

Can I negotiate with both the insurance adjuster and hire a public adjuster?

Once you hire a public adjuster, they become your authorized representative and handle all communications with the insurance company. You should not negotiate directly with the insurance adjuster simultaneously, as this creates confusion about representation and potentially undermines your public adjuster’s negotiating position.

Frequently Asked Questions

What is the main advantage of hiring a public adjuster in Florida?+

The primary advantage is significantly higher settlement amounts, with Florida data showing public adjuster-assisted claims averaging $22,266 compared to $18,659 without representation, a difference of $3,607 or 19.4%. Public adjusters handle all claim documentation, damage assessment, policy interpretation, and negotiation, removing the burden from policyholders while leveraging professional expertise to maximize recoveries.

Do public adjusters work with contractors and attorneys?+

Yes, experienced public adjusters maintain professional networks including licensed contractors for accurate repair estimates and attorneys specializing in insurance disputes. This collaboration ensures comprehensive claim support, though the public adjuster focuses specifically on claim documentation and negotiation rather than legal representation or actual repairs.

Will hiring a public adjuster delay my claim settlement?+

Initial claim documentation may take slightly longer with a public adjuster due to more thorough damage assessment, but this comprehensive approach typically prevents disputes and rework that cause greater delays. Well-documented claims with professional representation often settle faster than contested claims where policyholders repeatedly submit insufficient documentation to insurance company adjusters.

What types of damage do Florida public adjusters handle?+

Florida public adjusters handle all property damage types including hurricane and wind damage, water damage and flooding, fire and smoke damage, mold remediation, roof damage, sinkholes, theft and vandalism, and commercial property losses. Many specialize in specific damage types based on their geographic location and expertise.

How are public adjuster fees paid in Florida?+

Public adjusters work on contingency, receiving their fee (typically 5-20%) only when the insurance company pays your settlement. The fee is deducted from the settlement check, meaning you pay nothing upfront and owe nothing if no recovery is secured. All fee arrangements must be specified in a written contract per Florida law.

Can I fire my public adjuster if I’m unsatisfied?+

Yes, Florida law gives you 72 hours to cancel any public adjuster contract without penalty, and you can terminate representation later according to the contract terms. However, the public adjuster may be entitled to compensation for work already completed on your claim based on the contract provisions, so review termination clauses carefully before signing.

Does my insurance policy cover public adjuster fees?+

No, insurance policies do not cover public adjuster fees, which are the policyholder’s responsibility and deducted from the settlement. However, the increased settlement amount typically far exceeds the fee, resulting in higher net recovery. Some policies may cover appraisal costs or attorney fees under specific dispute resolution provisions, but not public adjuster services.